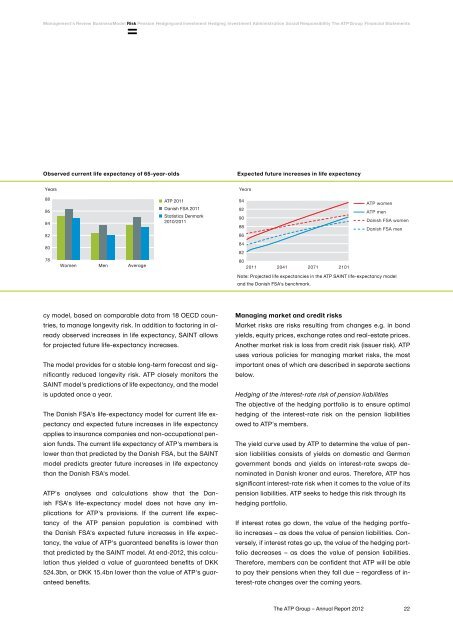

Management's Review Business Model Risk Pension Hedging and investment Hedging Investment Administration Social Responsibility <strong>The</strong> <strong>ATP</strong> <strong>Group</strong> Financial StatementsObserved current life expectancy of 65-year-oldsExpected future increases in life expectancyYearsYears88868482<strong>ATP</strong> 2011Danish FSA 2011Statistics Denmark2010/20119492908886<strong>ATP</strong> women<strong>ATP</strong> menDanish FSA womenDanish FSA men8078Women Men Average8482802011 2041 2071 2101Note: Projected life expectancies in the <strong>ATP</strong> SAINT life-expectancy modeland the Danish FSA's benchmark.cy model, based on comparable data from 18 OECD countries,to manage longevity risk. In addition to factoring in alreadyobserved increases in life expectancy, SAINT allowsfor projected future life-expectancy increases.<strong>The</strong> model provides for a stable long-term forecast and significantlyreduced longevity risk. <strong>ATP</strong> closely monitors theSAINT model's predictions of life expectancy, and the modelis updated once a year.<strong>The</strong> Danish FSA's life-expectancy model for current life expectancyand expected future increases in life expectancyapplies to insurance companies and non-occupational pensionfunds. <strong>The</strong> current life expectancy of <strong>ATP</strong>'s members islower than that predicted by the Danish FSA, but the SAINTmodel predicts greater future increases in life expectancythan the Danish FSA's model.<strong>ATP</strong>'s analyses and calculations show that the DanishFSA's life-expectancy model does not have any implicationsfor <strong>ATP</strong>'s provisions. If the current life expectancyof the <strong>ATP</strong> pension population is combined withthe Danish FSA's expected future increases in life expectancy,the value of <strong>ATP</strong>'s guaranteed benefits is lower thanthat predicted by the SAINT model. At end-<strong>2012</strong>, this calculationthus yielded a value of guaranteed benefits of DKK524.3bn, or DKK 15.4bn lower than the value of <strong>ATP</strong>'s guaranteedbenefits.Managing market and credit risksMarket risks are risks resulting from changes e.g. in bondyields, equity prices, exchange rates and real-estate prices.Another market risk is loss from credit risk (issuer risk). <strong>ATP</strong>uses various policies for managing market risks, the mostimportant ones of which are described in separate sectionsbelow.Hedging of the interest-rate risk of pension liabilities<strong>The</strong> objective of the hedging portfolio is to ensure optimalhedging of the interest-rate risk on the pension liabilitiesowed to <strong>ATP</strong>'s members.<strong>The</strong> yield curve used by <strong>ATP</strong> to determine the value of pensionliabilities consists of yields on domestic and Germangovernment bonds and yields on interest-rate swaps denominatedin Danish kroner and euros. <strong>The</strong>refore, <strong>ATP</strong> hassignificant interest-rate risk when it comes to the value of itspension liabilities. <strong>ATP</strong> seeks to hedge this risk through itshedging portfolio.If interest rates go down, the value of the hedging portfolioincreases – as does the value of pension liabilities. Conversely,if interest rates go up, the value of the hedging portfoliodecreases – as does the value of pension liabilities.<strong>The</strong>refore, members can be confident that <strong>ATP</strong> will be ableto pay their pensions when they fall due – regardless of interest-ratechanges over the coming years.<strong>The</strong> <strong>ATP</strong> <strong>Group</strong> – <strong>Annual</strong> <strong>Report</strong> <strong>2012</strong>22

Management's Review Business Model Risk Pension Hedging and investment Hedging Investment Administration Social Responsibility <strong>The</strong> <strong>ATP</strong> <strong>Group</strong> Financial StatementsPotential losses in the five risk classesDKK billion Sensitivity <strong>2012</strong> excl. Sensitivity <strong>2012</strong> incl. Sensitivity 2011 incl.tail-risk hedging tail-risk hedging tail-risk hedgingRisk classEventInterest Rates Interest rates +1.5% 0.4 0.4 4.7Credit Credit spread +7% 10.9 10.9 11.3Equities Equities -50% 22.9 18.1 10.2Inflation Real interest rate + 2.0%¹ 11.1 6.5 7.8Commodities Commodities -65% 4.8 4.8 3.01) <strong>The</strong> real interest rate increase of +2% is calculated as a change in inflation of -1.0% and a change in interest rates of + 1.0%.Risk diversificationIn its efforts to achieve returns, <strong>ATP</strong> systematically incursmarket risks through investment in different asset types. Inorder to diversify market risks, the assets of the investmentportfolio are invested in five risk classes with very differentrisk profiles. <strong>The</strong> Supervisory Board has established aframework for the distribution of assets.Protection against sharply falling values<strong>ATP</strong> focuses on protecting itself against 'tail risks', i.e. sharpdrops in the value of the investment portfolio, e.g. a 30-percentplunge in equity or commodity prices.'Tail risks' represent a significant risk to <strong>ATP</strong>, and therefore<strong>ATP</strong> hedges against heavy losses if these very negativeevents were to occur.However, the purchase of hedging directly reduces the investmentreturn. This has prompted the Supervisory Boardto set a framework and limits for this type of risk hedging.In <strong>2012</strong>, <strong>ATP</strong> hedged against heavy losses from falling equityprices, rising inflation and lower oil prices.Liquidity managementLike all other pension providers, <strong>ATP</strong> faces new challengesin terms of ensuring adequate liquidity. New regulations,setting out requirements for central clearing of value changesfor certain types of financial instruments, tighten investorliquidity requirements. Moreover, pension payouts exceedcontributions because <strong>ATP</strong> is a "mature" pension fund.In <strong>2012</strong>, this prompted the <strong>ATP</strong> Supervisory Board to adopta new liquidity management model, placing limits on theamount of liquidity <strong>ATP</strong> must be able to muster both in theshort term (five days) and in the long term (one year) relativeto different scenarios.Increased focus on counterparty risks<strong>The</strong> use of financial instruments, e.g. in the interest-ratehedging programme, represents a separate risk to <strong>ATP</strong>,since changes in the value of these instruments will generatea liability and a receivable between <strong>ATP</strong> and its counterparties.<strong>The</strong>refore, <strong>ATP</strong> may suffer a loss if the counterpartydefaults. In order to reduce this counterparty risk, both<strong>ATP</strong> and its counterparties require that an agreement oncollateral be concluded on receivables from the other party.For instance, <strong>ATP</strong> is to provide more collateral if interestrates go up and receive more collateral if interest rates godown. Only liquid assets, such as government bonds, canbe pledged as collateral for these contracts. For most ofits counterparties, <strong>ATP</strong> has introduced restrictions on thebonds eligible as collateral. Only domestic government andmortgage bonds, US government bonds and governmentbonds issued by eurozone countries with high credit ratingsare eligible as collateral.Operational risksOperational risks are e.g. the risk of loss arising from theoperational performance of the <strong>Group</strong>'s business. <strong>The</strong> mostsignificant operational risks are assessed as being errorsor delays in bulk disbursements and processing, for exampleerrors in calculation and payment systems, errors in col-<strong>The</strong> <strong>ATP</strong> <strong>Group</strong> – <strong>Annual</strong> <strong>Report</strong> <strong>2012</strong>23