Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

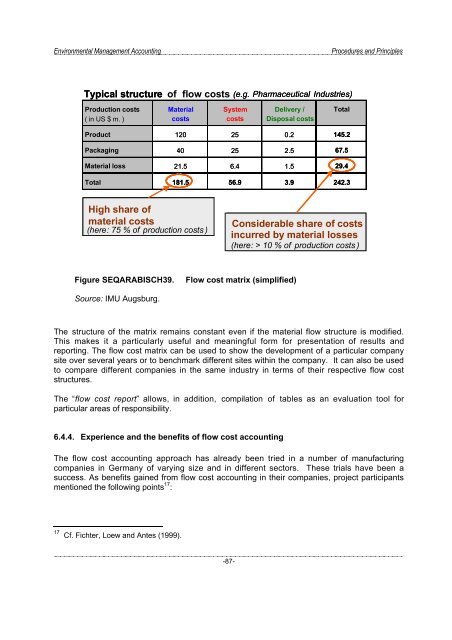

Typical structure of flow costs (e.g. Pharmaceutical Industries)<br />

Production costs<br />

Material<br />

System<br />

Delivery /<br />

Total<br />

( in US $ m. )<br />

costs<br />

costs<br />

Disposal costs<br />

Product 120 25 0.2 145.2<br />

Packaging 40 25 2.5 67.5<br />

Material loss 21.5 6.4 1.5 29.4<br />

Total 181.5 56.9 3.9 242.3<br />

Eminent High share share of of<br />

Material material costs !<br />

(<br />

here : 75 % of production costs )<br />

Considerable share of costs<br />

incurred by Material material losses !<br />

( here : > 10 % of production costs )<br />

Figure SEQARABISCH39.<br />

Flow cost matrix (simplified)<br />

Source: IMU Augsburg.<br />

The structure of the matrix remains constant even if the material flow structure is modified.<br />

This makes it a particularly useful <strong>and</strong> meaningful form for presentation of results <strong>and</strong><br />

reporting. The flow cost matrix can be used to show the development of a particular company<br />

site over several years or to benchmark different sites within the company. It can also be used<br />

to compare different companies in the same industry in terms of their respective flow cost<br />

structures.<br />

The “flow cost report” allows, in addition, compilation of tables as an evaluation tool for<br />

particular areas of responsibility.<br />

6.4.4. Experience <strong>and</strong> the benefits of flow cost accounting<br />

The flow cost accounting approach has already been tried in a number of manufacturing<br />

companies in Germany of varying size <strong>and</strong> in different sectors. These trials have been a<br />

success. As benefits gained from flow cost accounting in their companies, project participants<br />

mentioned the following points 17 :<br />

17 Cf. Fichter, Loew <strong>and</strong> Antes (1999).<br />

-87-