Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

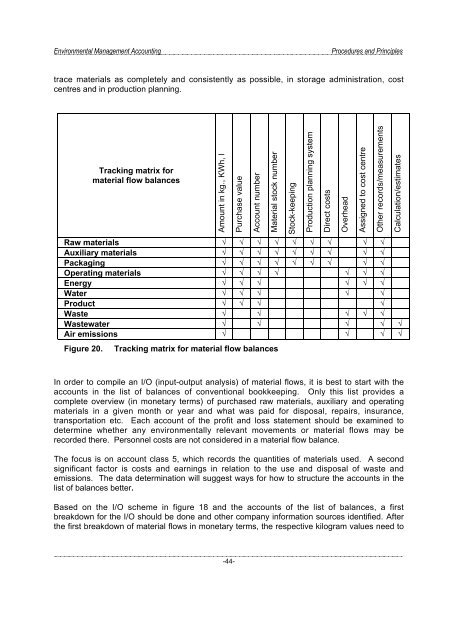

trace materials as completely <strong>and</strong> consistently as possible, in storage administration, cost<br />

centres <strong>and</strong> in production planning.<br />

Tracking matrix for<br />

material flow balances<br />

Amount in kg., KWh, l<br />

Purchase value<br />

Raw materials √ √ √ √ √ √ √ √ √<br />

Auxiliary materials √ √ √ √ √ √ √ √ √<br />

Packaging √ √ √ √ √ √ √ √ √<br />

Operating materials √ √ √ √ √ √ √<br />

Energy √ √ √ √ √ √<br />

Water √ √ √ √ √<br />

Product √ √ √ √<br />

Waste √ √ √ √ √<br />

Wastewater √ √ √ √ √<br />

Air emissions √ √ √ √<br />

Figure 20. Tracking matrix for material flow balances<br />

Account number<br />

Material stock number<br />

Stock-keeping<br />

Production planning system<br />

Direct costs<br />

Overhead<br />

Assigned to cost centre<br />

Other records/measurements<br />

Calculation/estimates<br />

In order to compile an I/O (input-output analysis) of material flows, it is best to start with the<br />

accounts in the list of balances of conventional bookkeeping. Only this list provides a<br />

complete overview (in monetary terms) of purchased raw materials, auxiliary <strong>and</strong> operating<br />

materials in a given month or year <strong>and</strong> what was paid for disposal, repairs, insurance,<br />

transportation etc. Each account of the profit <strong>and</strong> loss statement should be examined to<br />

determine whether any environmentally relevant movements or material flows may be<br />

recorded there. Personnel costs are not considered in a material flow balance.<br />

The focus is on account class 5, which records the quantities of materials used. A second<br />

significant factor is costs <strong>and</strong> earnings in relation to the use <strong>and</strong> disposal of waste <strong>and</strong><br />

emissions. The data determination will suggest ways for how to structure the accounts in the<br />

list of balances better.<br />

Based on the I/O scheme in figure 18 <strong>and</strong> the accounts of the list of balances, a first<br />

breakdown for the I/O should be done <strong>and</strong> other company information sources identified. After<br />

the first breakdown of material flows in monetary terms, the respective kilogram values need to<br />

-44-