Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

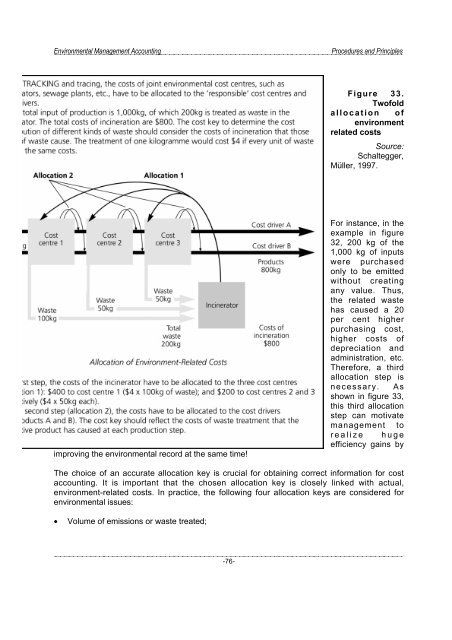

Figure 33.<br />

Twofold<br />

allocation of<br />

environment<br />

related costs<br />

Source:<br />

Schaltegger,<br />

Müller, 1997.<br />

improving the environmental record at the same time!<br />

For instance, in the<br />

example in figure<br />

32, 200 kg of the<br />

1,000 kg of inputs<br />

were purchased<br />

only to be emitted<br />

without creating<br />

any value. Thus,<br />

the related waste<br />

has caused a 20<br />

per cent higher<br />

purchasing cost,<br />

higher costs of<br />

depreciation <strong>and</strong><br />

administration, etc.<br />

Therefore, a third<br />

allocation step is<br />

necessary. As<br />

shown in figure 33,<br />

this third allocation<br />

step can motivate<br />

management to<br />

realize huge<br />

efficiency gains by<br />

The choice of an accurate allocation key is crucial for obtaining correct information for cost<br />

accounting. It is important that the chosen allocation key is closely linked with actual,<br />

environment-related costs. In practice, the following four allocation keys are considered for<br />

environmental issues:<br />

• Volume of emissions or waste treated;<br />

-76-