Monthly Bulletin July 2009 - Banque de France

Monthly Bulletin July 2009 - Banque de France

Monthly Bulletin July 2009 - Banque de France

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ECONOMIC<br />

AND MONETARY<br />

DEVELOPMENTS<br />

Prices and<br />

costs<br />

Chart 21 Breakdown of industrial producer<br />

prices<br />

(annual percentage changes; monthly data)<br />

Chart 22 Producer input and output price<br />

surveys<br />

(diffusion indices; monthly data)<br />

total industry excluding construction (left-hand scale)<br />

intermediate goods (left-hand scale)<br />

capital goods (left-hand scale)<br />

consumer goods (left-hand scale)<br />

energy (right-hand scale)<br />

manufacturing; input prices<br />

manufacturing; prices charged<br />

services; input prices<br />

services; prices charged<br />

10<br />

30<br />

80<br />

80<br />

8<br />

6<br />

24<br />

18<br />

70<br />

70<br />

4<br />

12<br />

60<br />

60<br />

2<br />

6<br />

50<br />

50<br />

0<br />

-2<br />

0<br />

-6<br />

40<br />

40<br />

-4<br />

-12<br />

30<br />

30<br />

-6<br />

2004 2005 2006 2007<br />

2008<br />

Sources: Eurostat and ECB calculations.<br />

Note: Data refer to the euro area including Slovakia.<br />

-18<br />

20<br />

2004 2005 2006 2007 2008<br />

Source: Markit.<br />

Note: An in<strong>de</strong>x value above 50 indicates an increase in prices,<br />

whereas a value below 50 indicates a <strong>de</strong>crease.<br />

20<br />

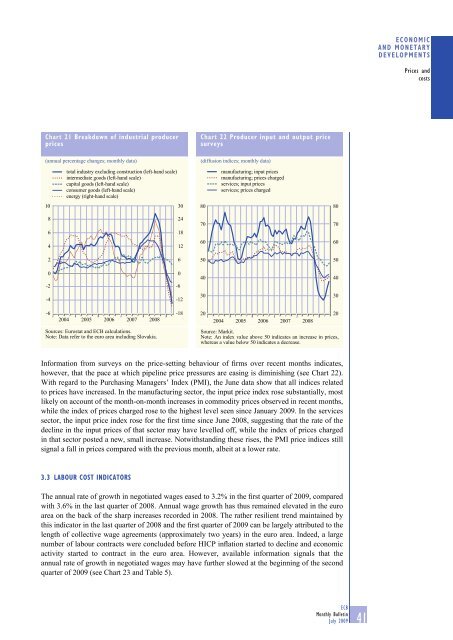

Information from surveys on the price-setting behaviour of firms over recent months indicates,<br />

however, that the pace at which pipeline price pressures are easing is diminishing (see Chart 22).<br />

With regard to the Purchasing Managers’ In<strong>de</strong>x (PMI), the June data show that all indices related<br />

to prices have increased. In the manufacturing sector, the input price in<strong>de</strong>x rose substantially, most<br />

likely on account of the month-on-month increases in commodity prices observed in recent months,<br />

while the in<strong>de</strong>x of prices charged rose to the highest level seen since January <strong>2009</strong>. In the services<br />

sector, the input price in<strong>de</strong>x rose for the first time since June 2008, suggesting that the rate of the<br />

<strong>de</strong>cline in the input prices of that sector may have levelled off, while the in<strong>de</strong>x of prices charged<br />

in that sector posted a new, small increase. Notwithstanding these rises, the PMI price indices still<br />

signal a fall in prices compared with the previous month, albeit at a lower rate.<br />

3.3 LABOUR COST INDICATORS<br />

The annual rate of growth in negotiated wages eased to 3.2% in the first quarter of <strong>2009</strong>, compared<br />

with 3.6% in the last quarter of 2008. Annual wage growth has thus remained elevated in the euro<br />

area on the back of the sharp increases recor<strong>de</strong>d in 2008. The rather resilient trend maintained by<br />

this indicator in the last quarter of 2008 and the first quarter of <strong>2009</strong> can be largely attributed to the<br />

length of collective wage agreements (approximately two years) in the euro area. In<strong>de</strong>ed, a large<br />

number of labour contracts were conclu<strong>de</strong>d before HICP inflation started to <strong>de</strong>cline and economic<br />

activity started to contract in the euro area. However, available information signals that the<br />

annual rate of growth in negotiated wages may have further slowed at the beginning of the second<br />

quarter of <strong>2009</strong> (see Chart 23 and Table 5).<br />

ECB<br />

<strong>Monthly</strong> <strong>Bulletin</strong><br />

<strong>July</strong> <strong>2009</strong><br />

41