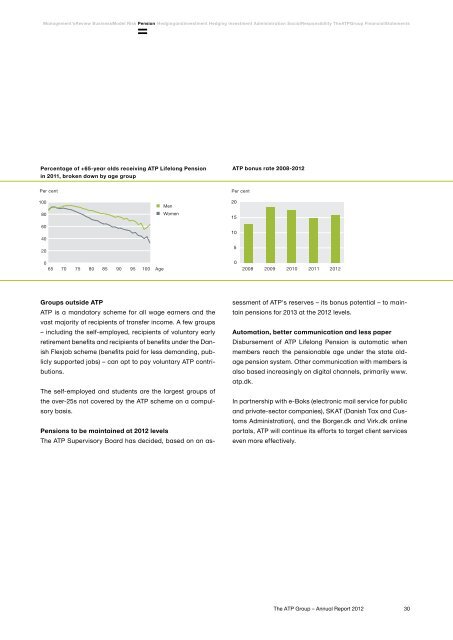

Management's Review Business Model Risk Pension Hedging and investment Hedging Investment Administration Social Responsibility <strong>The</strong> <strong>ATP</strong> <strong>Group</strong> Financial StatementsPercentage of +65-year olds receiving <strong>ATP</strong> Lifelong Pensionin 2011, broken down by age group<strong>ATP</strong> bonus rate 2008-<strong>2012</strong>Per centPer cent10080604020MenWomen2015105065 70 75 80 85 90 95 100 Age02008 2009 2010 2011 <strong>2012</strong><strong>Group</strong>s outside <strong>ATP</strong><strong>ATP</strong> is a mandatory scheme for all wage earners and thevast majority of recipients of transfer income. A few groups– including the self-employed, recipients of voluntary earlyretirement benefits and recipients of benefits under the DanishFlexjob scheme (benefits paid for less demanding, publiclysupported jobs) – can opt to pay voluntary <strong>ATP</strong> contributions.<strong>The</strong> self-employed and students are the largest groups ofthe over-25s not covered by the <strong>ATP</strong> scheme on a compulsorybasis.Pensions to be maintained at <strong>2012</strong> levels<strong>The</strong> <strong>ATP</strong> Supervisory Board has decided, based on an assessmentof <strong>ATP</strong>'s reserves – its bonus potential – to maintainpensions for 2013 at the <strong>2012</strong> levels.Automation, better communication and less paperDisbursement of <strong>ATP</strong> Lifelong Pension is automatic whenmembers reach the pensionable age under the state oldagepension system. Other communication with members isalso based increasingly on digital channels, primarily www.atp.dk.In partnership with e-Boks (electronic mail service for publicand private-sector companies), SKAT (Danish Tax and CustomsAdministration), and the Borger.dk and Virk.dk onlineportals, <strong>ATP</strong> will continue its efforts to target client serviceseven more effectively.<strong>The</strong> <strong>ATP</strong> <strong>Group</strong> – <strong>Annual</strong> <strong>Report</strong> <strong>2012</strong>30

Management's Review Business Model Risk Pension Hedging and investment Hedging Investment Administration Social Responsibility <strong>The</strong> <strong>ATP</strong> <strong>Group</strong> Financial StatementsImproved offer for disability pensionersPredictable pension, joint asset management and cost effective administrationMember development in <strong>2012</strong>Deposits, contributions and payouts in <strong>2012</strong>NumberDK MillionNumberMembers, beginning of year 96,300Additions- new members 9,400Departures- retired members 4,100- deceased members 1,100Members, end of year 100,500Contributions 1 503Payouts 184- converted to <strong>ATP</strong> 153 4,100- lump-sum benefits on death 31 1,100Total deposits, end of year 2,755 100,5001) After social-security contributions<strong>The</strong> Supplementary Labour Market Pension Scheme forDisability Pensioners (SUPP) offers disability pensionersparticularly attractive opportunities for saving for lifelongretirement. In <strong>2012</strong>, when disability pensioners paid aSUPP contribution of DKK 157 a month, this amount wastopped up by the central government, contributing a furtherDKK 314 a month.Enrolment in the SUPP scheme is voluntary. Just overfour in ten disability pensioners have enrolled in the SUPPscheme at <strong>ATP</strong> and enrolment is increasingPayouts under the scheme totalled DKK 184m in <strong>2012</strong>,DKK 153m of which was converted into <strong>ATP</strong> Lifelong Pension,while DKK 31m was paid out on death.Overhaul of the SUPP schemeSo far, the SUPP scheme has been a purely individual savingsscheme with no insurance elements. Savings underthe scheme were converted into <strong>ATP</strong> Lifelong Pensionwhen the disability pensioner reached retirement age underthe state old-age pension.As of 1 January 2013, the SUPP scheme at <strong>ATP</strong> will belinked more closely to <strong>ATP</strong> Lifelong Pension. At the sametime, SUPP's asset management will be pooled with thatof <strong>ATP</strong>.SUPP members get a predictable, guaranteed old-agepension, which is gradually built up through the accrualprocess. As an added benefit, the closer link to <strong>ATP</strong> willtranslate into lower expenses for SUPP members.As part of the overhaul, individual savings accounts willbe dismantled, and contributions for 2013 onwards will beused to acquire guaranteed lifelong pension rights at <strong>ATP</strong>.Existing individual savings accounts are converted intoguaranteed <strong>ATP</strong> lifelong pension rigths at 1 January 2013.Under the new rules, the period of disbursement on deathwill be extended to five years after the SUPP memberreaches retirement age under the state funded old-agepension. <strong>The</strong> amount to be disbursed is gradually scaleddown from the time the member reaches the retirementage under the state funded old-age pension, and after fiveyears there will be no disbursement. Previously, the estatereceived no disbursement on the death of a SUPP memberover the retirement age under the state funded old-agepension.Independent annual reportFor more information on the SUPP scheme, please refer tothe SUPP annual report at www.atp.dk.<strong>The</strong> <strong>ATP</strong> <strong>Group</strong> – <strong>Annual</strong> <strong>Report</strong> <strong>2012</strong>31