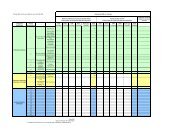

1 MANAGEMENT GROUPE SEB IN <strong>2010</strong> REPORT ON <strong>2010</strong> a very significant increase in intervention costs, which, conversely to 2009, mostly stems from the massive intensification of advertising investments in buoyant <strong>and</strong> receptive markets. Accordingly, the Group devoted €143 million to its advertising campaigns in <strong>2010</strong>, versus €95 million in 2009. The acceleration occurred mostly in the last quarter (€74 million invested against €50 million in the last 3 months of 2009). At the same time, the Group also bolstered its commercial resources <strong>and</strong> its product design costs, with the aim of boosting innovation <strong>and</strong> the product offer. Although overheads exp<strong>and</strong>ed due to the strengthening of certain structures, especially at Supor, the progress reported in ASS helped to significantly reduce related costs <strong>and</strong> the ongoing optimization of inventory management generated a significant improvement in warehousing costs; furthermore, it should be noted that the Group remained highly focused on research <strong>and</strong> development with a total investment of €73 million (including industry property costs), versus €64 million in 2009, of which €60 million was actually reported in the income statement (research tax credit of €5 million <strong>and</strong> capitalized research costs of €8 million). Operating profit climbed from €248 million in 2009 (7.8% of sales) to €349 million in <strong>2010</strong> (9.6% of sales). This 41% increase, greater than the operating margin, is linked to “Other income <strong>and</strong> charges”, which is much better than in 2009. It reached -€38.5 million (versus -€74 million in 2009), <strong>and</strong> mainly includes: approximately €5 million linked to adjustment of provisions for restructuring charges in France – due to the pension reform legislation – <strong>and</strong> ongoing litigations; provisions for charges linked to the reorganisation of the sales force in Brazil; various other low-value provisions which are broadly distributed worldwide; asset impairments amounting to some €15 million euros prudentially allocated to the goodwill of All-Clad, whose trading activity, despite the adjustment carried out in <strong>2010</strong>, has not yet returned to the levels anticipated during the acquisition. This impairment does not shed doubt on the value of the All-Clad br<strong>and</strong>, which has retained its power <strong>and</strong> medium-term potential. At the same time, at €50 million, bonuses <strong>and</strong> profi t sharing have risen significantly compared to €33.5 million in 2009. This increase is primarily linked to improved profitability in France. Net financial expense amounted to -€16 million, considerably lower compared to the -€27 million of 2009. This sharp improvement can be explained by a major reduction in interest expense (-€12 million versus -€23 million in 2009) as a result of the €277 million reduction in annual average debt. The other financial expenses are stable overall despite higher foreign exchange losses. At €220 million, net profit Group share increased by nearly 51% on the €146 million achieved in 2009. This is calculated after taxes of €89.5 million, representing a rate of 26.9%, slightly higher than the 2009 rate. It also includes minority shareholder interests for Supor, which amounts to €23 million to be deducted (€17 million in 2009). BALANCE SHEET Consolidated equity amounted to €1,571 million at 31 December <strong>2010</strong> – compared to €1,220 million at the end of 2009 – including a contribution of Supor’s minority shareholder interests for €173 million. This €351 million increase in equity (+29%) can be mostly explained by: €112 million from translation adjustments (appreciation effects of the yuan, real <strong>and</strong> dollar, especially on the valuation of the share in the net position of subsidiaries in the country concerned); for €244 million in recorded profit, less dividends paid in <strong>2010</strong> for the 2009 financial year (€56 million). This additional equity is understood to be net of SEB treasury stock, the amount of which decreased in <strong>2010</strong> after the exercise of stock options in an extremely favourable market context. At the end of <strong>2010</strong>, SEB S.A. had 1,980,698 treasury shares, versus 3,149,443 the previous year. Furthermore, net debt as at 31 December <strong>2010</strong> amounted to €131 million versus €243 million at year end 2009. This reduction of €112 million of debt reflects a new generation of cash, after an exceptional 2009. Working capital requirements reached €875 million (24% of sales) at the end of <strong>2010</strong>, versus €695 million at 31 December 2009 (21.9% of sales). This change is primarily due to an increase in stocks, especially around the end of the year: anticipation of a good first quarter 2011 for the Group <strong>and</strong> the Chinese New Year for Supor, purchase of Supor’s aluminium to freeze prices <strong>and</strong> compile stocks of Moulinex products prior to relaunching the br<strong>and</strong> in Europe early January 2011. Furthermore, cash outfl ows linked to restructuring operations amounted to €30 million (€25 million in 2009), while cash inflows linked to treasury stock sales totalled €33 million (€10 million in 2009) <strong>and</strong> the Group made no new acquisitions. Based on a debt of €131 million, the debt ratio was 0.08 at 31 December <strong>2010</strong> <strong>and</strong> marked a new consolidation of the Group’s financial position, which was already healthy with gearing of 0.20 at the end of 2009. The net debt/ EBITDA ratio also increased signifi cantly, moving from 0.65 at year end 2009 to 0.29 at year end <strong>2010</strong>, thereby demonstrating the continuation of rapid deleveraging <strong>and</strong> the Group’s enhanced capacity to pay back its debt. <strong>2010</strong> investments totalled €140 million, versus €109 million in 2009, showing a net recovery after a cautious 2009 due to the deteriorated economic climate. As in previous years, this investment was principally in tangible assets (approx. 80%) with almost equivalent distribution between moulds <strong>and</strong> tools for new products on one h<strong>and</strong> <strong>and</strong> production equipment (installation of new assembly lines, injection presses, etc.) <strong>and</strong>/or the renovation of buildings on the other h<strong>and</strong>. The remaining 20% covered mostly capitalized development costs <strong>and</strong> production-related computer software. 16 FINANCIAL REPORT AND REGISTRATION DOCUMENT <strong>2010</strong> GROUPE SEB

1 GROUPE SEB IN <strong>2010</strong> MANAGEMENT REPORT ON <strong>2010</strong> GEOGRAPHICAL BREAKDOWN OF <strong>2010</strong> SALES CASH FLOW AND INVESTMENT France 19% / 22%* € million 500 458 240 Asia / Pacific 21% / 19%* 400 368 398 210 Central Europe, Russia <strong>and</strong> other countries 18% / 17%* 300 200 140 180 150 120 1 South America 9% / 8%* 100 116 109 90 North America 11% / 11%* Other EU Western European countries 22% / 23%* 0 2008 2009 <strong>2010</strong> 60 * 2009 figures. Capital expenditure Cash flow TRADING RESULTS/SALES NET DEBT AND DEBT RATIO As a % 12 10 8 10.6 8.6 11.2 7.8 12 9.6 € million 700 600 500 400 649 0.6 1.0 0.8 0.6 300 243 0.4 6 4.5 4.6 6.0 200 100 0.2 131 0.2 4 2008 2009 <strong>2010</strong> 0 2008 2009 0.1 <strong>2010</strong> 0,0 0.0 Operating margin/sales EBIT/sales Net income/loss (Group share)/sales Gearing Net debt at 31/12 GROUPE SEB FINANCIAL REPORT AND REGISTRATION DOCUMENT <strong>2010</strong> 17