Box 2: On Innovation <strong>and</strong> Innovation SystemsThe European Commission def<strong>in</strong>es <strong>in</strong>novation as “<strong>the</strong> renewal <strong>and</strong> enlargement of <strong>the</strong> rangeof products <strong>and</strong> services <strong>and</strong> <strong>the</strong> associated markets; <strong>the</strong> establishment of new methods ofproduction, supply <strong>and</strong> distribution; <strong>the</strong> <strong>in</strong>troduction of changes <strong>in</strong> management, workorganisation, <strong>and</strong> <strong>the</strong> work<strong>in</strong>g conditions <strong>and</strong> skills of <strong>the</strong> workforce” (European Commission(COM(1995) 688). Traditional perspectives have viewed <strong>in</strong>novation as closely related toscience <strong>and</strong> technology. In practice, however, <strong>in</strong>novation can take many forms, <strong>in</strong>clud<strong>in</strong>gcommercialisation of science <strong>and</strong> technology as well as <strong>the</strong> development <strong>and</strong> implementationof new ideas more generally, as <strong>in</strong> <strong>the</strong> form of organizational change or <strong>in</strong>vent<strong>in</strong>g new ways ofdo<strong>in</strong>g th<strong>in</strong>gs.Ra<strong>the</strong>r than be<strong>in</strong>g a one-dimensional, l<strong>in</strong>ear process lead<strong>in</strong>g from certa<strong>in</strong> <strong>in</strong>put factors,<strong>in</strong>novation is <strong>the</strong> result of efforts by multiple actors, <strong>and</strong> is enhanced by <strong>the</strong>ir constructive<strong>in</strong>teractions. The concept of <strong>in</strong>novation has evolved from a l<strong>in</strong>ear model hav<strong>in</strong>g R&D as <strong>the</strong>start<strong>in</strong>g po<strong>in</strong>t, to <strong>the</strong> systemic model <strong>in</strong> which <strong>in</strong>novation arises from complex <strong>in</strong>teractionsbetween <strong>in</strong>dividuals, organisations <strong>and</strong> <strong>the</strong>ir operat<strong>in</strong>g environment (European Commission2003k). The notion of <strong>in</strong>novation system aims to broaden <strong>the</strong> scope of <strong>the</strong> policymaker toencompass <strong>the</strong> factors <strong>and</strong> reforms that may be most important for free<strong>in</strong>g up <strong>the</strong> potentialfor <strong>in</strong>novation, irrespective of <strong>in</strong> which policy doma<strong>in</strong> <strong>the</strong>y are found. Fur<strong>the</strong>rmore, <strong>the</strong> term‘<strong>in</strong>novation system’ has emerged to capture <strong>the</strong> <strong>in</strong>terrelated role of different actors, markets <strong>and</strong><strong>in</strong>stitutions (Andersson et. al. (2004a), p.19).Based on <strong>the</strong> <strong>in</strong>novation system approach, <strong>in</strong>novation policy is a horizontal policy approachencompass<strong>in</strong>g a wide range of areas <strong>and</strong> <strong>in</strong>struments that cut across traditional policy doma<strong>in</strong>s.Areas that could be mentioned <strong>in</strong> this context are taxation <strong>and</strong> <strong>in</strong>centive structures, ICT access<strong>and</strong> penetration, R&D <strong>in</strong>vestment <strong>and</strong> commercialization, networks <strong>and</strong> cluster<strong>in</strong>g, bus<strong>in</strong>essenvironment, technology upgrad<strong>in</strong>g, foreign direct <strong>in</strong>vestment, education, attitudes <strong>and</strong> socialcapital, etc. (see also figure below).Innovation System ModelDem<strong>and</strong>Consumers (f<strong>in</strong>al dem<strong>and</strong>)Producers (<strong>in</strong>termediate dem<strong>and</strong>)Framework ConditionsF<strong>in</strong>ancial enviroment; taxation <strong>and</strong><strong>in</strong>centives; propensity to <strong>in</strong>novation<strong>and</strong> entrepreneurship; mobilityIndustrialSystemEducation <strong>and</strong>Research SystemPoliticalSystemLarge companiesProffessionaleducation, tra<strong>in</strong><strong>in</strong>gGovernmentMature <strong>SMEs</strong>IntermediariesResearch<strong>in</strong>stitutes;BrokersHigher education<strong>and</strong> researchGovernanceNew, technologybasedfirmsPublic ssectorresearchRTD policiesInfrastructureBank<strong>in</strong>g,venture capitalIPR <strong>and</strong><strong>in</strong>formationInnovation <strong>and</strong>bus<strong>in</strong>ess reportStanards <strong>and</strong>normsSource: Arnold, Kuhlman, van der Meulen (2001)20

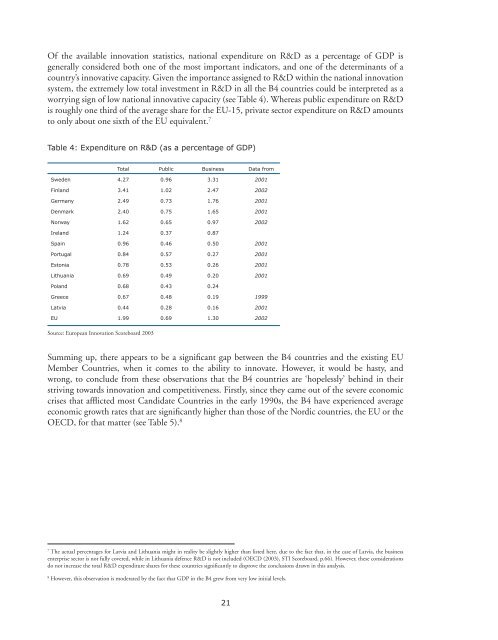

Of <strong>the</strong> available <strong>in</strong>novation statistics, national expenditure on R&D as a percentage of GDP isgenerally considered both one of <strong>the</strong> most important <strong>in</strong>dicators, <strong>and</strong> one of <strong>the</strong> determ<strong>in</strong>ants of acountry’s <strong>in</strong>novative capacity. Given <strong>the</strong> importance assigned to R&D with<strong>in</strong> <strong>the</strong> national <strong>in</strong>novationsystem, <strong>the</strong> extremely low total <strong>in</strong>vestment <strong>in</strong> R&D <strong>in</strong> all <strong>the</strong> B4 countries could be <strong>in</strong>terpreted as aworry<strong>in</strong>g sign of low national <strong>in</strong>novative capacity (see Table 4). Whereas public expenditure on R&Dis roughly one third of <strong>the</strong> average share for <strong>the</strong> EU-15, private sector expenditure on R&D amountsto only about one sixth of <strong>the</strong> EU equivalent. 7Table 4: Expenditure on R&D (as a percentage of GDP)Total Public Bus<strong>in</strong>ess Data fromSweden 4.27 0.96 3.31 2001F<strong>in</strong>l<strong>and</strong> 3.41 1.02 2.47 2002Germany 2.49 0.73 1.76 2001Denmark 2.40 0.75 1.65 2001Norway 1.62 0.65 0.97 2002Irel<strong>and</strong> 1.24 0.37 0.87Spa<strong>in</strong> 0.96 0.46 0.50 2001Portugal 0.84 0.57 0.27 2001Estonia 0.78 0.53 0.26 2001Lithuania 0.69 0.49 0.20 2001Pol<strong>and</strong> 0.68 0.43 0.24Greece 0.67 0.48 0.19 1999Latvia 0.44 0.28 0.16 2001EU 1.99 0.69 1.30 2002Source: European Innovation Scoreboard 2003Summ<strong>in</strong>g up, <strong>the</strong>re appears to be a significant gap between <strong>the</strong> B4 countries <strong>and</strong> <strong>the</strong> exist<strong>in</strong>g EUMember Countries, when it comes to <strong>the</strong> ability to <strong>in</strong>novate. However, it would be hasty, <strong>and</strong>wrong, to conclude from <strong>the</strong>se observations that <strong>the</strong> B4 countries are ‘hopelessly’ beh<strong>in</strong>d <strong>in</strong> <strong>the</strong>irstriv<strong>in</strong>g towards <strong>in</strong>novation <strong>and</strong> competitiveness. Firstly, s<strong>in</strong>ce <strong>the</strong>y came out of <strong>the</strong> severe economiccrises that afflicted most C<strong>and</strong>idate Countries <strong>in</strong> <strong>the</strong> early 1990s, <strong>the</strong> B4 have experienced averageeconomic growth rates that are significantly higher than those of <strong>the</strong> Nordic countries, <strong>the</strong> EU or <strong>the</strong>OECD, for that matter (see Table 5). 87The actual percentages for Latvia <strong>and</strong> Lithuania might <strong>in</strong> reality be slightly higher than listed here, due to <strong>the</strong> fact that, <strong>in</strong> <strong>the</strong> case of Latvia, <strong>the</strong> bus<strong>in</strong>essenterprise sector is not fully covered, while <strong>in</strong> Lithuania defence R&D is not <strong>in</strong>cluded (OECD (2003), STI Scoreboard, p.66). However, <strong>the</strong>se considerationsdo not <strong>in</strong>crease <strong>the</strong> total R&D expenditure shares for <strong>the</strong>se countries significantly to disprove <strong>the</strong> conclusions drawn <strong>in</strong> this analysis.8However, this observation is moderated by <strong>the</strong> fact that GDP <strong>in</strong> <strong>the</strong> B4 grew from very low <strong>in</strong>itial levels.21

- Page 1 and 2: Sylvia Schwaag SergerEmily HanssonC

- Page 4 and 5: About the International Organisatio

- Page 7: PREFACEAccession to the Single Mark

- Page 10 and 11: enterprise development. There are n

- Page 12 and 13: BOXESBox 1: The ‘Knowledge-Based

- Page 15 and 16: INTRODUCTIONAfter more than 10 year

- Page 17 and 18: CHAPTER 1: FROM STABILISATION TO IN

- Page 19: increased competitive pressure as B

- Page 24 and 25: Table 5: GDP Growth 1995-2003 in Se

- Page 26 and 27: Table 7: Relative Strengths and Wea

- Page 28 and 29: Box 3: The Indicator ProblemExistin

- Page 31 and 32: CHAPTER 2:BALTIC SMEs - AGENTS OF F

- Page 33 and 34: Table 9: Average Annual Growth of S

- Page 35 and 36: Box 4: Overview of Selected Multina

- Page 37 and 38: The Role of SMEs in Transitional Ec

- Page 39 and 40: e to the potential advantage of the

- Page 41 and 42: A common measurement of business ac

- Page 43 and 44: Figure 8: Labour Productivity per P

- Page 45 and 46: Figure 10: Employment in Med/Hi-tec

- Page 47 and 48: Summing up, there are fewer economi

- Page 49 and 50: Overall, SMEs tend to lack the fina

- Page 51 and 52: Figure 12: Enterprises with Innovat

- Page 53 and 54: Figure 14: Proportion of Enterprise

- Page 55 and 56: Table 14: Barriers to Innovation fo

- Page 57 and 58: Some interesting examples of cluste

- Page 59 and 60: CHAPTER 3:POLICIES PROMOTING SMEs A

- Page 61 and 62: National governments themselves wil

- Page 63 and 64: Institutional StructureIn all of th

- Page 65 and 66: EU countries (innovation relay cent

- Page 67 and 68: LITHUANIAAgency/OrganisationLithuan

- Page 69 and 70: From the private sector, the chambe

- Page 71 and 72: On the whole, the B4 have relativel

- Page 73 and 74:

LITHUANIAProgramme/Policy DocumentI

- Page 75 and 76:

Table 19: B4 National Rankings of A

- Page 77 and 78:

Box 11: Structural Funds to the Can

- Page 79 and 80:

Box 12: On SMEs and FinancingIt doe

- Page 81 and 82:

examples of evaluations of national

- Page 83 and 84:

CHAPTER 4:CHALLENGES AND RECOMMENDA

- Page 85 and 86:

General challengesBased on our own

- Page 87 and 88:

the above-mentioned channels. 27 On

- Page 89 and 90:

the EU average and particularly wit

- Page 91 and 92:

RecommendationsBased on the challen

- Page 93 and 94:

CHAPTER 5:A VISION OF A NORDIC-BALT

- Page 95 and 96:

addition, they are the most advance

- Page 97 and 98:

countries. One such sign is the rap

- Page 99 and 100:

CONCLUSIONSEU accession will not re

- Page 101 and 102:

REFERENCESAlfonso, Antonio, Ludger

- Page 103 and 104:

European Commission (2003f), Compre

- Page 105 and 106:

Eurostat (2004a), SMEs in the Candi

- Page 107 and 108:

Statistical Office of Estonia (2004

- Page 109 and 110:

APPENDIX I:Agenda for Working Group

- Page 111 and 112:

DAY 2:POLICY SOLUTIONS9:30-10:30 In

- Page 113 and 114:

APPENDIX II:Participants in the IKE

- Page 115 and 116:

APPENDIX III:Conclusions from the I

- Page 117 and 118:

APPENDIX IV:Summary of the Panel se

- Page 119 and 120:

Regarding the role of policymaking,

- Page 121 and 122:

APPENDIX V:Description of Field Stu

- Page 123 and 124:

Mr. Miroslaw MarekMr. Talis Millers

- Page 126:

IKED - International Organisation f