Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

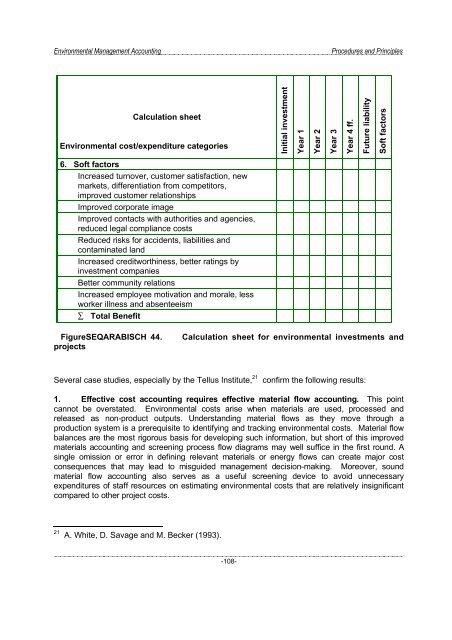

Calculation sheet<br />

<strong>Environmental</strong> cost/expenditure categories<br />

Initial investment<br />

Year 1<br />

Year 2<br />

Year 3<br />

Year 4 ff.<br />

Future liability<br />

Soft factors<br />

6. Soft factors<br />

Increased turnover, customer satisfaction, new<br />

markets, differentiation from competitors,<br />

improved customer relationships<br />

Improved corporate image<br />

Improved contacts with authorities <strong>and</strong> agencies,<br />

reduced legal compliance costs<br />

Reduced risks for accidents, liabilities <strong>and</strong><br />

contaminated l<strong>and</strong><br />

Increased creditworthiness, better ratings by<br />

investment companies<br />

Better community relations<br />

Increased employee motivation <strong>and</strong> morale, less<br />

worker illness <strong>and</strong> absenteeism<br />

∑ Total Benefit<br />

FigureSEQARABISCH 44.<br />

projects<br />

Calculation sheet for environmental investments <strong>and</strong><br />

Several case studies, especially by the Tellus Institute, 21<br />

confirm the following results:<br />

1. Eff ecti ve cost account ing requi r es ef fect ive mat eri al fl ow accounti ng. Thi s poi nt<br />

c annot be ov ers tated. Envi ronment al cost s ari se when materi als are us ed, proces sed <strong>and</strong><br />

r el eased as non-produc t out puts . Unders t<strong>and</strong>i ng materi al fl ows as they mov e through a<br />

product i on sy st em is a pr er equi s it e to ident if yi ng <strong>and</strong> track i ng env i ronment al cost s. Mat er ial flow<br />

bal ances are the mos t ri gor ous bas is for dev el oping suc h inf or mat ion, but short of thi s impr ov ed<br />

mat er ial s ac c ount ing <strong>and</strong> sc reeni ng pr oc es s flow diagr ams may well suff ic e in the fir s t round. A<br />

s ingl e omi ss i on or err or in def i ni ng relevant mat er ials or ener gy fl ows can create major cos t<br />

c onsequenc es that may lead to mi sgui ded management deci s ion- mak ing. Mor eov er , sound<br />

mat er ial flow acc ounti ng al so serv es as a us ef ul sc reeni ng devi ce to avoi d unnec es sar y<br />

expendi t ur es of staf f res ourc es on es ti mati ng env ir onmental cos ts that ar e relat iv el y ins ignif ic ant<br />

c ompared t o other pr oj ec t c os ts .<br />

21 A. White, D. Savage <strong>and</strong> M. Becker (1993).<br />

-108-