4. Constructionmanagement3. LeasingIntensive bidding 2. Design and pre-construction activity means growth potential1. Planning and permittingTimeTimeIn <strong>Skanska</strong>’s business plan for <strong>2011</strong>–2015, the ambition is to increase investments in infrastructureprojects. This growth will18–36occurmonthswhile maintaining the same turnover rate in the project portfolio. Thegood potential returns of these operations were demonstrated well by the divestment of the AutopistaCentral highway in Chile, which also resulted in an extra dividend to <strong>Skanska</strong>’s shareholders.Value creation in infrastructure developmentAchieving financial close is the first andlargest step in value creation.Valuestart avfasFinancialcloseConstructionRamp upof operationsValue creation step by stepIn public-private partnership projects, <strong>Skanska</strong> is involved in the entiredevelopment chain from design and financing to construction, operationand maintenance. By assuming this overall responsibility, <strong>Skanska</strong>optimizes both construction and operating costs.The selection process is crucial to <strong>Skanska</strong>. Projects must be in productsegments and markets where <strong>Skanska</strong> has proficiency and experience.They must of course also meet the yield requirements that <strong>Skanska</strong> hasestablished. <strong>Skanska</strong> performs a thorough examination of risks andopportunities, in close collaboration with the Group’s construction units.This results in a selection process in which <strong>Skanska</strong> focuses on a limitednumber of projects. <strong>Skanska</strong> usually forms a bidding consortium withone or more partners. After the consortium’s bid has been successful,final negotiations with the customer and potential financiers begin.When binding contracts have been signed, usually at financial close, theassignment is included in the order bookings of the construction unit.TidQualifyIdentifyBid and negotiateProject Development0−2 yearsAsset Management3−10 yearsTimeGenerating value<strong>Skanska</strong>’s Infrastructure Development operations focuson three segments – highways including bridges and tunnels,social infrastructure such as hospitals and schoolsand utilities such as power generation stations. <strong>Skanska</strong>is involved in the entire value chain from project designto operation and maintenance, which implies a gradualreduction in the risk level of projects. Its business model isbased on investing in long-term projects that increase invalue upon completion, thereby enabling <strong>Skanska</strong> to sellthem to investors that are interested in long-term, stablecash flows when the projects are in operation. <strong>Skanska</strong>’sambition is to expand its operations in the public-privatepartnership (PPP) sector.Public-private partnerships mean that private marketplayers provide facilities and buildings to public agencies.This implies a number of macroeconomic advantagesfor customers, taxpayers, users and builders. The modelmakes more room for investments in public facilities byspreading the cost of large investments over longer periods.PPP projects create value for <strong>Skanska</strong> by generatinglarge construction assignments as well as potential capitalgains from divestment of completed projects, as shown in<strong>Skanska</strong>’s business model on page 8.In addition to construction assignments, in many cases<strong>Skanska</strong> is also responsible for long-term service and maintenanceassignments. <strong>Skanska</strong> Infrastructure Developmentcreates assets characterized by reliable cash flowslasting many years, once “steady state” (the operationphase) begins.MarketThe market for PPP projects was characterized by intensivebidding activity during <strong>2011</strong>. Meanwhile the processesfor major projects are generally lengthy. This makes itdifficult to estimate at what point in time they will resultin concrete projects. For some years the United Kingdomhas been the biggest market for PPP solutions, but due tocutbacks in the government budget the supply of newPPP projects has diminished in the British market.RevenueRevenue in <strong>Skanska</strong> Infrastructure Development comesmainly from <strong>Skanska</strong>’s share of income in the companiesthat own assets in the project portfolio. Expenses consistmainly of bidding costs and the cost of <strong>Skanska</strong>’s ownemployees. When these companies are divested, <strong>Skanska</strong>reports only the gain on the sale, or development gain,directly in operating income. Since <strong>Skanska</strong> owns minorityholdings in these companies, no revenue is recognized.EarningsOperating income in <strong>Skanska</strong> Infrastructure Developmentamounted to SEK 4,726 M (297). This includes gains of66 Infrastructure Development <strong>Skanska</strong> <strong>Annual</strong> <strong>Report</strong> <strong>2011</strong>

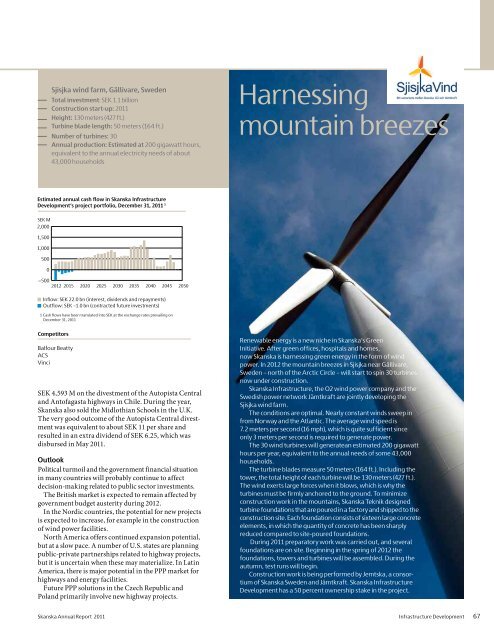

Årligt bedömt kassaflöde i <strong>Skanska</strong> Infrastrukturutvecklingsprojektportfölj per 31 december <strong>2011</strong> 1)Mkr2 0001 500 Sjisjka wind farm, Gällivare, Sweden1 000Total investment: SEK 1.1 billionConstruction start-up: <strong>2011</strong>500Height: 130 meters (427 ft.)0Turbine blade length: 50 meters (164 ft.)−500 Number of turbines: 302012 2015 2020 2025 2030 2035 2040 2045 2050<strong>Annual</strong> production: Estimated at 200 gigawatt hours,Inflöde: 22,0 Mdr kr (räntor, utdelningar och återbetalningar)equivalent to the annual electricity needs of about• Utflöde: −1,0 Mdr kr (framtida kontrakterade investeringar)43,000 households1) Kassaflödena är omräknade till valutakurserna per den 31 december <strong>2011</strong>3 0002 500Harnessingmountain breezes2 0001 5001 0005000−500<strong>2011</strong> 20152020202520302035204020452050Estimated annual cash flow in <strong>Skanska</strong> InfrastructureDevelopment’s project portfolio, December 31, <strong>2011</strong> 1SEK M2,000200015001,50010001,00050050000−5002012 20152020202520302035204020452050-5002012 20152020202520302035204020452050Inflow: SEK 22.0 bn (interest, dividends and repayments)• Outflow: SEK –1.0 bn (contracted future investments)1 Cash flows have been translated into SEK at the exchange rates prevailing onDecember 31, <strong>2011</strong>CompetitorsBalfour BeattyACSVinciSEK 4,593 M on the divestment of the Autopista Centraland Antofagasta highways in Chile. During the year,<strong>Skanska</strong> also sold the Midlothian Schools in the U.K.The very good outcome of the Autopista Central divestmentwas equivalent to about SEK 11 per share andresulted in an extra dividend of SEK 6.25, which wasdisbursed in May <strong>2011</strong>.OutlookPolitical turmoil and the government financial situationin many countries will probably continue to affectdecision-making related to public sector investments.The British market is expected to remain affected bygovernment budget austerity during 2012.In the Nordic countries, the potential for new projectsis expected to increase, for example in the constructionof wind power facilities.North America offers continued expansion potential,but at a slow pace. A number of U.S. states are planningpublic-private partnerships related to highway projects,but it is uncertain when these may materialize. In LatinAmerica, there is major potential in the PPP market forhighways and energy facilities.Future PPP solutions in the Czech Republic andPoland primarily involve new highway projects.Renewable energy is a new niche in <strong>Skanska</strong>’s GreenInitiative. After green offices, hospitals and homes,now <strong>Skanska</strong> is harnessing green energy in the form of windpower. In 2012 the mountain breezes in Sjisjka near Gällivare,Sweden – north of the Arctic Circle – will start to spin 30 turbinesnow under construction.<strong>Skanska</strong> Infrastructure, the O2 wind power company and theSwedish power network Jämtkraft are jointly developing theSjisjka wind farm.The conditions are optimal. Nearly constant winds sweep infrom Norway and the Atlantic. The average wind speed is7.2 meters per second (16 mph), which is quite sufficient sinceonly 3 meters per second is required to generate power.The 30 wind turbines will generatean estimated 200 gigawatthours per year, equivalent to the annual needs of some 43,000households.The turbine blades measure 50 meters (164 ft.). Including thetower, the total height of each turbine will be 130 meters (427 ft.).The wind exerts large forces when it blows, which is why theturbines must be firmly anchored to the ground. To minimizeconstruction work in the mountains, <strong>Skanska</strong> Teknik designedturbine foundations that are poured in a factory and shipped to theconstruction site. Each foundation consists of sixteen large concreteelements, in which the quantity of concrete has been sharplyreduced compared to site-poured foundations.During <strong>2011</strong> preparatory work was carried out, and severalfoundations are on site. Beginning in the spring of 2012 thefoundations, towers and turbines will be assembled. During theautumn, test runs will begin.Construction work is being performed by Jemtska, a consortiumof <strong>Skanska</strong> Sweden and Jämtkraft. <strong>Skanska</strong> InfrastructureDevelopment has a 50 percent ownership stake in the project.<strong>Skanska</strong> <strong>Annual</strong> <strong>Report</strong> <strong>2011</strong> Infrastructure Development 67

- Page 1 and 2:

Annual Report 2011

- Page 4 and 5:

NordenÖvriga EuropaIntäkterByggve

- Page 6:

2011 in briefFirst quarterSecond qu

- Page 9 and 10:

In Central Europe, our new green of

- Page 11 and 12:

”The business plan for 2011-2015

- Page 13 and 14:

Return on capital employed 2007−2

- Page 15 and 16:

20,000students participated.Safe ro

- Page 17 and 18:

per day to the blogenabled the gene

- Page 19 and 20: ”The divestment of the Group’s

- Page 21 and 22: Skanska uses a Groupwide procedure

- Page 23 and 24: New Karolinska Solna (NKS) , a univ

- Page 25 and 26: A day on the job with John Crecco,

- Page 27: A day on the job with Cecilia Fasth

- Page 30 and 31: 20 00010 00001999 2000 2001 2002 20

- Page 32 and 33: Above left: United Nations Headquar

- Page 34 and 35: Andel av orderstockenIncreased orde

- Page 36 and 37: Nordic countriesAndel av orderstock

- Page 38 and 39: Partihall InterchangeLength: 1,150

- Page 40 and 41: Other European countriesAndel av or

- Page 42 and 43: Heron TowerAddress: 110 Bishopsgate

- Page 44 and 45: The AmericasAndel av orderstockenUS

- Page 46 and 47: 1960 - 20111960: Karl Koch Erecting

- Page 48 and 49: Above left: Adjutantti, Helsinki, F

- Page 50 and 51: New Planläggning markets in Poland

- Page 52 and 53: Nordic countriesSwedenNorwayFinland

- Page 54 and 55: Other European countriesPolandCzech

- Page 56 and 57: Above left: Deloitte House, Warsaw,

- Page 58 and 59: 4. Byggande5. Förvaltning3. Uthyrn

- Page 60 and 61: Norden Europa AmerikaFördelningout

- Page 62 and 63: LustgårdenKvarteret Lustgården, L

- Page 64 and 65: EuropaAmerikaFördelningFördelning

- Page 66 and 67: AmerikaFördelningoutnyttjade Unite

- Page 68 and 69: Above left: London Hospital, London

- Page 72 and 73: Bedömt bruttonuvärdeGeografiKateg

- Page 74 and 75: A1 Expressway, PolandRoute: Gdańsk

- Page 76 and 77: Top left: Čertovo břemeno golf cl

- Page 78 and 79: Skanska’s Journey to Deep Green a

- Page 80 and 81: Initiatives in the carbon fieldThan

- Page 82 and 83: 876543210Skanska decided at an earl

- Page 84 and 85: 200100Skanska takes the lead0200420

- Page 86 and 87: Mdr kr175175The Board of Directors

- Page 88 and 89: Operating incomeSEK M 2011 2010Oper

- Page 90 and 91: Investments/DivestmentsSEK M 2011 2

- Page 92 and 93: Certain counterparties − for exam

- Page 94 and 95: The members and deputy members of t

- Page 96 and 97: Aside from day-to-day operations of

- Page 98 and 99: local management teams and were app

- Page 100 and 101: Consolidated income statementSEK M

- Page 102 and 103: Consolidated statement of financial

- Page 104 and 105: Consolidated statement of changes i

- Page 106 and 107: Consolidated cash flow statementCon

- Page 108 and 109: Parent Company balance sheetSEK M N

- Page 110 and 111: Parent Company cash flow statementS

- Page 112 and 113: Note01Consolidated accounting and v

- Page 114 and 115: Note01Continuedcontract premium is

- Page 116 and 117: Note01Continuedintended manner. Exa

- Page 118 and 119: Note01ContinuedIf the terms of a de

- Page 120 and 121:

of transfers of resources to a comp

- Page 122 and 123:

Note04Continued2011 ConstructionRes

- Page 124 and 125:

Note04ContinuedExternal revenue by

- Page 126 and 127:

Note06ContinuedSEK M Maturity Curre

- Page 128 and 129:

06NoteContinuedThe role of financia

- Page 130 and 131:

Note06ContinuedReconciliation with

- Page 132 and 133:

06NoteContinuedCollateralThe Group

- Page 134 and 135:

Note08RevenueNoteProjects in Skansk

- Page 136 and 137:

Note13Impairment losses/Reversals o

- Page 138 and 139:

Note16ContinuedTax assets and tax l

- Page 140 and 141:

Note18GoodwillGoodwill is recognize

- Page 142 and 143:

Note20Investments in joint ventures

- Page 144 and 145:

Note20ContinuedInformation on the G

- Page 146 and 147:

Note22Current-asset properties/Proj

- Page 148 and 149:

Note26Equity/earnings per shareIn t

- Page 150 and 151:

Note27Financial liabilitiesNoteFina

- Page 152 and 153:

NotePension obligations2011 2010Jan

- Page 154 and 155:

Note31Specification of interest-bea

- Page 156 and 157:

Note33Assets pledged, contingent li

- Page 158 and 159:

34NoteContinuedConsolidated stateme

- Page 160 and 161:

35NoteContinuedRelation between con

- Page 162 and 163:

Note37Remuneration to senior execut

- Page 164 and 165:

37NoteContinuedRemuneration and ben

- Page 166 and 167:

NoteThe dilution effect through 201

- Page 168 and 169:

Note42Consolidatedquarterly results

- Page 170 and 171:

Note43Five-yearGroup financial summ

- Page 172 and 173:

Financial ratios etc. 4, 5 Dec 31,

- Page 174 and 175:

Parent Company notes45NoteFinancial

- Page 176 and 177:

Note51Financial non-current assets,

- Page 178 and 179:

Note58Liabilities, Parent CompanyLi

- Page 180 and 181:

Note63Related party disclosures, Pa

- Page 182 and 183:

Auditors’ ReportTo the Annual Sha

- Page 184 and 185:

180 Notes, including accounting and

- Page 186 and 187:

Senior Executive TeamJohan Karlstr

- Page 188 and 189:

Board of DirectorsSverker Martin-L

- Page 190 and 191:

Major events during 2011This page s

- Page 192 and 193:

Below are the investments, divestme

- Page 194 and 195:

Definitions and explanationsAverage

- Page 196 and 197:

Annual Shareholders’ MeetingInves

- Page 198 and 199:

1887 Aktiebolaget Skånska Cementgj

- Page 200:

Skanska ABwww.skanska.comRåsundav