Note 28Provisions for pensions and similar commitmentsEffective from January 1, <strong>2003</strong>, <strong>Skanska</strong> applies the Swedish Financial AccountingStandards Council’s recommendation RR 29, ”Employee benefits,” which is basedon IAS 19.Pension liability according to the balance sheetGroupParent company<strong>2003</strong> 2002 <strong>2003</strong> 2002Interest-bearing pension liability 1 1,926 657 44 116Other pension obligations 132 327 237 247Total 2,058 984 281 3631 For the Parent Company: PRI liability in compliance with the Security of Income Act.<strong>Skanska</strong> has defined-benefit pension plans in Sweden, Norway, the United Kingdomand the United States. The pension in these plans is mainly based on final salary.The plans include a large number of employees, but <strong>Skanska</strong> also has definedcontributionplans in these countries. Group subsidiaries in other countries mainlyhave defined-contribution plans.Defined-benefit plansThe pension plans mainly consist of retirement pensions. Each respective employerusually has an obligation to pay a lifetime pension. Benefits are based on thenumber of years of employment. The employee must belong to the plan for acertain number of years to earn full retirement pension entitlement. For each year,the employee earns increased pension entitlements, which is reported as pensionearned during the period plus an increase in pension obligation.Pension plans are funded by securing pension obligations with assets in pensionfunds and provisions in the balance sheet. Funding occurs through payments fromthe respective Group companies and in some cases the employees.The managed assets in each pension fund are smaller than the pension obligation.For this reason, the difference is reported as a liability in the balance sheet. Theceiling rule that, in some cases, limits the value of these assets in the balance sheetdoes not apply when managed assets are smaller than pension obligations.Actuarial gains and losses are not reported in the <strong>2003</strong> income statement andbalance sheet, because <strong>Skanska</strong> applies the ”corridor” rules. These rules mean thata portion of actuarial gains and losses shall be reported in the income statementand the balance sheet in the coming period if they exceed the higher of:1) 10% of the present value of the pension obligation2) 10% of the fair value of managed assetsActuarial gains on managed assets and pension obligations amounted to SEK 0M at the beginning of <strong>2003</strong>. At the end of the year, actuarial gains amounted toapproximately 4% of the present value of pension obligations.The return on managed assets reported in the income statement amounted toSEK 292 M, while actual return amounted to SEK 512 M.The managed assets consist mainly of equities, interest-bearing securities andmutual fund units. An insignificant percentage of shareholdings consists of <strong>Skanska</strong>shares.The ITP occupational pension plan in Sweden is a defined-benefit plan. Aninsignificant portion is secured by insurance from the retirement insurance companyAlecta. This is a multi-employer insurance plan, and there is insufficient informationto report these obligations as a defined- benefit plan. Pensions secured by insurancefrom Alecta aretherefore reported as a defined-contribution plan.Trade union-sponsored plans in the United States are defined-benefit plans thatcover multiple employers. Since there is insufficient information to report theseobligations as defined-benefit plans, they are reported as defined-contributionplans.Defined-contribution plansThese plans mainly cover retirement pensions, disability pensions and familypensions. The premiums are paid regularly during the year by the respective Groupcompany to separate legal entities, for example insurance companies. The size ofthe premium is based on salary. The pension expense for the period is included inthe income statement.Commitments related to employee benefits, defined-benefit plansComparative figures are not stated, since these pensions are reported in compliancewith RR 29 effective from January 1, <strong>2003</strong>.Group <strong>2003</strong>Pension commitments, funded plans, present value on December 31 6,567Managed assets, actual value on December 31 –4,929Total 1,638Unreported actuarial gains (+), losses (–), managed assets 220Unreported acuarial gains (+), losses (–), pension commitments 68Net liability according to balance sheet 1,926Total pension expensesGroup <strong>2003</strong>Pensions earned during the period 393Less: Funds supplied by employees –34Interest on commitments 330Expected return on managed assets –292Pension expenses, defined-benefit plans 397Pension expenses, defined-contribution plans 531Employer social welfare contributions, defined-benefitand defined-contribution plans 76Total pension expenses 1,004Pension commitmentsGroup <strong>2003</strong>Opening balance, January 1 6,446Pensions earned during the period 393Interest on commitments 330Benefits paid –182Reclassification 105Unreported actuarial gains (–), losses (+), pension commitments –68Exchange rate differences –457Pension commitments, present value 6,567Managed assetsGroup <strong>2003</strong>Opening balance, January 1 4,460Expected return on managed assets 292Funds supplied by employers 240Funds supplied by employees 34Unreported actuarial gains (–), losses (+), pension commitments 220Exchange rate differences –317Managed assets, actual value 4,929Reconciliation of net liabilityGroup <strong>2003</strong>Opening balance, January 1, pension liabilities 1 657Pension expenses 397Benefits paid –182Funds supplied by employers –240Change in accounting principle 1 635Reclassification –201Exchange rate differences –140Net liability according to balance sheet 1,9261 Opening balance of pension laibilities according to local rules in each respective country.Actuarial assumptionsGroup Sweden Norway U.K. USA Average 1Discount rate, January 1 5.75% 6.00% 5.50% 5.50% 5.70%Discount rate. December 31 5.75% 5.50% 5.50% 5.50% 5.60%Expected return on managed assets 6.50% 6.40% 7.10% 6.50% 6.65%– of which, equities 8.00% 9.50% 7.50% 8.00% 8.15%– of which, interest-bearing securities 5.00% 6.00% 4.50% 4.00% 5.00%Expected wage and salary increase 3.00% 3.30% 3.85% 4.40% 3.40%Expected inflation 2.00% 2.50% 2.35% 2.90% 2.25%1 Weighted average.72 Notes, including accounting and valuation principles – <strong>Skanska</strong> <strong>Annual</strong> <strong>Report</strong> <strong>2003</strong>

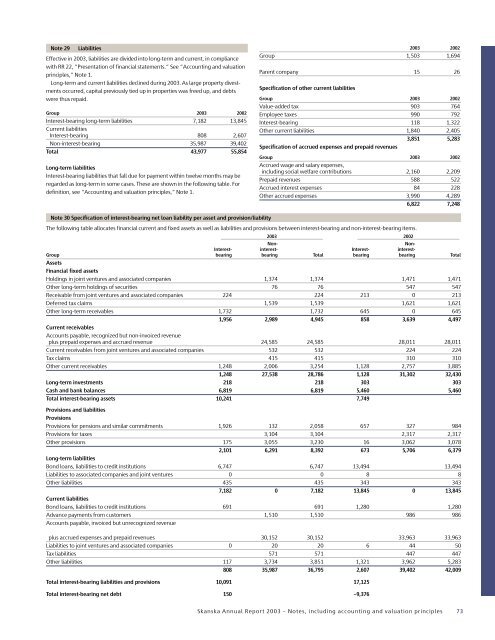

Note 29LiabilitiesEffective in <strong>2003</strong>, liabilities are divided into long-term and current, in compliancewith RR 22, ”Presentation of financial statements.” See ”Accounting and valuationprinciples,” Note 1.Long-term and current liabilities declined during <strong>2003</strong>. As large property divestmentsoccurred, capital previously tied up in properties was freed up, and debtswere thus repaid.Group <strong>2003</strong> 2002Interest-bearing long-term liabilities 7,182 13,845Current liabilitiesInterest-bearing 808 2,607Non-interest-bearing 35,987 39,402Total 43,977 55,854Long-term liabilitiesInterest-bearing liabilities that fall due for payment within twelve months may beregarded as long-term in some cases. These are shown in the following table. Fordefinition, see ”Accounting and valuation principles,” Note 1.<strong>2003</strong> 2002Group 1,503 1,694Parent company 15 26Specification of other current liabilitiesGroup <strong>2003</strong> 2002Value-added tax 903 764Employee taxes 990 792Interest-bearing 118 1,322Other current liabilities 1,840 2,4053,851 5,283Specification of accrued expenses and prepaid revenuesGroup <strong>2003</strong> 2002Accrued wage and salary expenses,including social welfare contributions 2,160 2,209Prepaid revenues 588 522Accrued interest expenses 84 228Other accrued expenses 3,990 4,2896,822 7,248Note 30 Specification of interest-bearing net loan liability per asset and provision/liabilityThe following table allocates financial current and fixed assets as well as liabilities and provisions between interest-bearing and non-interest-bearing items.<strong>2003</strong> 2002Non-Non-Interest- interest- Interest- interest-Group bearing bearing Total bearing bearing TotalAssetsFinancial fixed assetsHoldings in joint ventures and associated companies 1,374 1,374 1,471 1,471Other long-term holdings of securities 76 76 547 547Receivable from joint ventures and associated companies 224 224 213 0 213Deferred tax claims 1,539 1,539 1,621 1,621Other long-term receivables 1,732 1,732 645 0 6451,956 2,989 4,945 858 3,639 4,497Current receivablesAccounts payable, recognized but non-invoiced revenueplus prepaid expenses and accrued revenue 24,585 24,585 28,011 28,011Current receivables from joint ventures and associated companies 532 532 224 224Tax claims 415 415 310 310Other current receivables 1,248 2,006 3,254 1,128 2,757 3,8851,248 27,538 28,786 1,128 31,302 32,430Long-term investments 218 218 303 303Cash and bank balances 6,819 6,819 5,460 5,460Total interest-bearing assets 10,241 7,749Provisions and liabilitiesProvisionsProvisions for pensions and similar commitments 1,926 132 2,058 657 327 984Provisions for taxes 3,104 3,104 2,317 2,317Other provisions 175 3,055 3,230 16 3,062 3,0782,101 6,291 8,392 673 5,706 6,379Long-term liabilitiesBond loans, liabilities to credit institutions 6,747 6,747 13,494 13,494Liabilities to associated companies and joint ventures 0 0 8 8Other liabilities 435 435 343 3437,182 0 7,182 13,845 0 13,845Current liabilitiesBond loans, liabilities to credit institutions 691 691 1,280 1,280Advance payments from customers 1,510 1,510 986 986Accounts payable, invoiced but unrecognized revenueplus accrued expenses and prepaid revenues 30,152 30,152 33,963 33,963Liabilities to joint ventures and associated companies 0 20 20 6 44 50Tax liabilities 571 571 447 447Other liabilities 117 3,734 3,851 1,321 3,962 5,283808 35,987 36,795 2,607 39,402 42,009Total interest-bearing liabilities and provisions 10,091 17,125Total interest-bearing net debt 150 –9,376<strong>Skanska</strong> <strong>Annual</strong> <strong>Report</strong> <strong>2003</strong> – Notes, including accounting and valuation principles 73