Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

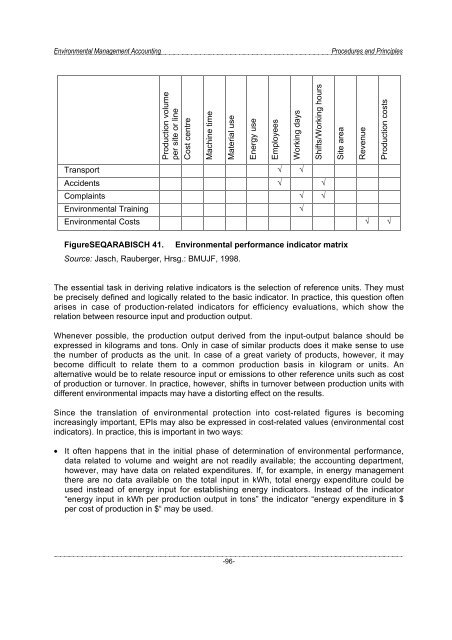

Production volume<br />

per site or line<br />

Cost centre<br />

Machine time<br />

Material use<br />

Energy use<br />

Employees<br />

Working days<br />

Shifts/Working hours<br />

Site area<br />

Revenue<br />

Production costs<br />

Transport √ √<br />

Accidents √ √<br />

Complaints √ √<br />

<strong>Environmental</strong> Training<br />

√<br />

<strong>Environmental</strong> Costs √ √<br />

FigureSEQARABISCH 41. <strong>Environmental</strong> performance indicator matrix<br />

Source: Jasch, Rauberger, Hrsg.: BMUJF, 1998.<br />

The essential task in deriving relative indicators is the selection of reference units. They must<br />

be precisely defined <strong>and</strong> logically related to the basic indicator. In practice, this question often<br />

arises in case of production-related indicators for efficiency evaluations, which show the<br />

relation between resource input <strong>and</strong> production output.<br />

Whenever possible, the production output derived from the input-output balance should be<br />

expressed in kilograms <strong>and</strong> tons. Only in case of similar products does it make sense to use<br />

the number of products as the unit. In case of a great variety of products, however, it may<br />

become difficult to relate them to a common production basis in kilogram or units. An<br />

alternative would be to relate resource input or emissions to other reference units such as cost<br />

of production or turnover. In practice, however, shifts in turnover between production units with<br />

different environmental impacts may have a distorting effect on the results.<br />

Since the translation of environmental protection into cost-related figures is becoming<br />

increasingly important, EPIs may also be expressed in cost-related values (environmental cost<br />

indicators). In practice, this is important in two ways:<br />

• It often happens that in the initial phase of determination of environmental performance,<br />

data related to volume <strong>and</strong> weight are not readily available; the accounting department,<br />

however, may have data on related expenditures. If, for example, in energy management<br />

there are no data available on the total input in kWh, total energy expenditure could be<br />

used instead of energy input for establishing energy indicators. Instead of the indicator<br />

“energy input in kWh per production output in tons” the indicator “energy expenditure in $<br />

per cost of production in $“ may be used.<br />

-96-