Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

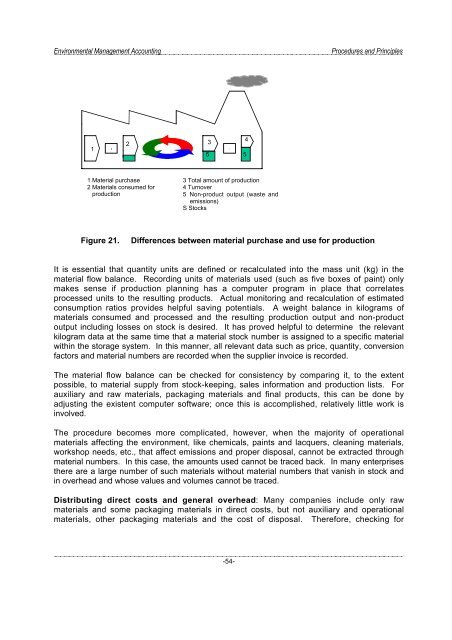

1<br />

S<br />

2 3<br />

4<br />

S<br />

5 5<br />

1 Material purchase<br />

2 Materials consumed for<br />

production<br />

3 Total amount of production<br />

4 Turnover<br />

5 Non-product output (waste <strong>and</strong><br />

emissions)<br />

S Stocks<br />

Figure 21.<br />

Differences between material purchase <strong>and</strong> use for production<br />

It is essential that quantity units are defined or recalculated into the mass unit (kg) in the<br />

material flow balance. Recording units of materials used (such as five boxes of paint) only<br />

makes sense if production planning has a computer program in place that correlates<br />

processed units to the resulting products. Actual monitoring <strong>and</strong> recalculation of estimated<br />

consumption ratios provides helpful saving potentials. A weight balance in kilograms of<br />

materials consumed <strong>and</strong> processed <strong>and</strong> the resulting production output <strong>and</strong> non-product<br />

output including losses on stock is desired. It has proved helpful to determine the relevant<br />

kilogram data at the same time that a material stock number is assigned to a specific material<br />

within the storage system. In this manner, all relevant data such as price, quantity, conversion<br />

factors <strong>and</strong> material numbers are recorded when the supplier invoice is recorded.<br />

The material flow balance can be checked for consistency by comparing it, to the extent<br />

possible, to material supply from stock-keeping, sales information <strong>and</strong> production lists. For<br />

auxiliary <strong>and</strong> raw materials, packaging materials <strong>and</strong> final products, this can be done by<br />

adjusting the existent computer software; once this is accomplished, relatively little work is<br />

involved.<br />

The procedure becomes more complicated, however, when the majority of operational<br />

materials affecting the environment, like chemicals, paints <strong>and</strong> lacquers, cleaning materials,<br />

workshop needs, etc., that affect emissions <strong>and</strong> proper disposal, cannot be extracted through<br />

material numbers. In this case, the amounts used cannot be traced back. In many enterprises<br />

there are a large number of such materials without material numbers that vanish in stock <strong>and</strong><br />

in overhead <strong>and</strong> whose values <strong>and</strong> volumes cannot be traced.<br />

Distributing direct costs <strong>and</strong> general overhead: Many companies include only raw<br />

materials <strong>and</strong> some packaging materials in direct costs, but not auxiliary <strong>and</strong> operational<br />

materials, other packaging materials <strong>and</strong> the cost of disposal. Therefore, checking for<br />

-54-