- Page 3 and 4:

Your comments on the format and con

- Page 5 and 6:

During the course of this project,

- Page 7 and 8:

AcknowledgmentsThese Guidelines rep

- Page 9 and 10:

FundingFunding of this project was

- Page 11 and 12:

Table of ContentsBook 1SubjectPage

- Page 13 and 14:

1. Introduction1.1 GeneralGood asse

- Page 15 and 16:

(iv) provide proven practice approa

- Page 17 and 18:

3. Research Procedure3.1 Terms of R

- Page 19 and 20:

4. How to use these Guidelines4.1 W

- Page 21 and 22:

6. Units of MeasurementQuantity Uni

- Page 23 and 24:

8. Earthen Irrigation Channels8.1 D

- Page 25 and 26:

8.3 ReferencesAustralian National C

- Page 27 and 28:

9.1 IntroductionA key input to adva

- Page 29 and 30:

Data from Goulburn-Murray Water’s

- Page 31 and 32:

General 1 2 3 4 5 6DescriptionRisk

- Page 33 and 34:

Channel BankSequential Deterioratio

- Page 35 and 36:

9.2 ReferencesGutteridge Haskins &

- Page 37 and 38:

10.2.3.1 Dispersive layer of materi

- Page 39 and 40:

Causes ofSpecific factorDeteriorati

- Page 41 and 42:

10.1.2.5 BendsA bend in the channel

- Page 43 and 44:

10.1.4.1 Construction techniqueIrri

- Page 45 and 46:

10.1.5.4 Overtopping of banksIn ade

- Page 47 and 48:

In the past maintenance techniques

- Page 49 and 50:

Maintenance is a continuing require

- Page 51 and 52:

10.1.7.4 Yabbies/fresh water crayfi

- Page 54 and 55:

Direct removal ofmaterial by entrai

- Page 56 and 57:

Figure 10.10 shows longitudinal cra

- Page 58 and 59:

10.2.3.3 Irregular compaction - bri

- Page 60 and 61:

10.3 ReferencesEmerson W (1996), pe

- Page 62 and 63:

11.1 GeneralThe Investigation and P

- Page 64 and 65:

iv) Available fill materials and, w

- Page 66 and 67:

12.15 Radius of Bends .............

- Page 68 and 69:

There are several ways a channel ca

- Page 70 and 71:

• Land acquisition extent and typ

- Page 72 and 73:

The investigation should generally

- Page 74 and 75:

• Backfill: 10% compaction factor

- Page 76 and 77:

1. Flow Area, A, is the cross-secti

- Page 78 and 79:

after ageing and weed growth. If an

- Page 80 and 81: elationships may be the controlling

- Page 82 and 83: These maximum velocities should be

- Page 84 and 85: Thus channels are usually designed

- Page 86 and 87: Some of the design issues that shou

- Page 88 and 89: 12.12.1.3 Best PracticeEither of th

- Page 90 and 91: 12.13.2 Channel MaintenanceIncrease

- Page 92 and 93: along a channel. The depth of the w

- Page 94 and 95: 12.13.4.7 Change of AlignmentThe in

- Page 96 and 97: 12.15 Radius of Bends12.15.1 Flow A

- Page 98 and 99: 12.16 Channel Cross SectionThe cros

- Page 100 and 101: Some irrigation authorities use one

- Page 102 and 103: 12.16.2 BanksChannel cross sections

- Page 104 and 105: Unless the bank is very high, the s

- Page 106 and 107: The stability of channel batters ca

- Page 108 and 109: drop bars become difficult and time

- Page 110 and 111: Both the height above the bed and t

- Page 112 and 113: • enable maintenance of the chann

- Page 114 and 115: - Access agreementsA description of

- Page 116 and 117: 13/08/02 19:2012.20 Channel Tenure

- Page 118 and 119: 13/08/02 19:20As with the damage to

- Page 120 and 121: 13/08/02 19:20Advantages of Protect

- Page 122 and 123: - gates provide a better deterrent

- Page 124 and 125: 13/08/02 19:20When considering expo

- Page 126 and 127: 13/08/02 19:20A typical design draw

- Page 128 and 129: 13/08/02 19:20Sinclair Knight Merz

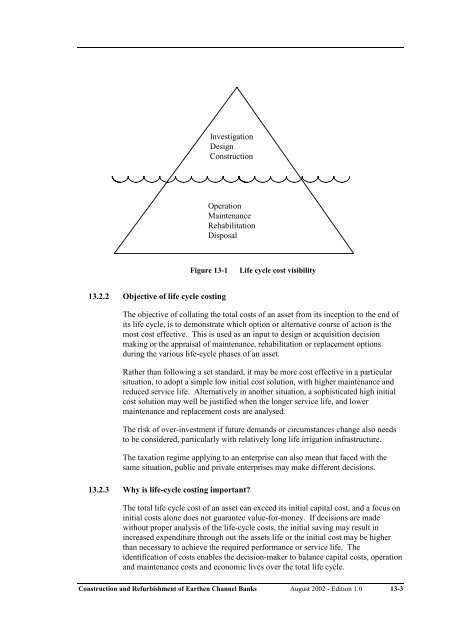

- Page 132 and 133: For example, the initial constructi

- Page 134 and 135: 13.2.6 When to use Life Cycle Analy

- Page 136 and 137: The timing of the life-cycle costin

- Page 138 and 139: • assess cost of collecting missi

- Page 140 and 141: Microsoft Excel has quite a good pr

- Page 142 and 143: The costs used in these methods sho

- Page 144 and 145: Life CyclePhaseInvestigationDesignC

- Page 146 and 147: Life CyclePhaseMaintenanceRehabilit

- Page 148 and 149: ReplacementProject managementInvest

- Page 150 and 151: Residual valueLegal feesInsuranceAd

- Page 152 and 153: 13.4.6.2 Recurring CostsChannel con

- Page 154 and 155: $1.00.80Percent ofValue of$1.00.60.

- Page 156 and 157: 13.4.11 Evaluate ResultsThe results

- Page 158 and 159: 13.6 Tipsthe way open to incur sign

- Page 160 and 161: 14. Risk AnalysisTable of ContentsS

- Page 162 and 163: Consequences for irrigation authori

- Page 164 and 165: 15. Material Selection and TestingT

- Page 166 and 167: c) Shrinkage - will the bank crack

- Page 168 and 169: depth. For this reason, the soils o

- Page 170 and 171: Natural moisture content should als

- Page 172 and 173: The study identified some confusion

- Page 174 and 175: 15.4.2 Determination of the plastic

- Page 176 and 177: 1. Preparation of PatTake approxima

- Page 178 and 179: EmersonClass No.Degree ofDispersion

- Page 180 and 181:

15.7.1 Coarse grained soilsIn this

- Page 182 and 183:

sufficient gravel for erosion resis

- Page 184 and 185:

GroupSymbolsSuitability for Earthen

- Page 186 and 187:

The uniform application and thoroug

- Page 188 and 189:

essential that the chemical is thor

- Page 190 and 191:

Where laboratory testing facilities

- Page 192 and 193:

Clays are the plastic fines. They c

- Page 194 and 195:

etween the soil sample and the wate

- Page 196 and 197:

16. Compaction ControlTable of Cont

- Page 198 and 199:

16.1 PurposeDuring this research pr

- Page 200 and 201:

All compaction equipment utilises s

- Page 202 and 203:

The soil density required for a cha

- Page 204 and 205:

In the past, a method specification

- Page 206 and 207:

Low permeability and high stability

- Page 208 and 209:

16.10.1.1 Tamping Foot RollerTampin

- Page 210 and 211:

16.10.1.5 Non-Circular Impact Rolle

- Page 212 and 213:

16.10.3 Compactor OperationsAfter t

- Page 214 and 215:

16.11.4 Moisture Content ControlBef

- Page 216 and 217:

16.12 Density Control Tests and Pro

- Page 218 and 219:

Correlation with local materials an

- Page 220 and 221:

The main advantages of the Nuclear

- Page 222 and 223:

Figure 16.4Hilf Density Ratio Repor

- Page 224 and 225:

The location and test results for e

- Page 226 and 227:

16.14.3 Reporting and RecordsTest r

- Page 228 and 229:

16.16 Tests for small projectsThe s

- Page 230 and 231:

The advantages of the Drop Test are

- Page 232 and 233:

AS1289.6.3.2-1997AS1289.6.3.3-1997A

- Page 234 and 235:

17. Protective CoverTable of Conten

- Page 236 and 237:

The bank dries and cracks from the

- Page 238 and 239:

17.5 Specifications17.5.1 GravelPar

- Page 240 and 241:

17.6 Establish Vegetation CoverTops

- Page 242 and 243:

Species Growing Conditions Establis

- Page 244 and 245:

17.7.2 Rope Wick ApplicationMuch of

- Page 246 and 247:

There are a number of fibre mats or

- Page 248 and 249:

17.10 Australian StandardsAS1289.3.

- Page 250 and 251:

18.1 IntroductionFor many earthen c

- Page 252 and 253:

When re-shaping the batters of exis

- Page 254 and 255:

LifeCrestOld bank lineBattered bank

- Page 256 and 257:

Photos\inside batter\CG7channel2arm

- Page 258 and 259:

4. To help place the rock material

- Page 260 and 261:

False ToeFigure 18.8Protective laye

- Page 262 and 263:

The confinement system would be adv

- Page 264 and 265:

• Able to survive during non-oper

- Page 266 and 267:

18.6 ReferencesHutchison D & Locke

- Page 268 and 269:

19.20 Guidelines on Field Quality C

- Page 270 and 271:

Construction and Refurbishment of E

- Page 272 and 273:

• Figure 19.2)3. Temporary Bench

- Page 274 and 275:

The capabilities and limitations of

- Page 276 and 277:

19.3.1 Construction EquipmentThe ba

- Page 278 and 279:

construction. The aim of scarifying

- Page 280 and 281:

Whether or not a front-end loader o

- Page 282 and 283:

The thickness of each layer will va

- Page 284 and 285:

distribution. The use of alternativ

- Page 286 and 287:

19.8 Construction RecordsAdequate r

- Page 288 and 289:

19.12 Protective Cover on Crest and

- Page 290 and 291:

19.21 Australian StandardsAS 1726-1

- Page 292 and 293:

20.1 ScopeAustralia’s earthen irr

- Page 294 and 295:

Bank re-construction normally requi

- Page 296 and 297:

•meter outlet locations and type

- Page 298 and 299:

In the case of channel bank refurbi

- Page 300 and 301:

20.4.1.1 StrippingWith outside bank

- Page 302 and 303:

All public roads to be used by truc

- Page 304 and 305:

5. Material is delivered by trucks

- Page 306 and 307:

Need to drain and de-waterEBM befor

- Page 308 and 309:

significantly and a more conservati

- Page 310 and 311:

Aim for crest width ofabout 2 metre

- Page 312 and 313:

Refer to Section 18, Inside Batter

- Page 314 and 315:

21.8.10 Re-alignment ..............

- Page 316 and 317:

Seepage is a complex hydrologic phe

- Page 318 and 319:

2. Seepage losses increase as the d

- Page 320 and 321:

Refer also to the following section

- Page 322 and 323:

21.4 Channel Seepage ConsequencesSe

- Page 324 and 325:

Channel seepage is one of the sever

- Page 326 and 327:

Seepage is proportional to soil per

- Page 328 and 329:

Methods based on vertical flow meas

- Page 330 and 331:

ainfallPumpingevapotranspirationIrr

- Page 332 and 333:

Flow NetsA flow net is a system of

- Page 334 and 335:

Data from indirect measurement proc

- Page 336 and 337:

(ii) EM SurveyElectro-magnetic (EM)

- Page 338 and 339:

The volume of waterloss from the dr

- Page 340 and 341:

21.7.3.2 Inflow-Outflow Method (Dyn

- Page 342 and 343:

Imperfect seal will cause the meter

- Page 344 and 345:

The groundwater level can then be d

- Page 346 and 347:

Stable IsotopesThe basis of testing

- Page 348 and 349:

To be most successful, there needs

- Page 350 and 351:

21.8.6 Surface interception drainag

- Page 352 and 353:

KeyWatertable before tree plantingW

- Page 354 and 355:

• The preparation of a best pract

- Page 356 and 357:

21.11 ReferencesAustralian National

- Page 358 and 359:

22. Channel LiningTable of Contents

- Page 360 and 361:

22.1 IntroductionThe conservation o

- Page 362 and 363:

The different types of channel lini

- Page 364 and 365:

Table 22-1Unlined Earthen Channels

- Page 366 and 367:

Lining of channels will not elimina

- Page 368 and 369:

To supply a given discharge, the cr

- Page 370 and 371:

22.4.5 Structural SafetyThe stabili

- Page 372 and 373:

soil pressures and under-drainage i

- Page 374 and 375:

Concrete linings are suitable for b

- Page 376 and 377:

22.5.12 Availability of Constructio

- Page 378 and 379:

esistance to erosion. To improve th

- Page 380 and 381:

Construction and Refurbishment of E

- Page 382 and 383:

22.7.1.2 General Design Considerati

- Page 384 and 385:

22.7.1.4 Lining ThicknessThe thickn

- Page 386 and 387:

particular problems, but in smaller

- Page 388 and 389:

Where the earth lining finishes abo

- Page 390 and 391:

control where the channel material

- Page 392 and 393:

sand requires about 5% cement by we

- Page 394 and 395:

22.7.6 Soil SealantsSoil sealants a

- Page 396 and 397:

22.7.7 Cost of Earth LiningsThe cap

- Page 398 and 399:

Although they can assist with shear

- Page 400 and 401:

22.8.2 Membrane Liner TypesGeomembr

- Page 402 and 403:

Polyethylene has also appeared in m

- Page 404 and 405:

FPP resistance to common chemical e

- Page 406 and 407:

The base coat and seal coat rates m

- Page 408 and 409:

A common and misleading argument is

- Page 410 and 411:

These thermal expansion and contrac

- Page 412 and 413:

Another factor is the ability to ha

- Page 414 and 415:

Some lining methods expand and cont

- Page 416 and 417:

22.8.9.1 Geomembrane ThicknessThe t

- Page 418 and 419:

Cover typeThickness ofEarth fill(m)

- Page 420 and 421:

22.8.9.5 Cover MaterialGeomembranes

- Page 422 and 423:

As well, velocities which are permi

- Page 424 and 425:

22.8.11 FencingWhen livestock, part

- Page 426 and 427:

22.10 ReferencesAlther GR (1987), T

- Page 428 and 429:

23. Measures to Reduce the Rate ofD

- Page 430 and 431:

Channel DesignBank MaterialDeterior

- Page 432 and 433:

Stock and VerminAdjacentlandholders

- Page 434 and 435:

To ensure that a channel bank has a

- Page 436 and 437:

Advantages of Draining• Allows fo

- Page 438 and 439:

To efficiently maintain a channel,

- Page 440 and 441:

Compared with other countries where

- Page 442 and 443:

23.4.7 LeaksTransverse cracks are t

- Page 444 and 445:

23.5 Reduction of Deterioration due

- Page 446 and 447:

Photo 23-1Channel bed showing mumbl

- Page 448 and 449:

Thus, control of carp by draining c

- Page 450 and 451:

The disadvantages of a biological c

- Page 452 and 453:

Carp have been blamed for erosion o

- Page 454 and 455:

Management Groups gives guidelines

- Page 456 and 457:

Organisation Contact Details Aims/A

- Page 458 and 459:

Chemical treatment is often recomme

- Page 460 and 461:

23.7 Reduction of Deterioration due

- Page 462 and 463:

Grey Parrot Pea - Dillaynia cineres

- Page 464 and 465:

Lodge G (1998), Review on Fish Barr

- Page 466 and 467:

cation exchange capacity (CEC) a me

- Page 468 and 469:

fetch the distance over which the w

- Page 470 and 471:

plant term used for construction eq

- Page 472:

supply level the supply level is a