Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

INPUT in kg/kWh<br />

Raw materials<br />

Auxiliary materials<br />

Packaging<br />

Operating materials<br />

Merch<strong>and</strong>ise<br />

Energy<br />

Gas<br />

Coal<br />

Fuel Oil<br />

Other Fuels<br />

District heat<br />

Renewables (Biomass, Wood)<br />

Solar, Wind, Water<br />

Externally produced electricity<br />

Internally produced electricity<br />

Water<br />

Municipal Water<br />

Ground water<br />

Spring water<br />

Rain/ Surface Water<br />

OUTPUT in kg<br />

Product<br />

Main Product<br />

By Products<br />

Waste<br />

Municipal waste<br />

Recycled waste<br />

Hazardous waste<br />

Waste Water<br />

Amount<br />

Heavy metals<br />

COD<br />

BOD<br />

Air-Emissions<br />

CO2<br />

CO<br />

NOx<br />

SO2<br />

Dust<br />

FCKWs, NH4, VOCs<br />

Ozone depleting substances<br />

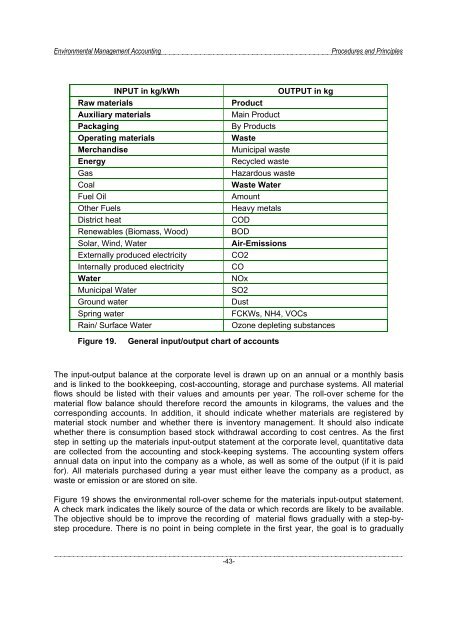

Figure 19.<br />

General input/output chart of accounts<br />

The input-output balance at the corporate level is drawn up on an annual or a monthly basis<br />

<strong>and</strong> is linked to the bookkeeping, cost-accounting, storage <strong>and</strong> purchase systems. All material<br />

flows should be listed with their values <strong>and</strong> amounts per year. The roll-over scheme for the<br />

material flow balance should therefore record the amounts in kilograms, the values <strong>and</strong> the<br />

corresponding accounts. In addition, it should indicate whether materials are registered by<br />

material stock number <strong>and</strong> whether there is inventory management. It should also indicate<br />

whether there is consumption based stock withdrawal according to cost centres. As the first<br />

step in setting up the materials input-output statement at the corporate level, quantitative data<br />

are collected from the accounting <strong>and</strong> stock-keeping systems. The accounting system offers<br />

annual data on input into the company as a whole, as well as some of the output (if it is paid<br />

for). All materials purchased during a year must either leave the company as a product, as<br />

waste or emission or are stored on site.<br />

Figure 19 shows the environmental roll-over scheme for the materials input-output statement.<br />

A check mark indicates the likely source of the data or which records are likely to be available.<br />

The objective should be to improve the recording of material flows gradually with a step-bystep<br />

procedure. There is no point in being complete in the first year, the goal is to gradually<br />

-43-