The Stakeholder Engagement Manual Volume 2 - AccountAbility

The Stakeholder Engagement Manual Volume 2 - AccountAbility

The Stakeholder Engagement Manual Volume 2 - AccountAbility

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

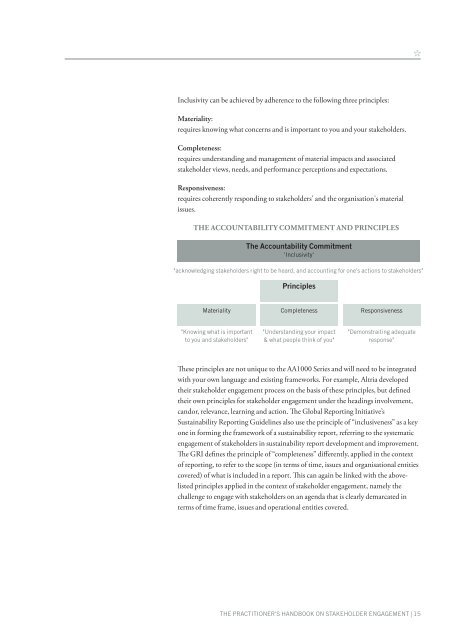

Inclusivity can be achieved by adherence to the following three principles:<br />

Materiality:<br />

requires knowing what concerns and is important to you and your stakeholders.<br />

Completeness:<br />

requires understanding and management of material impacts and associated<br />

stakeholder views, needs, and performance perceptions and expectations.<br />

Responsiveness:<br />

requires coherently responding to stakeholders' and the organisation's material<br />

issues.<br />

THE ACCOUNTABILITY COMMITMENT AND PRINCIPLES<br />

<strong>The</strong> Accountability Commitment<br />

'Inclusivity'<br />

"acknowledging stakeholders right to be heard, and accounting for one's actions to stakeholders"<br />

Principles<br />

Hear that Materiality means: <strong>The</strong> organisation identifi Completeness<br />

es and addresses the most signifi cant Responsiveness<br />

impacts related to<br />

it's business operations and the stratergy, as well as the stakeholders that organisation identifi es and<br />

sddresses the stakeholders with signifi cant potential to infl uence the organisation.<br />

"Knowing what is important "Understanding your impact "Demonstraiting adequate<br />

to you and stakeholders" & what people think of you"<br />

response"<br />

Th ese principles are not unique to the AA1000 Series and will need to be integrated<br />

with your own language and existing frameworks. For example, Altria developed<br />

their stakeholder engagement process on the basis of these principles, but defi ned<br />

their own principles for stakeholder engagement under the headings involvement,<br />

candor, relevance, learning and action. Th e Global Reporting Initiative’s<br />

Sustainability Reporting Guidelines also use the principle of “inclusiveness” as a key<br />

one in forming the framework of a sustainability report, referring to the systematic<br />

engagement of stakeholders in sustainability report development and improvement.<br />

Th e GRI defi nes the principle of “completeness” diff erently, applied in the context<br />

of reporting, to refer to the scope (in terms of time, issues and organisational entities<br />

covered) of what is included in a report. Th is can again be linked with the abovelisted<br />

principles applied in the context of stakeholder engagement, namely the<br />

challenge to engage with stakeholders on an agenda that is clearly demarcated in<br />

terms of time frame, issues and operational entities covered.<br />

THE PRACTITIONER'S HANDBOOK ON STAKEHOLDER ENGAGEMENT | 15