Figure 9: Structure of Gross Value-Added by Sector 19 , Trends for B4 Countries100%90%80%70%60%50%40%30%20%10%0%ESTONIAStructure of Gross Value-Added by Sector(% of total, by NACE classification)31,8 32,8 33,6 32,91999 2000 2001 2002100%90%80%70%60%50%40%30%20%10%0%LATVIAStructure of Gross Value-Added by Sector(% of total, by NACE classification)31 32,4 32,8 31,41999 2000 2001 2002Services Agricultural Industry Construction Trade O<strong>the</strong>r ActivitiesServices Agricultural Industry Construction Trade O<strong>the</strong>r Activities100%90%80%70%60%50%40%30%20%10%0%LITHUANIAStructure of Gross Value-Added by Sector(% of total, by NACE classification)23 24,7 24,8 261999 2000 2001 2002100%90%80%70%60%50%40%30%20%10%0%POLANDStructure of Gross Value-Added by Sector(% of total, by NACE classification)22,1 22,8 23,9 24,31999 2000 2001 2002Services Agricultural Industry Construction Trade O<strong>the</strong>r ActivitiesServices Agricultural Industry Construction Trade O<strong>the</strong>r ActivitiesSource: Romanian National Institute of Statistics, (2003)<strong>SMEs</strong> are most prom<strong>in</strong>ent with<strong>in</strong> <strong>the</strong> trade sector, although lately <strong>the</strong>ir presence <strong>the</strong>re has beenshr<strong>in</strong>k<strong>in</strong>g (Figure 11). Without more detailed data <strong>and</strong> careful exam<strong>in</strong>ation, it is difficult to drawconclusions as to <strong>the</strong> implications of <strong>the</strong> sectoral make-up of <strong>SMEs</strong> <strong>in</strong> <strong>the</strong> B4. In considerationof <strong>the</strong> fact that employment <strong>in</strong> <strong>the</strong> B4 countries is, on average, less high-tech <strong>in</strong>tensive <strong>in</strong> bothmanufactur<strong>in</strong>g <strong>and</strong> services than <strong>in</strong> <strong>the</strong> EU (see Figure 10), an exclusive high-tech focus would clearlybe <strong>in</strong>appropriate. One of <strong>the</strong> big challenges <strong>in</strong> policymak<strong>in</strong>g is <strong>the</strong> question of whe<strong>the</strong>r it is possibleto gauge <strong>in</strong> which areas <strong>the</strong> development potential of <strong>SMEs</strong> would be <strong>the</strong> greatest or, even morespecifically, <strong>in</strong> which area support of <strong>SMEs</strong> might render <strong>the</strong> greatest social benefits.19For comparison purposes, sectors have been def<strong>in</strong>ed us<strong>in</strong>g <strong>the</strong> follow<strong>in</strong>g NACE classification group<strong>in</strong>gs: Agricultural (A,B), Industry (C,D,E), Construction(F), Trade (G), Services (H,I,J,K), O<strong>the</strong>r Activities (L,M,N,O,P,Q).42

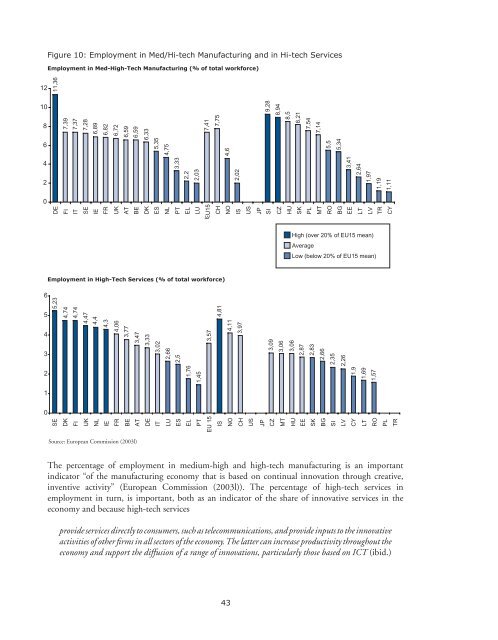

Figure 10: Employment <strong>in</strong> Med/Hi-tech Manufactur<strong>in</strong>g <strong>and</strong> <strong>in</strong> Hi-tech ServicesEmployment <strong>in</strong> Med-High-Tech Manufactur<strong>in</strong>g (% of total workforce)1210864206Employment <strong>in</strong> High-Tech Services (% of total workforce)543210Source: European Commission (2003l)The percentage of employment <strong>in</strong> medium-high <strong>and</strong> high-tech manufactur<strong>in</strong>g is an important<strong>in</strong>dicator “of <strong>the</strong> manufactur<strong>in</strong>g economy that is based on cont<strong>in</strong>ual <strong>in</strong>novation through creative,<strong>in</strong>ventive activity” (European Commission (2003l)). The percentage of high-tech services <strong>in</strong>employment <strong>in</strong> turn, is important, both as an <strong>in</strong>dicator of <strong>the</strong> share of <strong>in</strong>novative services <strong>in</strong> <strong>the</strong>economy <strong>and</strong> because high-tech servicesprovide services directly to consumers, such as telecommunications, <strong>and</strong> provide <strong>in</strong>puts to <strong>the</strong> <strong>in</strong>novativeactivities of o<strong>the</strong>r firms <strong>in</strong> all sectors of <strong>the</strong> economy. The latter can <strong>in</strong>crease productivity throughout <strong>the</strong>economy <strong>and</strong> support <strong>the</strong> diffusion of a range of <strong>in</strong>novations, particularly those based on ICT (ibid.)43

- Page 1 and 2: Sylvia Schwaag SergerEmily HanssonC

- Page 4 and 5: About the International Organisatio

- Page 7: PREFACEAccession to the Single Mark

- Page 10 and 11: enterprise development. There are n

- Page 12 and 13: BOXESBox 1: The ‘Knowledge-Based

- Page 15 and 16: INTRODUCTIONAfter more than 10 year

- Page 17 and 18: CHAPTER 1: FROM STABILISATION TO IN

- Page 19: increased competitive pressure as B

- Page 22 and 23: Box 2: On Innovation and Innovation

- Page 24 and 25: Table 5: GDP Growth 1995-2003 in Se

- Page 26 and 27: Table 7: Relative Strengths and Wea

- Page 28 and 29: Box 3: The Indicator ProblemExistin

- Page 31 and 32: CHAPTER 2:BALTIC SMEs - AGENTS OF F

- Page 33 and 34: Table 9: Average Annual Growth of S

- Page 35 and 36: Box 4: Overview of Selected Multina

- Page 37 and 38: The Role of SMEs in Transitional Ec

- Page 39 and 40: e to the potential advantage of the

- Page 41 and 42: A common measurement of business ac

- Page 43: Figure 8: Labour Productivity per P

- Page 47 and 48: Summing up, there are fewer economi

- Page 49 and 50: Overall, SMEs tend to lack the fina

- Page 51 and 52: Figure 12: Enterprises with Innovat

- Page 53 and 54: Figure 14: Proportion of Enterprise

- Page 55 and 56: Table 14: Barriers to Innovation fo

- Page 57 and 58: Some interesting examples of cluste

- Page 59 and 60: CHAPTER 3:POLICIES PROMOTING SMEs A

- Page 61 and 62: National governments themselves wil

- Page 63 and 64: Institutional StructureIn all of th

- Page 65 and 66: EU countries (innovation relay cent

- Page 67 and 68: LITHUANIAAgency/OrganisationLithuan

- Page 69 and 70: From the private sector, the chambe

- Page 71 and 72: On the whole, the B4 have relativel

- Page 73 and 74: LITHUANIAProgramme/Policy DocumentI

- Page 75 and 76: Table 19: B4 National Rankings of A

- Page 77 and 78: Box 11: Structural Funds to the Can

- Page 79 and 80: Box 12: On SMEs and FinancingIt doe

- Page 81 and 82: examples of evaluations of national

- Page 83 and 84: CHAPTER 4:CHALLENGES AND RECOMMENDA

- Page 85 and 86: General challengesBased on our own

- Page 87 and 88: the above-mentioned channels. 27 On

- Page 89 and 90: the EU average and particularly wit

- Page 91 and 92: RecommendationsBased on the challen

- Page 93 and 94: CHAPTER 5:A VISION OF A NORDIC-BALT

- Page 95 and 96:

addition, they are the most advance

- Page 97 and 98:

countries. One such sign is the rap

- Page 99 and 100:

CONCLUSIONSEU accession will not re

- Page 101 and 102:

REFERENCESAlfonso, Antonio, Ludger

- Page 103 and 104:

European Commission (2003f), Compre

- Page 105 and 106:

Eurostat (2004a), SMEs in the Candi

- Page 107 and 108:

Statistical Office of Estonia (2004

- Page 109 and 110:

APPENDIX I:Agenda for Working Group

- Page 111 and 112:

DAY 2:POLICY SOLUTIONS9:30-10:30 In

- Page 113 and 114:

APPENDIX II:Participants in the IKE

- Page 115 and 116:

APPENDIX III:Conclusions from the I

- Page 117 and 118:

APPENDIX IV:Summary of the Panel se

- Page 119 and 120:

Regarding the role of policymaking,

- Page 121 and 122:

APPENDIX V:Description of Field Stu

- Page 123 and 124:

Mr. Miroslaw MarekMr. Talis Millers

- Page 126:

IKED - International Organisation f