Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

Assessments should be at shorter time intervals, e.g., quarterly, monthly or weekly, in order to<br />

determine weak points <strong>and</strong> to take corrective measures in time. The main inputs of raw <strong>and</strong><br />

auxiliary materials <strong>and</strong> energy as well as the major sources of emissions should be monitored<br />

on a process level.<br />

Site <strong>and</strong> corporate indicators serve as general performance information for management over<br />

a longer period of time <strong>and</strong> for annual reporting for the management review. Site indicators<br />

may also be used for assessing environmental impacts in environmental statements in<br />

accordance with the EU EMAS regulations. Corporate environmental reports include<br />

aggregated indicators on a corporate level.<br />

7.4. The problem of finding a meaningful denominator<br />

Where production output (PO) from the material flow balance does not provide a meaningful<br />

indicator or is not available, or in addition to this denominator, other variables can be used.<br />

Number of employees is a reference often used especially in the service sector.<br />

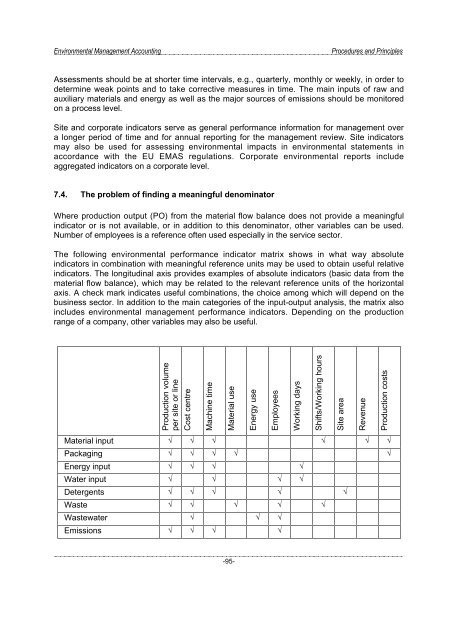

The following environmental performance indicator matrix shows in what way absolute<br />

indicators in combination with meaningful reference units may be used to obtain useful relative<br />

indicators. The longitudinal axis provides examples of absolute indicators (basic data from the<br />

material flow balance), which may be related to the relevant reference units of the horizontal<br />

axis. A check mark indicates useful combinations, the choice among which will depend on the<br />

business sector. In addition to the main categories of the input-output analysis, the matrix also<br />

includes environmental management performance indicators. Depending on the production<br />

range of a company, other variables may also be useful.<br />

Production volume<br />

per site or line<br />

Cost centre<br />

Machine time<br />

Material use<br />

Energy use<br />

Employees<br />

Working days<br />

Shifts/Working hours<br />

Site area<br />

Revenue<br />

Production costs<br />

Material input √ √ √ √ √ √<br />

Packaging √ √ √ √ √<br />

Energy input √ √ √ √<br />

Water input √ √ √ √<br />

Detergents √ √ √ √ √<br />

Waste √ √ √ √ √<br />

Wastewater √ √ √<br />

Emissions √ √ √ √<br />

-95-