Comprehensive Annual Financial Report - St. Tammany Parish ...

Comprehensive Annual Financial Report - St. Tammany Parish ...

Comprehensive Annual Financial Report - St. Tammany Parish ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

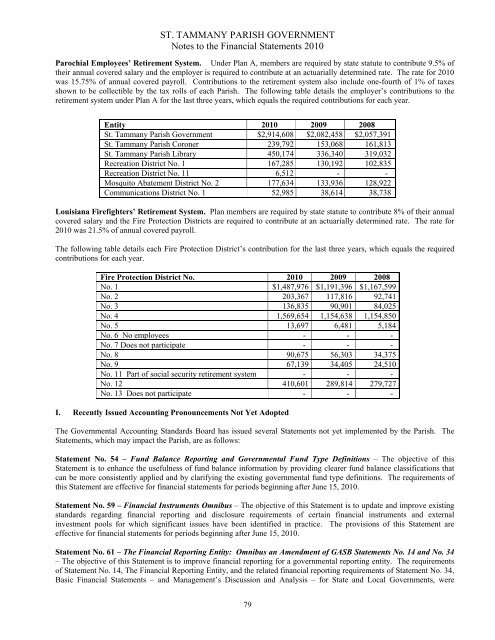

ST. TAMMANY PARISH GOVERNMENT<br />

Notes to the <strong>Financial</strong> <strong>St</strong>atements 2010<br />

Parochial Employees’ Retirement System. Under Plan A, members are required by state statute to contribute 9.5% of<br />

their annual covered salary and the employer is required to contribute at an actuarially determined rate. The rate for 2010<br />

was 15.75% of annual covered payroll. Contributions to the retirement system also include one-fourth of 1% of taxes<br />

shown to be collectible by the tax rolls of each <strong>Parish</strong>. The following table details the employer’s contributions to the<br />

retirement system under Plan A for the last three years, which equals the required contributions for each year.<br />

Entity 2010 2009 2008<br />

<strong>St</strong>. <strong>Tammany</strong> <strong>Parish</strong> Government $2,914,608 $2,082,458 $2,057,391<br />

<strong>St</strong>. <strong>Tammany</strong> <strong>Parish</strong> Coroner 239,792 153,068 161,813<br />

<strong>St</strong>. <strong>Tammany</strong> <strong>Parish</strong> Library 450,174 336,340 319,032<br />

Recreation District No. 1 167,285 130,192 102,835<br />

Recreation District No. 11 6,512 - -<br />

Mosquito Abatement District No. 2 177,634 133,936 128,922<br />

Communications District No. 1 52,985 38,614 38,738<br />

Louisiana Firefighters’ Retirement System. Plan members are required by state statute to contribute 8% of their annual<br />

covered salary and the Fire Protection Districts are required to contribute at an actuarially determined rate. The rate for<br />

2010 was 21.5% of annual covered payroll.<br />

The following table details each Fire Protection District’s contribution for the last three years, which equals the required<br />

contributions for each year.<br />

Fire Protection District No. 2010 2009 2008<br />

No. 1 $1,487,976 $1,191,396 $1,167,599<br />

No. 2 203,367 117,816 92,741<br />

No. 3 136,835 90,901 84,025<br />

No. 4 1,569,654 1,154,638 1,154,850<br />

No. 5 13,697 6,481 5,184<br />

No. 6 No employees - - -<br />

No. 7 Does not participate - - -<br />

No. 8 90,675 56,303 34,375<br />

No. 9 67,139 34,405 24,510<br />

No. 11 Part of social security retirement system - - -<br />

No. 12 410,601 289,814 279,727<br />

No. 13 Does not participate - - -<br />

I. Recently Issued Accounting Pronouncements Not Yet Adopted<br />

The Governmental Accounting <strong>St</strong>andards Board has issued several <strong>St</strong>atements not yet implemented by the <strong>Parish</strong>. The<br />

<strong>St</strong>atements, which may impact the <strong>Parish</strong>, are as follows:<br />

<strong>St</strong>atement No. 54 – Fund Balance <strong>Report</strong>ing and Governmental Fund Type Definitions – The objective of this<br />

<strong>St</strong>atement is to enhance the usefulness of fund balance information by providing clearer fund balance classifications that<br />

can be more consistently applied and by clarifying the existing governmental fund type definitions. The requirements of<br />

this <strong>St</strong>atement are effective for financial statements for periods beginning after June 15, 2010.<br />

<strong>St</strong>atement No. 59 – <strong>Financial</strong> Instruments Omnibus – The objective of this <strong>St</strong>atement is to update and improve existing<br />

standards regarding financial reporting and disclosure requirements of certain financial instruments and external<br />

investment pools for which significant issues have been identified in practice. The provisions of this <strong>St</strong>atement are<br />

effective for financial statements for periods beginning after June 15, 2010.<br />

<strong>St</strong>atement No. 61 – The <strong>Financial</strong> <strong>Report</strong>ing Entity: Omnibus an Amendment of GASB <strong>St</strong>atements No. 14 and No. 34<br />

– The objective of this <strong>St</strong>atement is to improve financial reporting for a governmental reporting entity. The requirements<br />

of <strong>St</strong>atement No. 14, The <strong>Financial</strong> <strong>Report</strong>ing Entity, and the related financial reporting requirements of <strong>St</strong>atement No. 34,<br />

Basic <strong>Financial</strong> <strong>St</strong>atements – and Management’s Discussion and Analysis – for <strong>St</strong>ate and Local Governments, were<br />

79