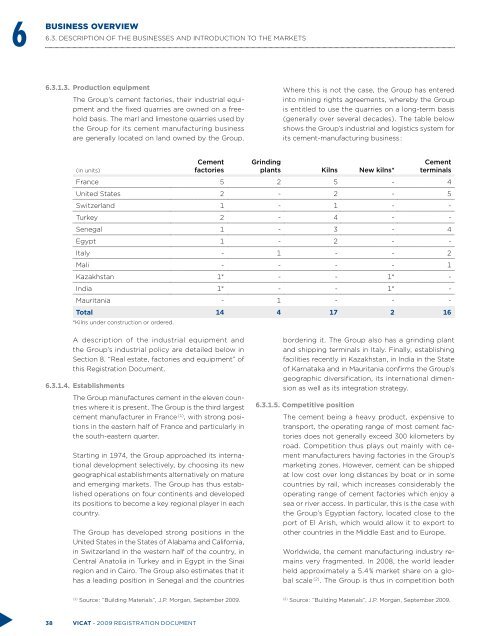

6BUSINESS OVERVIEW6.3. DESCRIPTION OF THE BUSINESSES AND INTRODUCTION TO THE MARKETS6.3.1.3. Production equipmentThe Group’s cement factories, their industrial equipmentand the fixed quarries are owned on a freeholdbasis. The marl and limestone quarries used bythe Group for its cement manufacturing businessare generally located on land owned by the Group.Where this is not the case, the Group has enteredinto mining rights agreements, whereby the Groupis entitled to use the quarries on a long-term basis(generally over several decades). The table belowshows the Group’s industrial and logistics system forits cement-manufacturing business :(in units)CementfactoriesGrindingplants Kilns New kilns*CementterminalsFrance 5 2 5 - 4United States 2 - 2 - 5Switzerland 1 - 1 - -Turkey 2 - 4 - -Senegal 1 - 3 - 4Egypt 1 - 2 - -Italy - 1 - - 2Mali - - - - 1Kazakhstan 1* - - 1* -India 1* - - 1* -Mauritania - 1 - - -Total 14 4 17 2 16*Kilns under construction or ordered.A description of the industrial equipment andthe Group’s industrial policy are detailed below inSection 8. “Real estate, factories and equipment” ofthis Registration Document.6.3.1.4. EstablishmentsThe Group manufactures cement in the eleven countrieswhere it is present. The Group is the third largestcement manufacturer in France (1) , with strong positionsin the eastern half of France and particularly inthe south-eastern quarter.Starting in 1974, the Group approached its internationaldevelopment selectively, by choosing its newgeographical establishments alternatively on matureand emerging markets. The Group has thus establishedoperations on four continents and developedits positions to become a key regional player in eachcountry.The Group has developed strong positions in theUnited States in the States of Alabama and California,in Switzerland in the western half of the country, inCentral Anatolia in Turkey and in Egypt in the Sinairegion and in Cairo. The Group also estimates that ithas a leading position in Senegal and the countriesbordering it. The Group also has a grinding plantand shipping terminals in Italy. Finally, establishingfacilities recently in Kazakhstan, in India in the Stateof Karnataka and in Mauritania confirms the Group’sgeographic diversification, its international dimensionas well as its integration strategy.6.3.1.5. Competitive positionThe cement being a heavy product, expensive totransport, the operating range of most cement factoriesdoes not generally exceed 300 kilometers byroad. Competition thus plays out mainly with cementmanufacturers having factories in the Group’smarketing zones. However, cement can be shippedat low cost over long distances by boat or in somecountries by rail, which increases considerably theoperating range of cement factories which enjoy asea or river access. In particular, this is the case withthe Group’s Egyptian factory, located close to theport of El Arish, which would allow it to export toother countries in the Middle East and to Europe.Worldwide, the cement manufacturing industry remainsvery fragmented. In 2008, the world leaderheld approximately a 5.4 % market share on a globalscale (2) . The Group is thus in competition both(1)Source : “Building Materials”, J.P. Morgan, September 2009.(2)Source : “Building Materials”, J.P. Morgan, September 2009.38 VICAT - 2009 registration document

BUSINESS OVERVIEW6.3. DESCRIPTION OF THE BUSINESSES AND INTRODUCTION TO THE MARKETS6with national cement manufacturers such as Oyakin Turkey or Ciments du Sahel in Senegal and withmultinational cement manufacturers such as Lafarge(France), Cemex (Mexico), Holcim (Switzerland),HeidelbergCement (Germany) or Italcementi (Italy),which operate in a number of the Group’s markets.6.3.1.6. CustomersThe profiles of customers are similar in most areas inthe world where the Group is established. The Groupsells either to general contractors, such as concretemixers, manufacturers of prefabricated concrete elements,contractors in the construction and publicworks sector, local authorities, residential property developersor master masons, or to intermediaries suchas construction material wholesalers or supermarketchains. The relative weight of one type of customer,however, can vary significantly from one country ofoperation to another according to the maturity of themarket and local construction practices.In addition, cement is marketed either in bulk or inbags. According to the level of development of eachoperating country, the packaging mix (bulk/bag)and the mix of customer types can vary significantly.Accordingly, as the ready-mixed concrete system isstrongly developed in the United States, the Group primarilysells its cement in bulk and mostly to concretemixers. Conversely, Senegal does not yet have a readymixedconcrete network and the Group sells its cementprimarily in bags to wholesalers and to retailers.6.3.1.7. Overview of the cement marketsThe Group has 12 cement factories spread over sixcountries, as well as four cement grinding plants establishedin three countries. The table below summarizesthe cement volumes sold by country :(in millions of tonnes)* 2009 2008 2007France 3,218 3,771 3,904United States 1,271 1,766 2,127Switzerland 754 715 724Turkey 3,087 3,160 2,969Senegal/Mali/Mauritania 2,260 1,969 1,939Egypt 3,493 2,370 1,983Italy 424 474 509Total 14,507 14,225 14,155*Volumes of cement, clinker and masonry cement.Intra-group cement sales accounted for 16 % of theGroup’s activity, with a significant disparity rangingfrom 0 % to 33 % depending on each operatingcountry.The various cement markets are discussed below,together with their size and their development overthe last five years. Price changes are covered inSection 9. “Examination of the financial situation andresults” of this Registration Document.(a) FranceThe new build sector is down by 21.8 % due to thedecline in new housing and non-residential buildingconstruction (1) . The public works sector declined by7.5 %, with this fall leveling off in the final months ofthe year. Orders received in the final months were upby comparison with the same period in 2008, signalingthe first effects of the government’s economicstimulus plan.Historic birthplace of the Group, the French cementmarket is mature, with consumption of 20.4 milliontonnes in 2009 (2) . Consumption reached approximately386 kg of cement per capita in 2008 (3) .Since 2004, owing to the drop in consumption overthe last two years, sales volumes have fallen byapproximately 7 % over five years (4) , or an averageannual decrease of 1.5 % over the period. Between2007 and 2009, French cement consumption showedan average annual decrease of 5.1 %, owing to thedecline in cement consumption which began in 2008(-2.8 %), accelerated in 2009 to end at -15.5 %, againsta difficult economic situation for the economy as awhole. Cement consumption is expected to fall furtherin 2010 by around 3 to 5 %, taking into accountthe government’s economic stimulus plan.(1)Source : Commissariat Général au Développement Durable.(2)Source : SFIC, 2009.(3)Source : Cembureau (organization representing theEuropean cement industry, comprising 26 members).(4)Source : SFIC, 2009.2009 registration document - VICAT 39