6 - Vicat

6 - Vicat

6 - Vicat

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

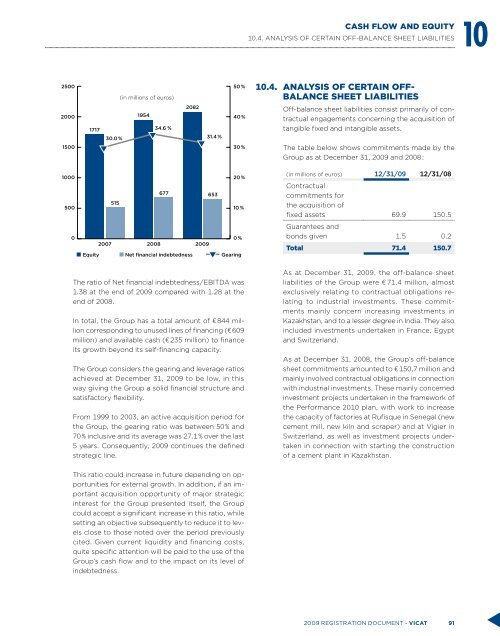

CASH FLOW AND EQUITY1010.4. ANALYSIS OF CERTAIN OFF-BALANCE SHEET LIABILITIES2500(in millions of euros)50 %10.4. ANALYSIS OF CERTAIN OFF-BALANCE SHEET LIABILITIES200015001717195434.6 %30.0 %208231.4 %40 %30 %Off-balance sheet liabilities consist primarily of contractualengagements concerning the acquisition oftangible fixed and intangible assets.The table below shows commitments made by theGroup as at December 31, 2009 and 2008 :1000500020 %67765351510 %0 %20072008 2009Equity Net financial indebtedness Gearing(in millions of euros) 12/31/09 12/31/08Contractualcommitments forthe acquisition offixed assets 69.9 150.5Guarantees andbonds given 1.5 0.2Total 71.4 150.7The ratio of Net financial indebtedness/EBITDA was1.38 at the end of 2009 compared with 1.28 at theend of 2008.In total, the Group has a total amount of € 844 millioncorresponding to unused lines of financing (€ 609million) and available cash (€ 235 million) to financeits growth beyond its self-financing capacity.The Group considers the gearing and leverage ratiosachieved at December 31, 2009 to be low, in thisway giving the Group a solid financial structure andsatisfactory flexibility.From 1999 to 2003, an active acquisition period forthe Group, the gearing ratio was between 50 % and70 % inclusive and its average was 27.1 % over the last5 years. Consequently, 2009 continues the definedstrategic line.As at December 31, 2009, the off-balance sheetliabilities of the Group were € 71.4 million, almostexclusively relating to contractual obligations relatingto industrial investments. These commitmentsmainly concern increasing investments inKazakhstan, and to a lesser degree in India. They alsoincluded investments undertaken in France, Egyptand Switzerland.As at December 31, 2008, the Group’s off-balancesheet commitments amounted to € 150,7 million andmainly involved contractual obligations in connectionwith industrial investments. These mainly concernedinvestment projects undertaken in the framework ofthe Performance 2010 plan, with work to increasethe capacity of factories at Rufisque in Senegal (newcement mill, new kiln and scraper) and at Vigier inSwitzerland, as well as investment projects undertakenin connection with starting the constructionof a cement plant in Kazakhstan.This ratio could increase in future depending on opportunitiesfor external growth. In addition, if an importantacquisition opportunity of major strategicinterest for the Group presented itself, the Groupcould accept a significant increase in this ratio, whilesetting an objective subsequently to reduce it to levelsclose to those noted over the period previouslycited. Given current liquidity and financing costs,quite specific attention will be paid to the use of theGroup’s cash flow and to the impact on its level ofindebtedness.2009 registration document - VICAT 91