ipsas 29—financial instruments: recognition and measurement - IFAC

ipsas 29—financial instruments: recognition and measurement - IFAC

ipsas 29—financial instruments: recognition and measurement - IFAC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT<br />

illustrations as of the expected date of the forecast transaction immediately before the<br />

forecast transaction, i.e., at the beginning of Period 2. If the assessment of hedge<br />

effectiveness is done before the forecast transaction occurs, the difference should be<br />

discounted to the current date to arrive at the actual amount of ineffectiveness. For<br />

example, if the <strong>measurement</strong> date were one month after the hedging relationship was<br />

established <strong>and</strong> the forecast transaction is now expected to occur in two months, the<br />

amount would have to be discounted for the remaining two months before the forecast<br />

transaction is expected to occur to arrive at the actual fair value. This step would not be<br />

necessary in the examples provided above because there was no ineffectiveness.<br />

Therefore, additional discounting of the amounts, which net to zero, would not have<br />

changed the result.<br />

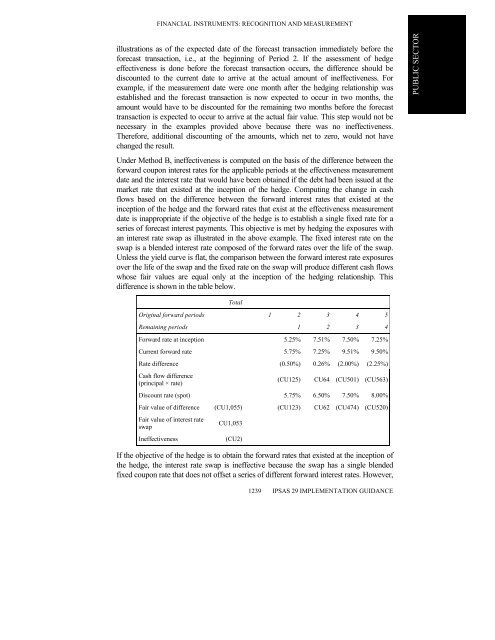

Under Method B, ineffectiveness is computed on the basis of the difference between the<br />

forward coupon interest rates for the applicable periods at the effectiveness <strong>measurement</strong><br />

date <strong>and</strong> the interest rate that would have been obtained if the debt had been issued at the<br />

market rate that existed at the inception of the hedge. Computing the change in cash<br />

flows based on the difference between the forward interest rates that existed at the<br />

inception of the hedge <strong>and</strong> the forward rates that exist at the effectiveness <strong>measurement</strong><br />

date is inappropriate if the objective of the hedge is to establish a single fixed rate for a<br />

series of forecast interest payments. This objective is met by hedging the exposures with<br />

an interest rate swap as illustrated in the above example. The fixed interest rate on the<br />

swap is a blended interest rate composed of the forward rates over the life of the swap.<br />

Unless the yield curve is flat, the comparison between the forward interest rate exposures<br />

over the life of the swap <strong>and</strong> the fixed rate on the swap will produce different cash flows<br />

whose fair values are equal only at the inception of the hedging relationship. This<br />

difference is shown in the table below.<br />

Total<br />

Original forward periods 1 2 3 4 5<br />

Remaining periods 1 2 3 4<br />

Forward rate at inception 5.25% 7.51% 7.50% 7.25%<br />

Current forward rate 5.75% 7.25% 9.51% 9.50%<br />

Rate difference (0.50%) 0.26% (2.00%) (2.25%)<br />

Cash flow difference<br />

(principal × rate)<br />

1239<br />

(CU125) CU64 (CU501) (CU563)<br />

Discount rate (spot) 5.75% 6.50% 7.50% 8.00%<br />

Fair value of difference (CU1,055) (CU123) CU62 (CU474) (CU520)<br />

Fair value of interest rate<br />

swap<br />

CU1,053<br />

Ineffectiveness (CU2)<br />

If the objective of the hedge is to obtain the forward rates that existed at the inception of<br />

the hedge, the interest rate swap is ineffective because the swap has a single blended<br />

fixed coupon rate that does not offset a series of different forward interest rates. However,<br />

IPSAS 29 IMPLEMENTATION GUIDANCE<br />

PUBLIC SECTOR

![International Auditing and Assurance Standards Board [IAASB] - IFAC](https://img.yumpu.com/22522144/1/190x245/international-auditing-and-assurance-standards-board-iaasb-ifac.jpg?quality=85)