Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

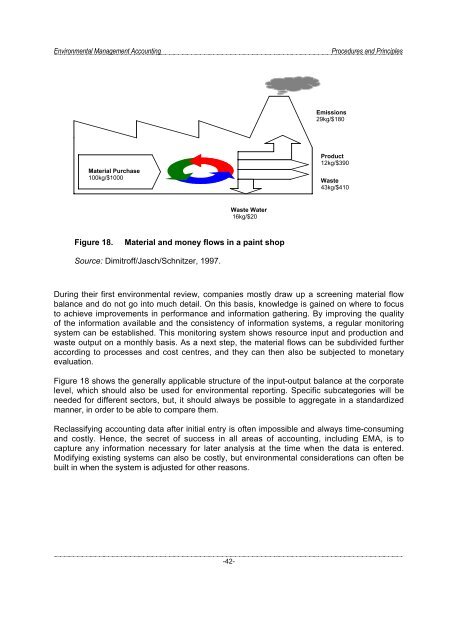

Emissions<br />

29kg/$180<br />

Material Purchase<br />

100kg/$1000<br />

Product<br />

12kg/$390<br />

Waste<br />

43kg/$410<br />

Waste Water<br />

16kg/$20<br />

Figure 18.<br />

Material <strong>and</strong> money flows in a paint shop<br />

Source: Dimitroff/Jasch/Schnitzer, 1997.<br />

During their first environmental review, companies mostly draw up a screening material flow<br />

balance <strong>and</strong> do not go into much detail. On this basis, knowledge is gained on where to focus<br />

to achieve improvements in performance <strong>and</strong> information gathering. By improving the quality<br />

of the information available <strong>and</strong> the consistency of information systems, a regular monitoring<br />

system can be established. This monitoring system shows resource input <strong>and</strong> production <strong>and</strong><br />

waste output on a monthly basis. As a next step, the material flows can be subdivided further<br />

according to processes <strong>and</strong> cost centres, <strong>and</strong> they can then also be subjected to monetary<br />

evaluation.<br />

Figure 18 shows the generally applicable structure of the input-output balance at the corporate<br />

level, which should also be used for environmental reporting. Specific subcategories will be<br />

needed for different sectors, but, it should always be possible to aggregate in a st<strong>and</strong>ardized<br />

manner, in order to be able to compare them.<br />

Reclassifying accounting data after initial entry is often impossible <strong>and</strong> always time-consuming<br />

<strong>and</strong> costly. Hence, the secret of success in all areas of accounting, including EMA, is to<br />

capture any information necessary for later analysis at the time when the data is entered.<br />

Modifying existing systems can also be costly, but environmental considerations can often be<br />

built in when the system is adjusted for other reasons.<br />

-42-