Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

Supplier<br />

Material<br />

Incoming<br />

Production<br />

Outgoing<br />

storage<br />

storage<br />

Products &<br />

Packaging<br />

Customer<br />

Material losses<br />

Disposal<br />

system<br />

Residual<br />

Substances<br />

- solid waste<br />

- effluent<br />

- exhaust<br />

- heat / noise<br />

emission<br />

Disposal<br />

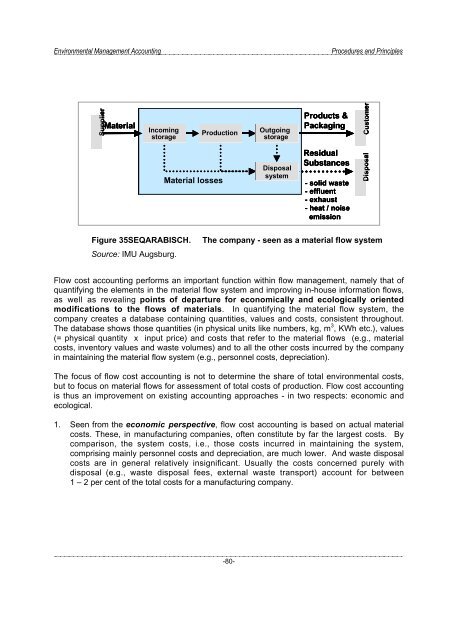

Figure 35SEQARABISCH.<br />

Source: IMU Augsburg.<br />

The company - seen as a material flow system<br />

Flow cost accounting performs an important function within flow management, namely that of<br />

quantifying the elements in the material flow system <strong>and</strong> improving in-house information flows,<br />

as well as revealing points of departure for economically <strong>and</strong> ecologically oriented<br />

modifications to the flows of materials. In quantifying the material flow system, the<br />

company creates a database containing quantities, values <strong>and</strong> costs, consistent throughout.<br />

The database shows those quantities (in physical units like numbers, kg, m 3 , KWh etc.), values<br />

(= physical quantity x input price) <strong>and</strong> costs that refer to the material flows (e.g., material<br />

costs, inventory values <strong>and</strong> waste volumes) <strong>and</strong> to all the other costs incurred by the company<br />

in maintaining the material flow system (e.g., personnel costs, depreciation).<br />

The focus of flow cost accounting is not to determine the share of total environmental costs,<br />

but to focus on material flows for assessment of total costs of production. Flow cost accounting<br />

is thus an improvement on existing accounting approaches - in two respects: economic <strong>and</strong><br />

ecological.<br />

1. Seen from the economic perspective, flow cost accounting is based on actual material<br />

costs. These, in manufacturing companies, often constitute by far the largest costs. By<br />

comparison, the system costs, i.e., those costs incurred in maintaining the system,<br />

comprising mainly personnel costs <strong>and</strong> depreciation, are much lower. And waste disposal<br />

costs are in general relatively insignificant. Usually the costs concerned purely with<br />

disposal (e.g., waste disposal fees, external waste transport) account for between<br />

1 – 2 per cent of the total costs for a manufacturing company.<br />

-80-