Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

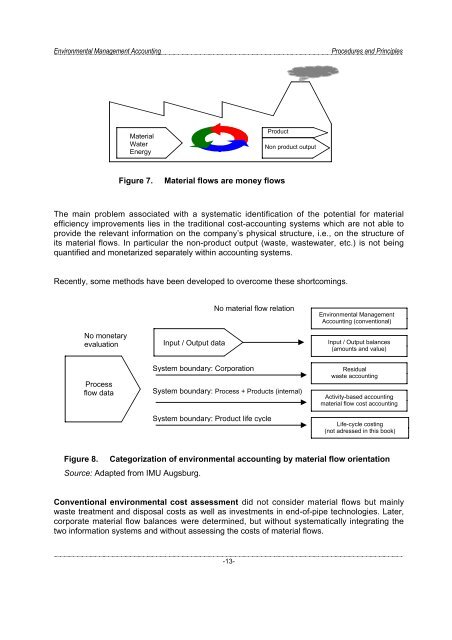

Material<br />

Water<br />

Energy<br />

Product<br />

Non product output<br />

Figure 7.<br />

Material flows are money flows<br />

The main problem associated with a systematic identification of the potential for material<br />

efficiency improvements lies in the traditional cost-accounting systems which are not able to<br />

provide the relevant information on the company’s physical structure, i.e., on the structure of<br />

its material flows. In particular the non-product output (waste, wastewater, etc.) is not being<br />

quantified <strong>and</strong> monetarized separately within accounting systems.<br />

Recently, some methods have been developed to overcome these shortcomings.<br />

No monetary<br />

evaluation<br />

Input / Output data<br />

No material flow relation<br />

<strong>Environmental</strong> <strong>Management</strong><br />

<strong>Accounting</strong> (conventional)<br />

Input / Output balances<br />

(amounts <strong>and</strong> value)<br />

Process<br />

flow data<br />

System boundary: Corporation<br />

System boundary: Process + Products (internal)<br />

System boundary: Product life cycle<br />

Residual<br />

waste accounting<br />

Activity-based accounting<br />

material flow cost accounting<br />

Life-cycle costing<br />

(not adressed in this book)<br />

Figure 8. Categorization of environmental accounting by material flow orientation<br />

Source: Adapted from IMU Augsburg.<br />

Conventional environmental cost assessment did not consider material flows but mainly<br />

waste treatment <strong>and</strong> disposal costs as well as investments in end-of-pipe technologies. Later,<br />

corporate material flow balances were determined, but without systematically integrating the<br />

two information systems <strong>and</strong> without assessing the costs of material flows.<br />

-13-