Market Outlook - BNP PARIBAS - Investment Services India

Market Outlook - BNP PARIBAS - Investment Services India

Market Outlook - BNP PARIBAS - Investment Services India

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

After the announcement concerning the GSEs in late<br />

December, our outlook on spreads is much milder,<br />

around 15-20 bps of widening. With the<br />

announcement, agencies in total have about USD<br />

100 bn in purchasing power for the year, and can act<br />

as a backstop bid. But we underscore that our milder<br />

outlook particularly hinges on the GSEs. As shown in<br />

Chart 2, the spread to agency debt is fairly attractive<br />

on a historical basis and a small widening could go a<br />

long way in improving the economics further.<br />

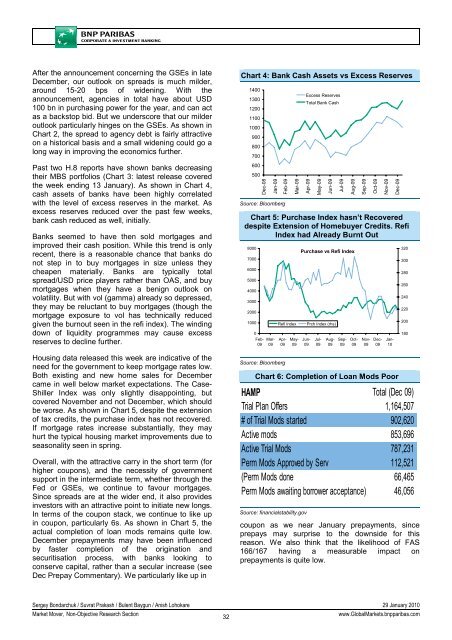

Past two H.8 reports have shown banks decreasing<br />

their MBS portfolios (Chart 3: latest release covered<br />

the week ending 13 January). As shown in Chart 4,<br />

cash assets of banks have been highly correlated<br />

with the level of excess reserves in the market. As<br />

excess reserves reduced over the past few weeks,<br />

bank cash reduced as well, initially.<br />

Banks seemed to have then sold mortgages and<br />

improved their cash position. While this trend is only<br />

recent, there is a reasonable chance that banks do<br />

not step in to buy mortgages in size unless they<br />

cheapen materially. Banks are typically total<br />

spread/USD price players rather than OAS, and buy<br />

mortgages when they have a benign outlook on<br />

volatility. But with vol (gamma) already so depressed,<br />

they may be reluctant to buy mortgages (though the<br />

mortgage exposure to vol has technically reduced<br />

given the burnout seen in the refi index). The winding<br />

down of liquidity programmes may cause excess<br />

reserves to decline further.<br />

Housing data released this week are indicative of the<br />

need for the government to keep mortgage rates low.<br />

Both existing and new home sales for December<br />

came in well below market expectations. The Case-<br />

Shiller Index was only slightly disappointing, but<br />

covered November and not December, which should<br />

be worse. As shown in Chart 5, despite the extension<br />

of tax credits, the purchase index has not recovered.<br />

If mortgage rates increase substantially, they may<br />

hurt the typical housing market improvements due to<br />

seasonality seen in spring.<br />

Overall, with the attractive carry in the short term (for<br />

higher coupons), and the necessity of government<br />

support in the intermediate term, whether through the<br />

Fed or GSEs, we continue to favour mortgages.<br />

Since spreads are at the wider end, it also provides<br />

investors with an attractive point to initiate new longs.<br />

In terms of the coupon stack, we continue to like up<br />

in coupon, particularly 6s. As shown in Chart 5, the<br />

actual completion of loan mods remains quite low.<br />

December prepayments may have been influenced<br />

by faster completion of the origination and<br />

securitisation process, with banks looking to<br />

conserve capital, rather than a secular increase (see<br />

Dec Prepay Commentary). We particularly like up in<br />

Chart 4: Bank Cash Assets vs Excess Reserves<br />

1400<br />

1300<br />

1200<br />

1100<br />

1000<br />

900<br />

800<br />

700<br />

600<br />

500<br />

Dec-08<br />

Jan-09<br />

Feb-09<br />

Source: Bloomberg<br />

Mar-09<br />

Excess Reserves<br />

Total Bank Cash<br />

Apr-09<br />

May-09<br />

Jun-09<br />

Chart 5: Purchase Index hasn’t Recovered<br />

despite Extension of Homebuyer Credits. Refi<br />

Index had Already Burnt Out<br />

8000<br />

7000<br />

6000<br />

5000<br />

4000<br />

3000<br />

2000<br />

1000<br />

0<br />

Feb-<br />

09<br />

Mar-<br />

09<br />

Apr-<br />

09<br />

Source: Bloomberg<br />

Refi Index<br />

May-<br />

09<br />

coupon as we near January prepayments, since<br />

prepays may surprise to the downside for this<br />

reason. We also think that the likelihood of FAS<br />

166/167 having a measurable impact on<br />

prepayments is quite low.<br />

Jul-09<br />

Aug-09<br />

Purchase vs Refi Index<br />

Jun-<br />

09<br />

Prch Index (rhs)<br />

Jul-<br />

09<br />

Aug-<br />

09<br />

Sep-<br />

09<br />

Oct-<br />

09<br />

Sep-09<br />

Nov-<br />

09<br />

Oct-09<br />

Dec-<br />

09<br />

Nov-09<br />

Jan-<br />

10<br />

Chart 6: Completion of Loan Mods Poor<br />

HAMP Total (Dec 09)<br />

Trial Plan Offers 1,164,507<br />

# of Trial Mods started 902,620<br />

Active mods 853,696<br />

Active Trial Mods 787,231<br />

Perm Mods Approved by Serv 112,521<br />

(Perm Mods done 66,465<br />

Perm Mods awaiting borrower acceptance) 46,056<br />

Source: financialstability.gov<br />

Dec-09<br />

320<br />

300<br />

280<br />

260<br />

240<br />

220<br />

200<br />

180<br />

Sergey Bondarchuk / Suvrat Prakash / Bulent Baygun / Anish Lohokare 29 January 2010<br />

<strong>Market</strong> Mover, Non-Objective Research Section<br />

32<br />

www.Global<strong>Market</strong>s.bnpparibas.com