100th Annual Report 2006-2007 - Tata Steel

100th Annual Report 2006-2007 - Tata Steel

100th Annual Report 2006-2007 - Tata Steel

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Management Discussion and Analysis<br />

iron ore leases to the Government and the approval process is<br />

in progress.<br />

The Company is also pursuing setting up integrated steel<br />

plants in Chhattisgarh and Jharkhand in phases in the<br />

future.<br />

c) Other Projects in India<br />

The Company is setting up a 1.6 million tonne metallurgical<br />

coke making facility in Haldia to support future enhanced coke<br />

requirement in Jamshedpur. The project cost is estimated at<br />

Rs. 1,150 crores and will be commissioned by March 2008. The<br />

Company has acquired requisite land, completed civil work and<br />

placed orders for major equipments.<br />

2. Primary steel making in countries rich in Iron Ore and / or<br />

Coal / Gas<br />

The Company believes in a de-integrated production<br />

philosophy to maximise value in the steel industry. The<br />

Company has identified possible locations to set up primary<br />

steel making facilities in the long term. These locations<br />

(including India) are attractive by virtue of competitive factors<br />

of production i.e. availability of raw material, energy sources<br />

etc. The Company intends to link low cost steel production<br />

facilities with the most favourable steel consuming markets,<br />

to maximise value creation across the entire value chain. The<br />

Company intends to have a balance between the growing<br />

markets of the developing countries and the mature markets<br />

with high end products and technology. Investments in<br />

Nat<strong>Steel</strong> Asia Pte. Ltd. and <strong>Tata</strong> <strong>Steel</strong> (Thailand) Public Co.<br />

Ltd., (erstwhile Millennium <strong>Steel</strong>) were steps taken in this<br />

direction.<br />

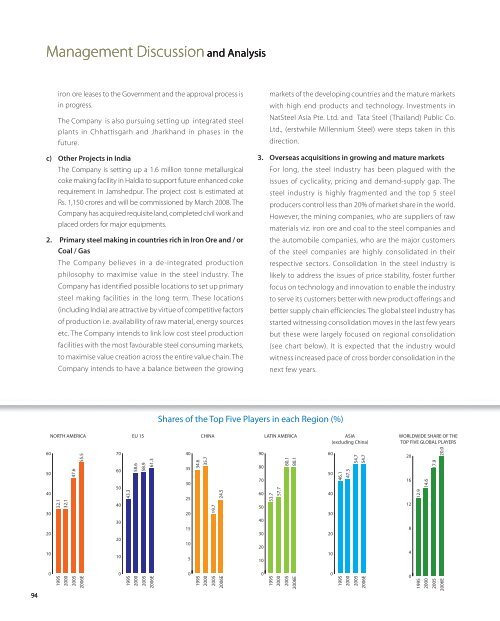

3. Overseas acquisitions in growing and mature markets<br />

For long, the steel industry has been plagued with the<br />

issues of cyclicality, pricing and demand-supply gap. The<br />

steel industry is highly fragmented and the top 5 steel<br />

producers control less than 20% of market share in the world.<br />

However, the mining companies, who are suppliers of raw<br />

materials viz. iron ore and coal to the steel companies and<br />

the automobile companies, who are the major customers<br />

of the steel companies are highly consolidated in their<br />

respective sectors. Consolidation in the steel industry is<br />

likely to address the issues of price stability, foster further<br />

focus on technology and innovation to enable the industry<br />

to serve its customers better with new product offerings and<br />

better supply chain efficiencies. The global steel industry has<br />

started witnessing consolidation moves in the last few years<br />

but these were largely focused on regional consolidation<br />

(see chart below). It is expected that the industry would<br />

witness increased pace of cross border consolidation in the<br />

next few years.<br />

Shares of the Top Five Players in each Region (%)<br />

NORTH AMERICA<br />

EU 15<br />

CHINA<br />

LATIN AMERICA<br />

ASIA<br />

(excluding China)<br />

WORLDWIDE SHARE OF THE<br />

TOP FIVE GLOBAL PLAYERS<br />

94<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

1995 32.1<br />

2000<br />

32.1<br />

47.6<br />

55.5<br />

2005<br />

<strong>2006</strong>E<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

1995 43.3<br />

2000<br />

58.6<br />

58.9<br />

61.3<br />

2005<br />

<strong>2006</strong>E<br />

40<br />

35<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

1995 34.6<br />

35.7<br />

19.7<br />

24.5<br />

2000<br />

2005<br />

<strong>2006</strong>E<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

1995 53.7<br />

2000<br />

57.7<br />

80.1<br />

80.1<br />

2005<br />

<strong>2006</strong>E<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

54.7<br />

54.7<br />

1995 46.1<br />

2000<br />

47.3<br />

2005<br />

<strong>2006</strong>E<br />

20<br />

16<br />

12<br />

8<br />

4<br />

0<br />

1995 12.9<br />

2000<br />

14.6<br />

2005<br />

17.9<br />

<strong>2006</strong>E<br />

20.0