Child Support Enforcement - Sarpy County Nebraska

Child Support Enforcement - Sarpy County Nebraska

Child Support Enforcement - Sarpy County Nebraska

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

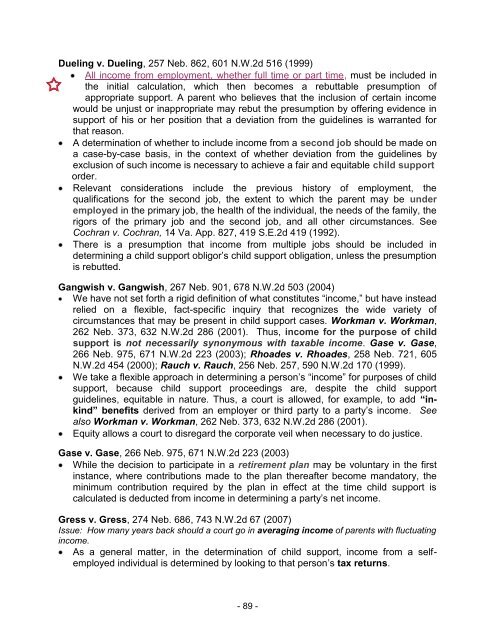

Dueling v. Dueling, 257 Neb. 862, 601 N.W.2d 516 (1999)<br />

All income from employment, whether full time or part time, must be included in<br />

the initial calculation, which then becomes a rebuttable presumption of<br />

appropriate support. A parent who believes that the inclusion of certain income<br />

would be unjust or inappropriate may rebut the presumption by offering evidence in<br />

support of his or her position that a deviation from the guidelines is warranted for<br />

that reason.<br />

A determination of whether to include income from a second job should be made on<br />

a case-by-case basis, in the context of whether deviation from the guidelines by<br />

exclusion of such income is necessary to achieve a fair and equitable child support<br />

order.<br />

Relevant considerations include the previous history of employment, the<br />

qualifications for the second job, the extent to which the parent may be under<br />

employed in the primary job, the health of the individual, the needs of the family, the<br />

rigors of the primary job and the second job, and all other circumstances. See<br />

Cochran v. Cochran, 14 Va. App. 827, 419 S.E.2d 419 (1992).<br />

There is a presumption that income from multiple jobs should be included in<br />

determining a child support obligor‘s child support obligation, unless the presumption<br />

is rebutted.<br />

Gangwish v. Gangwish, 267 Neb. 901, 678 N.W.2d 503 (2004)<br />

We have not set forth a rigid definition of what constitutes ―income,‖ but have instead<br />

relied on a flexible, fact-specific inquiry that recognizes the wide variety of<br />

circumstances that may be present in child support cases. Workman v. Workman,<br />

262 Neb. 373, 632 N.W.2d 286 (2001). Thus, income for the purpose of child<br />

support is not necessarily synonymous with taxable income. Gase v. Gase,<br />

266 Neb. 975, 671 N.W.2d 223 (2003); Rhoades v. Rhoades, 258 Neb. 721, 605<br />

N.W.2d 454 (2000); Rauch v. Rauch, 256 Neb. 257, 590 N.W.2d 170 (1999).<br />

We take a flexible approach in determining a person‘s ―income‖ for purposes of child<br />

support, because child support proceedings are, despite the child support<br />

guidelines, equitable in nature. Thus, a court is allowed, for example, to add “inkind”<br />

benefits derived from an employer or third party to a party‘s income. See<br />

also Workman v. Workman, 262 Neb. 373, 632 N.W.2d 286 (2001).<br />

Equity allows a court to disregard the corporate veil when necessary to do justice.<br />

Gase v. Gase, 266 Neb. 975, 671 N.W.2d 223 (2003)<br />

While the decision to participate in a retirement plan may be voluntary in the first<br />

instance, where contributions made to the plan thereafter become mandatory, the<br />

minimum contribution required by the plan in effect at the time child support is<br />

calculated is deducted from income in determining a party‘s net income.<br />

Gress v. Gress, 274 Neb. 686, 743 N.W.2d 67 (2007)<br />

Issue: How many years back should a court go in averaging income of parents with fluctuating<br />

income.<br />

As a general matter, in the determination of child support, income from a selfemployed<br />

individual is determined by looking to that person‘s tax returns.<br />

- 89 -