- Page 1 and 2:

Proceedings from the Third Internat

- Page 3 and 4:

© All rights reserved. No part of

- Page 5 and 6:

Skopje, 15.10.2009 Dear Colleagues,

- Page 8 and 9:

CONTENTS: PART I: REGIONAL TRADE AG

- Page 10:

Ph.D. Sanja Đurđić THE RULE OF L

- Page 13 and 14:

PART I: Greater openness means fier

- Page 15 and 16:

PART I: the past never experienced

- Page 17 and 18:

PART I: Nowadays such actions will

- Page 19 and 20:

PART I: ratio could ultimately rais

- Page 21 and 22:

PART I: 3. CEFTA regional cooperati

- Page 23 and 24:

PART I: any other type of economic

- Page 25 and 26:

PART I: including Kosovo, who is de

- Page 27 and 28:

PART I: Rodrik, Dani. (1999), The N

- Page 29 and 30:

PART I: The paper examines how West

- Page 31 and 32:

PART I: What are the main reasons f

- Page 33 and 34:

PART I: EU growth rates and a sign

- Page 35 and 36:

PART I: only a limited portion of t

- Page 37 and 38:

PART I: on a larger trade deficit;

- Page 39 and 40:

PART I: and world trade in goods an

- Page 42 and 43:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 44 and 45:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 46 and 47:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 48 and 49:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 50 and 51:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 52:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 55 and 56:

PART I: was developed especially fo

- Page 57 and 58:

PART I: 2. Theoretical background,

- Page 59 and 60:

PART I: focus on the way in which t

- Page 61 and 62:

PART I: of private incomes by addin

- Page 63 and 64:

PART I: the GDP per capita: the 53.

- Page 65 and 66:

PART I: received EU-transfers, but

- Page 68 and 69:

Dr Márta Zádor, PhD Deputy Genera

- Page 70 and 71:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 72 and 73:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 74 and 75:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 76 and 77:

Macedonia REGIONAL TRADE AGREEMENTS

- Page 78 and 79:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 80 and 81:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 82 and 83:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 84 and 85:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 86 and 87:

Goran Buturac, Ph.D., Research Fell

- Page 88 and 89:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 90 and 91:

c in total exports of country a in

- Page 92 and 93:

2.3. Comparative advantages REGIONA

- Page 94 and 95:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 96 and 97:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 98 and 99:

2.6. Export similarities The paper

- Page 100:

REGIONAL TRADE AGREEMENTS AND REGIO

- Page 103 and 104:

PART II: INTRODUCTION CEFTA-2006 is

- Page 105 and 106:

PART II: Agreement for Modification

- Page 107 and 108:

PART II: only provide temporary rep

- Page 109 and 110:

PART II: The Leaders of the Group o

- Page 111 and 112:

PART II: messages over the past yea

- Page 113 and 114:

PART II: INTRODUCTION Central Europ

- Page 115 and 116:

PART II: Table 1: Gross domestic pr

- Page 117 and 118:

PART II: Figure 3: Distribution of

- Page 119 and 120:

PART II: Table 6: Countries of West

- Page 121 and 122:

PART II: Adriatic gas pipeline is c

- Page 123 and 124:

PART II: Total Croatian export to t

- Page 125 and 126:

PART II: CIA - The World Bank Factb

- Page 128 and 129:

CEFTA-2006 TRADE COOPERATION Sanja

- Page 130 and 131:

the implementation of the protocol

- Page 132 and 133:

CEFTA-2006 TRADE COOPERATION in the

- Page 134 and 135:

The major foreign trade partners in

- Page 136:

Integration, Vol. 26, No. 3, 309-33

- Page 139 and 140:

PART II: divisive, as well as mainl

- Page 141 and 142:

PART II: of time. During the transi

- Page 143 and 144:

PART II: been recovered from 2004 o

- Page 145 and 146:

PART II: diversified structure as c

- Page 147 and 148:

PART II: VAR and to test if one may

- Page 149 and 150: PART II: VAR since the test for coi

- Page 151 and 152: PART II: coefficient sign) but mode

- Page 153 and 154: PART II: elasticity. The seasonal f

- Page 155 and 156: PART II: GDP” that has been runni

- Page 157 and 158: PART II: Faini, R., Pritchett, L. a

- Page 159 and 160: PART II: pleasant. The expectations

- Page 161 and 162: PART II: Table 3: Regional trade ex

- Page 163 and 164: PART II: In order to bring to an en

- Page 165 and 166: PART II: stimulated the growth rate

- Page 168 and 169: CEFTA-2006 TRADE COOPERATION Irena

- Page 170 and 171: CEFTA-2006 TRADE COOPERATION within

- Page 172 and 173: Table 2: Data on exports of agricul

- Page 174 and 175: CEFTA-2006 TRADE COOPERATION 3.1. T

- Page 176 and 177: Macedonian export of non-agricultur

- Page 178 and 179: is 37.1% of the total Serbian trade

- Page 180: CEFTA-2006 TRADE COOPERATION na CEF

- Page 183 and 184: PART II: countries in the Region, a

- Page 185 and 186: PART II: becoming wealthier consume

- Page 187 and 188: PART II: versa for Croatia; for Mac

- Page 189 and 190: PART II: Table 5: Exports of the Re

- Page 191 and 192: PART II: Commission of the European

- Page 193 and 194: PART III: Serbia, Macedonia and man

- Page 195 and 196: PART III: of TNCs have changed the

- Page 197 and 198: PART III: 3. Foundations of the new

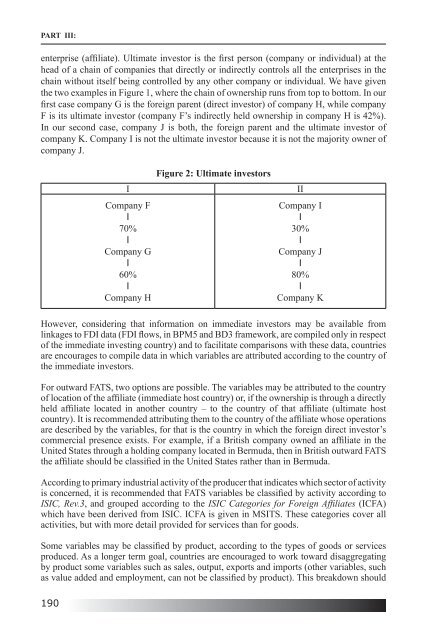

- Page 199: PART III: modes of supply, FATS cor

- Page 203 and 204: PART III: REFERENCES Bjelić, Predr

- Page 205 and 206: PART III: requirement for compulsor

- Page 207 and 208: PART III: Companies prepare and pre

- Page 209 and 210: PART III: it refers to adjusting of

- Page 211 and 212: PART III: presentation of assets, l

- Page 214 and 215: SOME ASPECTS OF TRADE STATISTICS AN

- Page 216 and 217: their mass and inversely proportion

- Page 218 and 219: Peri specifications in log-log spac

- Page 220 and 221: orn population, is less reliable an

- Page 222 and 223: SOME ASPECTS OF TRADE STATISTICS AN

- Page 224: Weltwirtschaftliches Archiv, 90(01)

- Page 227 and 228: PART IV: INTRODUCTION The manufactu

- Page 229 and 230: PART IV: 12 Figure 2: Main developm

- Page 231 and 232: PART IV: Firms’ characteristics F

- Page 233 and 234: PART IV: 3.2. Measurement and data

- Page 235 and 236: PART IV: high and high technologica

- Page 237 and 238: PART IV: study. Firstly, companies

- Page 239 and 240: PART IV: and Consumption Studies, U

- Page 241 and 242: PART IV: medium-sized enterprises,

- Page 243 and 244: PART IV: Balkan transition economie

- Page 245 and 246: PART IV: evidence that human capita

- Page 247 and 248: PART IV: of involving Serbia in a u

- Page 249 and 250: PART IV: REFERENCES Arandarenko, M.

- Page 252 and 253:

CEFTA-2006 AND ANHANCING COMPETITIV

- Page 254 and 255:

CEFTA-2006 AND ANHANCING COMPETITIV

- Page 256 and 257:

CEFTA-2006 AND ANHANCING COMPETITIV

- Page 258 and 259:

CEFTA-2006 AND ANHANCING COMPETITIV

- Page 260:

CEFTA-2006 AND ANHANCING COMPETITIV

- Page 263 and 264:

PART IV: INTRODUCTION Air transport

- Page 265 and 266:

PART IV: 2. Air transport market Ge

- Page 267 and 268:

PART IV: Finally, it is necessary t

- Page 269 and 270:

PART IV: Figure 2: PSO routes conne

- Page 271 and 272:

PART IV: 2012), and 9% lower in the

- Page 273 and 274:

PART IV: b) Second phase from 2011

- Page 275 and 276:

PART IV: IATA Passenger Forecast (2

- Page 277 and 278:

PART IV: determined by legal rules

- Page 279 and 280:

PART IV: Congress in 1985. As a con

- Page 281 and 282:

PART IV: 4. The rule of law and ind

- Page 283 and 284:

PART IV: the establishment of the r

- Page 285 and 286:

PART IV: REFERENCES Barro, R. (1991

- Page 287 and 288:

PART V: the association process ear

- Page 289 and 290:

PART V: Figure 3: EU FDI outward fl

- Page 291 and 292:

PART V: (macroeconomic stability an

- Page 293 and 294:

PART V: FDIPC- logarithm value of t

- Page 295 and 296:

PART V: DIST shows that if the dist

- Page 297 and 298:

PART V: University Press. Deichmann

- Page 299 and 300:

PART V: developing countries, where

- Page 301 and 302:

PART V: Figure 2: FDI inflow distri

- Page 303 and 304:

PART V: The economic literature usu

- Page 305 and 306:

PART V: The regression equation, wi

- Page 307 and 308:

PART V: Table 1. Determinants of FD

- Page 309 and 310:

PART V: The key determinants that w

- Page 311 and 312:

PART V: REFERENCES Liebscher, K. (2

- Page 313 and 314:

PART V: INTRODUCTION In the conditi

- Page 315 and 316:

PART V: from government regarding a

- Page 317 and 318:

PART V: 306 3.1. Comparative analys

- Page 319 and 320:

PART V: are sufficiently developed.

- Page 321 and 322:

PART V: monopolistic companies is e

- Page 323 and 324:

PART V: Savić Lj., (2008.), Inostr

- Page 325 and 326:

PART V: abandoned CEFTA membership)

- Page 327 and 328:

PART V: Figure 1: FDI in selected c

- Page 329 and 330:

PART V: 318 Table 3: Balance of pay

- Page 331 and 332:

PART V: come true if stable politic

- Page 333 and 334:

PART V: The task of the effective u

- Page 335 and 336:

PART V: Cooperation between the pub

- Page 337 and 338:

PART V: needs of Serbia and in that

- Page 339 and 340:

PART V: conventional production and

- Page 341 and 342:

PART V: REFERENCES Bandiera, O., Ca

- Page 343 and 344:

PART V: stability and macroeconomic

- Page 345 and 346:

PART V: By economic activity, the m

- Page 347 and 348:

PART V: Table 3: Exports and import

- Page 349 and 350:

PART V: In the last years, a series

- Page 351 and 352:

PART V: Figure 4: Balance of paymen

- Page 353 and 354:

PART V: because the level of per ca