Financial Report and Registration Document 2010 - Groupe Seb

Financial Report and Registration Document 2010 - Groupe Seb

Financial Report and Registration Document 2010 - Groupe Seb

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

1<br />

GROUPE SEB IN <strong>2010</strong><br />

INDUSTRIAL STRATEGY<br />

INDUSTRIAL STRATEGY<br />

The Group’s industrial strategy aims to continuously improve competitive<br />

performance <strong>and</strong> quality over the long term. The French <strong>and</strong> international<br />

production plan is deployed according to three major lines:<br />

Europe-based manufacturing for products when economies of scale<br />

are feasible <strong>and</strong> where the Group is a market leader, protecting its own<br />

product concepts using specifi c technologies for products (enabling a<br />

better product mix <strong>and</strong> justifying higher prices) or for processes (allowing<br />

a decrease in the cost price);<br />

use of its own plants outside Europe for economic mass-production where<br />

the Group wishes to retain control of its specific technologies in products<br />

<strong>and</strong> processes – these same factories also make products destined for<br />

local markets;<br />

sourcing of certain basic everyday products or articles in which the Group<br />

cannot exploit economies of scale.<br />

In Europe, the Group’s competitiveness involves expertise <strong>and</strong> technology<br />

centres. Product expertise centres bring together the specifi c expertise<br />

for a core activity or product category in research <strong>and</strong> development,<br />

industrialization <strong>and</strong> production. Technological centres reinforce product<br />

centres in key cross-disciplinary technologies such as materials, plastics,<br />

heating elements or electronics. Also present in industrial sites, project<br />

platforms comprise marketing, research <strong>and</strong> sourcing teams in charge of<br />

creating product offers.<br />

The Group’s industrial facility included a total of 24 industrial sites in<br />

<strong>2010</strong> (1) which produce 70% of products sold worldwide. The other 30%<br />

are outsourced, in particular to China. More specifically, the <strong>2010</strong> breakdown<br />

of production was as follows:<br />

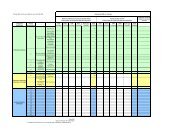

LOCATION OF SALES PRODUCTION<br />

Europe 40%<br />

In <strong>2010</strong>, contrary to 2009, the operations of the Group’s European plants<br />

benefited from low inventories in retail distribution <strong>and</strong> the good performance<br />

<strong>and</strong>/or recovery of consumption in numerous countries, with a very<br />

favourable impact on volumes. Barring a few exceptions, the plants were<br />

in a rather good, or even very good position, in relation to absorption of<br />

costs <strong>and</strong> targeted <strong>and</strong> specifi c actions were carried out in less loaded<br />

sites (production transfers, in particular).<br />

To ensure <strong>and</strong> optimise the competitiveness of its industrial capacity,<br />

<strong>Groupe</strong> SEB constantly upgrades its plants, taking account of the economic<br />

reality of markets: adjustment of volumes, refocusing of production <strong>and</strong>/<br />

or reduction of operating costs if necessary, greater use of sourcing<br />

according to needs, in addition to manufacturing capacity upgrades to meet<br />

increasingly strong dem<strong>and</strong> as is currently the case in China. For example,<br />

the extension of buildings on the Wuhan (Supor) site dedicated to cookware<br />

will allow the Group to double production capacity in 2011; the upgrade<br />

process of the new Shaoxing plant, specialised in small electrical appliances,<br />

was signifi cantly accelerated to meet booming dem<strong>and</strong> in the Chinese<br />

market. At the same time, the Group decided to reintegrate in a number of<br />

Chinese plants part of the production that had been outsourced to Chinese<br />

subcontractors (kettles, in particular). Productivity plans are first deployed<br />

throughout plants in China in order to gradually reach Group st<strong>and</strong>ards.<br />

Ultimately, the combination of sustained industrial operations <strong>and</strong> the<br />

productivity actions implemented led to genuine improvement in the Group’s<br />

industrial performance in <strong>2010</strong>.<br />

The Group has also introduced a global Supply Chain Management system<br />

intended to rationalize stocks of fi nished products, optimize the quality<br />

of these stocks <strong>and</strong> implement a process to improve customer service.<br />

The actions undertaken resulted in significant improvements of all ratios in<br />

the last three years with, in particular, a clear improvement in the inventories<br />

of low turnover products, major reduction in supply chain costs (transports<br />

<strong>and</strong> warehouses) <strong>and</strong> major progress in sales forecasts.<br />

1<br />

Sourced 30%<br />

China 20%<br />

South America 8%<br />

USA 2%<br />

(1) 26 in March 2011 (2 Imusa sites).<br />

GROUPE SEB<br />

FINANCIAL REPORT AND REGISTRATION DOCUMENT <strong>2010</strong><br />

9