Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

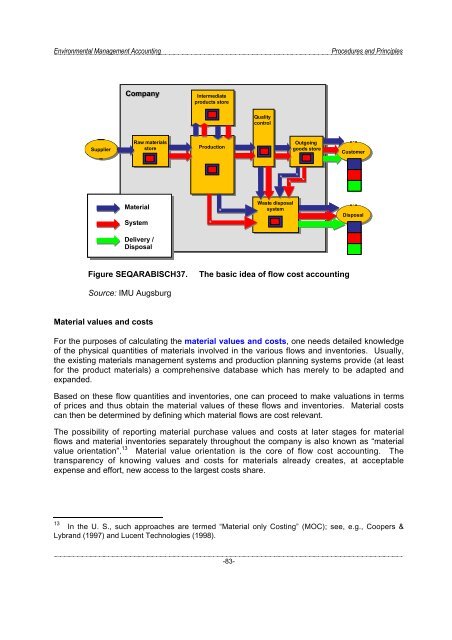

Company<br />

Intermediate<br />

products store<br />

Quality<br />

control<br />

Supplier<br />

Raw materials<br />

store<br />

Production<br />

Outgoing<br />

goods store<br />

Customer<br />

Material<br />

System<br />

Waste disposal<br />

system<br />

Disposal<br />

Delivery /<br />

Disposal<br />

Figure SEQARABISCH37.<br />

The basic idea of flow cost accounting<br />

Source: IMU Augsburg<br />

Material values <strong>and</strong> costs<br />

For the purposes of calculating the material values <strong>and</strong> costs, one needs detailed knowledge<br />

of the physical quantities of materials involved in the various flows <strong>and</strong> inventories. Usually,<br />

the existing materials management systems <strong>and</strong> production planning systems provide (at least<br />

for the product materials) a comprehensive database which has merely to be adapted <strong>and</strong><br />

exp<strong>and</strong>ed.<br />

Based on these flow quantities <strong>and</strong> inventories, one can proceed to make valuations in terms<br />

of prices <strong>and</strong> thus obtain the material values of these flows <strong>and</strong> inventories. Material costs<br />

can then be determined by defining which material flows are cost relevant.<br />

The possibility of reporting material purchase values <strong>and</strong> costs at later stages for material<br />

flows <strong>and</strong> material inventories separately throughout the company is also known as “material<br />

value orientation”. 13 Material value orientation is the core of flow cost accounting. The<br />

transparency of knowing values <strong>and</strong> costs for materials already creates, at acceptable<br />

expense <strong>and</strong> effort, new access to the largest costs share.<br />

13<br />

In the U. S., such approaches are termed “Material only Costing” (MOC); see, e.g., Coopers &<br />

Lybr<strong>and</strong> (1997) <strong>and</strong> Lucent Technologies (1998).<br />

-83-