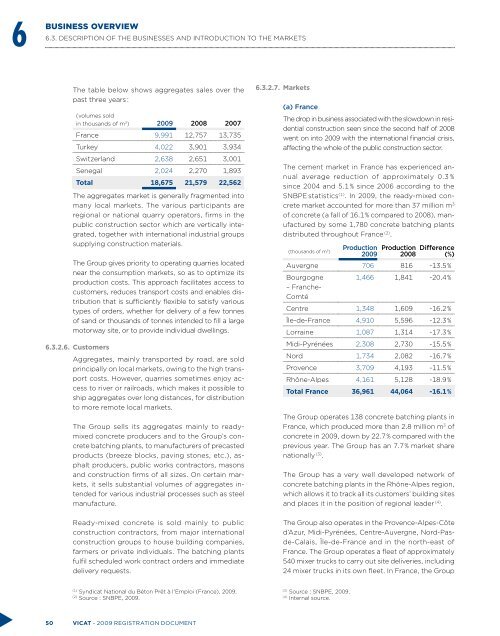

6BUSINESS OVERVIEW6.3. DESCRIPTION OF THE BUSINESSES AND INTRODUCTION TO THE MARKETSThe table below shows aggregates sales over thepast three years :(volumes soldin thousands of m 3 ) 2009 2008 2007France 9,991 12,757 13,735Turkey 4,022 3,901 3,934Switzerland 2,638 2,651 3,001Senegal 2,024 2,270 1,893Total 18,675 21,579 22,562The aggregates market is generally fragmented intomany local markets. The various participants areregional or national quarry operators, firms in thepublic construction sector which are vertically integrated,together with international industrial groupssupplying construction materials.The Group gives priority to operating quarries locatednear the consumption markets, so as to optimize itsproduction costs. This approach facilitates access tocustomers, reduces transport costs and enables distributionthat is sufficiently flexible to satisfy varioustypes of orders, whether for delivery of a few tonnesof sand or thousands of tonnes intended to fill a largemotorway site, or to provide individual dwellings.6.3.2.6. CustomersAggregates, mainly transported by road, are soldprincipally on local markets, owing to the high transportcosts. However, quarries sometimes enjoy accessto river or railroads, which makes it possible toship aggregates over long distances, for distributionto more remote local markets.The Group sells its aggregates mainly to readymixedconcrete producers and to the Group’s concretebatching plants, to manufacturers of precastedproducts (breeze blocks, paving stones, etc.), asphaltproducers, public works contractors, masonsand construction firms of all sizes. On certain markets,it sells substantial volumes of aggregates intendedfor various industrial processes such as steelmanufacture.Ready-mixed concrete is sold mainly to publicconstruction contractors, from major internationalconstruction groups to house building companies,farmers or private individuals. The batching plantsfulfil scheduled work contract orders and immediatedelivery requests.6.3.2.7. Markets(a) FranceThe drop in business associated with the slowdown in residentialconstruction seen since the second half of 2008went on into 2009 with the international financial crisis,affecting the whole of the public construction sector.The cement market in France has experienced annualaverage reduction of approximately 0.3 %since 2004 and 5.1 % since 2006 according to theSNBPE statistics (1) . In 2009, the ready-mixed concretemarket accounted for more than 37 million m 3of concrete (a fall of 16.1 % compared to 2008), manufacturedby some 1,780 concrete batching plantsdistributed throughout France (2) .(thousands of m 3 )Production2009 Production2008 Difference(%)Auvergne 706 816 -13.5 %Bourgogne 1,466 1,841 -20.4 %– Franche-ComtéCentre 1,348 1,609 -16.2 %Île-de-France 4,910 5,596 -12.3 %Lorraine 1,087 1,314 -17.3 %Midi-Pyrénées 2,308 2,730 -15.5 %Nord 1,734 2,082 -16.7 %Provence 3,709 4,193 -11.5 %Rhône-Alpes 4,161 5,128 -18.9 %Total France 36,961 44,064 -16.1 %The Group operates 138 concrete batching plants inFrance, which produced more than 2.8 million m 3 ofconcrete in 2009, down by 22.7 % compared with theprevious year. The Group has an 7.7 % market sharenationally (3) .The Group has a very well developed network ofconcrete batching plants in the Rhône-Alpes region,which allows it to track all its customers’ building sitesand places it in the position of regional leader (4) .The Group also operates in the Provence-Alpes-Côted’Azur, Midi-Pyrénées, Centre-Auvergne, Nord-Pasde-Calais,Île-de-France and in the north-east ofFrance. The Group operates a fleet of approximately540 mixer trucks to carry out site deliveries, including24 mixer trucks in its own fleet. In France, the Group(1)Syndicat National du Béton Prêt à l'Emploi (France), 2009.(2)Source : SNBPE, 2009.(3)Source : SNBPE, 2009.(4)Internal source.50 VICAT - 2009 registration document

BUSINESS OVERVIEW6.3. DESCRIPTION OF THE BUSINESSES AND INTRODUCTION TO THE MARKETS6provides most of the cement and approximately onethird of the aggregates consumed by its ready-mixedconcrete business, which illustrates the high degreeof vertical integration of its activities.In France, the technical sales team of the Group’sready-mixed concrete division benefits from thecollaboration from Sigma Béton, a key unit of theLouis <strong>Vicat</strong> Technical Centre, specialising in theready-mixed concrete, aggregates and road productssectors, certified to ISO 9002 for the formulation,analysis and audit of aggregates, cement andconcrete. Sigma Béton also runs a training business,research and development and analysis services forconcretes delivered to producers, to manufacturersin the concrete products sector and to constructionand public works contractors.The French aggregates market represented 348 milliontonnes in 2009 (1) (excluding recycled materials)down by 13 % compared to 2008, from the operationof approximately 3,500 quarries. The Group has 63production sites, including 48 quarries, which enabledit to produce and market 10 million tonnes ofaggregates in 2009, i.e. approximately 2.8 % of thenational market (2) . The Group is one of the top tenaggregate producers in France, it being specifiedthat, according to the Group’s estimates, the firsteight producers produce more than 50 % of nationalproduction.The Group’s strategy for its Aggregates business inFrance is to concentrate on the areas where it alreadyhas a presence in the Ready-mixed concrete business.In order to reinforce its Aggregates business,in January 2003 the Group acquired the companyRudigoz, owner of two concrete batching plants andtwo quarries in the Rhône-Alpes area and in 2004 thecompany Matériaux SA, based in eastern France.In 2009, the Group’s Aggregates business in Francefell by 21.8 % (compared with a production of nearly12.8 million tonnes in 2008) with a drop that affectedall regions.(b) United StatesThe American market for ready-mixed concretewas estimated at approximately 203 million m 3 for2009 (3) . Ready-mixed concrete is widely used in theUnited States. The drop in this market acceleratedin 2009 due to the more marked residential marketcrisis and the beginning of a slowdown in the privatenon-residential market. Consequently, 2009 suffereda 24 % decline at national level, after a drop of 15 %in 2008. As a result, the market has remained highlycompetitive with both large and strongly integratedplayers, such as Cemex or Lafarge being present, butmany small independent producers still being activeat the local level as well.The Group operates 47 concrete batching plants in theUnited States, in the two areas where it is established.These produced an overall output of slightly morethan 1.4 million m 3 in 2009 (of which 73 % in Californiaand 27 % in Alabama) retreating by 33 % by comparisonwith global production in 2008 (2.1 million m 3 ).Development of the Group’s sales volumes varies onthe basis of regions and is determined by the residentialmarket. Given the size of the American market,only the two regional markets on which the Group isestablished are discussed below.In May 2008, the Group acquired a major ready-mixedconcrete facility near Atlanta, thereby strengtheningits vertical integration in the South-East, in particularwith a view to build the new Ragland kiln. The Walkergroup facility is located in an important market, southof Atlanta, that is driven in the long term by stronggrowth in this city’s population. The facility purchasedhas 14 concrete batching plants spread over ninesites that have a production capacity in the range of700,000 m 3 and represent 200,000 tonnes of cementconsumption potential.The ready-mixed concrete market in which the Groupis active in the South-East, i.e. Alabama and Georgia,accounted for a production of almost 8.3 million m 3in 2009, which represents a decline of 37 % comparedto 2008 (4) .The ready-mixed concrete market in California accountedfor a production of 18.2 million m 3 in 2009,a steep fall of 30.8 % compared with the previousyear because of a considerable fall in residentialconstruction (5) .(c) SwitzerlandThe ready-mixed concrete market in Switzerland hasexperienced 4.3 % annual average growth since 2004and stability since 2006, according to the latest estimatesfrom the ERMCO (6) . Consumption declined in2002 and 2003, before increasing in 2004 with build-(1)Source : National Union of Quarries and Materials (Unicem), 2009(2)Source : Unicem, 2009(3) (4) (5)Source : National Ready Mix Concrete Association, 2009(6)European Ready Mixed Concrete Organization (Bruxelles),20092009 registration document - VICAT 51