Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Environmental Management Accounting Procedures and Principles

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Environmental</strong> <strong>Management</strong> <strong>Accounting</strong><br />

<strong>Procedures</strong> <strong>and</strong> <strong>Principles</strong><br />

a consistency check provides great optimization potentials, <strong>and</strong> has thus become a major tool<br />

in environmental accounting. Therefore it is desirable for the technical <strong>and</strong> financial<br />

bookkeeping to be conducted in a compatible way.<br />

Emissions<br />

Input<br />

Product<br />

Waste<br />

Wastewater<br />

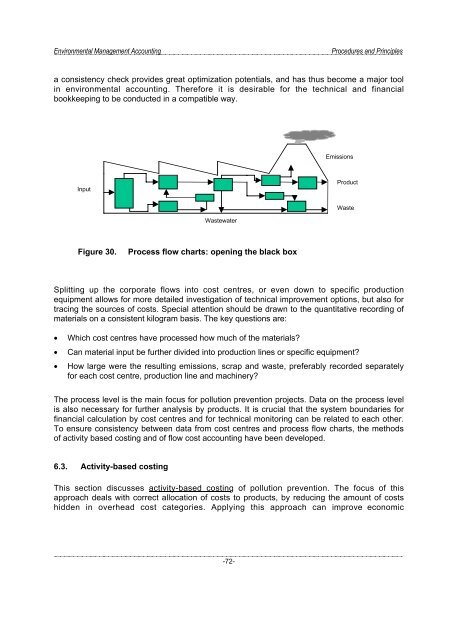

Figure 30.<br />

Process flow charts: opening the black box<br />

Splitting up the corporate flows into cost centres, or even down to specific production<br />

equipment allows for more detailed investigation of technical improvement options, but also for<br />

tracing the sources of costs. Special attention should be drawn to the quantitative recording of<br />

materials on a consistent kilogram basis. The key questions are:<br />

• Which cost centres have processed how much of the materials?<br />

• Can material input be further divided into production lines or specific equipment?<br />

• How large were the resulting emissions, scrap <strong>and</strong> waste, preferably recorded separately<br />

for each cost centre, production line <strong>and</strong> machinery?<br />

The process level is the main focus for pollution prevention projects. Data on the process level<br />

is also necessary for further analysis by products. It is crucial that the system boundaries for<br />

financial calculation by cost centres <strong>and</strong> for technical monitoring can be related to each other.<br />

To ensure consistency between data from cost centres <strong>and</strong> process flow charts, the methods<br />

of activity based costing <strong>and</strong> of flow cost accounting have been developed.<br />

6.3. Activity-based costing<br />

This section discusses activity-based costing of pollution prevention. The focus of this<br />

approach deals with correct allocation of costs to products, by reducing the amount of costs<br />

hidden in overhead cost categories. Applying this approach can improve economic<br />

-72-