Jahresabschluss der Investkredit-Gruppe 2008 ... - Volksbank AG

Jahresabschluss der Investkredit-Gruppe 2008 ... - Volksbank AG

Jahresabschluss der Investkredit-Gruppe 2008 ... - Volksbank AG

Erfolgreiche ePaper selbst erstellen

Machen Sie aus Ihren PDF Publikationen ein blätterbares Flipbook mit unserer einzigartigen Google optimierten e-Paper Software.

<strong>Investkredit</strong> Annual Report<br />

Notes – Other Details and Risk Report <strong>2008</strong><br />

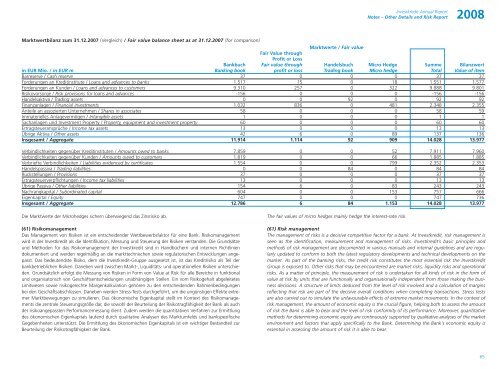

Marktwertbilanz zum 31.12.2007 (Vergleich) / Fair value balance sheet as at 31.12.2007 (for comparison)<br />

Marktwerte / Fair value<br />

Bankbuch<br />

Fair Value through<br />

Profit or Loss<br />

Fair value through Handelsbuch Micro Hedge Summe Bilanzwert<br />

in EUR Mio. / in EUR m Banking book profit or loss Trading book Micro hedge Total Value of item<br />

Barreserve / Cash reserve 37 0 0 0 37 37<br />

For<strong>der</strong>ungen an Kreditinstitute / Loans and advances to banks 1.517 15 0 18 1.551 1.577<br />

For<strong>der</strong>ungen an Kunden / Loans and advances to customers 9.310 257 0 322 9.888 9.801<br />

Risikovorsorge / Risk provisions for loans and advances -156 0 0 0 -156 -156<br />

Handelsaktiva / Trading assets 0 0 92 0 92 92<br />

Finanzanlagen / Financial investments 1.032 836 0 481 2.348 2.355<br />

Anteile an assozierten Unternehmen / Shares in associates 58 0 0 0 58 59<br />

Immaterielles Anlagevermögen / Intangible assets 1 0 0 0 1 1<br />

Sachanlagen und Investment Property / Property, equipment and investment property 60 0 0 0 60 60<br />

Ertragsteueransprüche / Income tax assets 13 0 0 0 13 13<br />

Übrige Aktiva / Other assets 42 6 0 89 137 136<br />

Insgesamt / Aggregate 11.914 1.114 92 909 14.028 13.977<br />

Verbindlichkeiten gegenüber Kreditinstituten / Amounts owed to banks 7.859 0 0 52 7.911 7.960<br />

Verbindlichkeiten gegenüber Kunden / Amounts owed to customers 1.819 0 0 66 1.885 1.885<br />

Verbriefte Verbindlichkeiten / Liabilities evidenced by certificates 1.554 0 0 799 2.352 2.353<br />

Handelspassiva / Trading liabilities 0 0 84 0 84 84<br />

Rückstellungen / Provisions 37 0 0 0 37 37<br />

Ertragsteuerverpflichtungen / Income tax liabilities 13 0 0 0 13 13<br />

Übrige Passiva / Other liabilities 154 6 0 83 243 243<br />

Nachrangkapital / Subordinated capital 604 0 0 153 757 666<br />

Eigenkapital / Equity 747 0 0 0 747 736<br />

Insgesamt / Aggregate 12.786 6 84 1.153 14.028 13.977<br />

Die Marktwerte <strong>der</strong> Microhedges sichern überwiegend das Zinsrisiko ab.<br />

(61) Risikomanagement<br />

Das Management von Risiken ist ein entscheiden<strong>der</strong> Wettbewerbsfaktor für eine Bank. Risikomanagement<br />

wird in <strong>der</strong> <strong>Investkredit</strong> als die Identifikation, Messung und Steuerung <strong>der</strong> Risiken verstanden. Die Grundsätze<br />

und Methoden für das Risikomanagement <strong>der</strong> <strong>Investkredit</strong> sind in Handbüchern und internen Richtlinien<br />

dokumentiert und werden regelmäßig an die markttechnischen sowie regulatorischen Entwicklungen angepasst.<br />

Das bedeutendste Risiko, dem die <strong>Investkredit</strong>-<strong>Gruppe</strong> ausgesetzt ist, ist das Kreditrisiko als Teil <strong>der</strong><br />

bankbetrieblichen Risiken. Daneben wird zwischen Markt-, Liquiditäts- und operationellen Risiken unterschieden.<br />

Grundsätzlich erfolgt die Messung von Risiken in Form von Value at Risk für alle Bereiche in funktional<br />

und organisatorisch von Geschäftsentscheidungen unabhängigen Stellen. Ein vom Risikogehalt abgeleitetes<br />

Limitwesen sowie risikogerechte Margenkalkulation gehören zu den entscheidenden Rahmenbedingungen<br />

bei den Geschäftsabschlüssen. Daneben werden Stress-Tests durchgeführt, um die ungünstigen Effekte extremer<br />

Marktbewegungen zu simulieren. Das ökonomische Eigenkapital stellt im Kontext des Risikomanagements<br />

die zentrale Steuerungsgröße dar, die sowohl <strong>der</strong> Beurteilung <strong>der</strong> Risikotragfähigkeit <strong>der</strong> Bank als auch<br />

<strong>der</strong> risikoangepassten Performancemessung dient. Zudem werden die quantitativen Verfahren zur Ermittlung<br />

des ökonomischen Eigenkapitals laufend durch qualitative Analysen des Marktumfelds und bankspezifische<br />

Gegebenheiten unterstützt. Die Ermittlung des ökonomischen Eigenkapitals ist ein wichtiger Bestandteil zur<br />

Beurteilung <strong>der</strong> Risikotragfähigkeit <strong>der</strong> Bank.<br />

The fair values of micro hedges mainly hedge the interest-rate risk.<br />

(61) Risk management<br />

The management of risks is a decisive competitive factor for a bank. At <strong>Investkredit</strong>, risk management is<br />

seen as the identification, measurement and management of risks. <strong>Investkredit</strong>’s basic principles and<br />

methods of risk management are documented in various manuals and internal guidelines and are regularly<br />

updated to conform to both the latest regulatory developments and technical developments on the<br />

market. As part of the banking risks, the credit risk constitutes the most essential risk the <strong>Investkredit</strong><br />

Group is exposed to. Other risks that may be encountered are market risks, liquidity risks and operational<br />

risks. As a matter of principle, the measurement of risk is un<strong>der</strong>taken for all kinds of risk in the form of<br />

value at risk by units that are functionally and organisationally independent from those making the business<br />

decisions. A structure of limits deduced from the level of risk involved and a calculation of margins<br />

reflecting that risk are part of the decisive overall conditions when completing transactions. Stress tests<br />

are also carried out to simulate the unfavourable effects of extreme market movements. In the context of<br />

risk management, the amount of economic equity is the crucial figure, helping both to assess the amount<br />

of risk the Bank is able to bear and the level of risk conformity of its performance. Moreover, quantitative<br />

methods for determining economic equity are continuously supported by qualitative analyses of the market<br />

environment and factors that apply specifically to the Bank. Determining the Bank’s economic equity is<br />

essential in assessing the amount of risk it is able to bear.<br />

65