Jahresabschluss der Investkredit-Gruppe 2008 ... - Volksbank AG

Jahresabschluss der Investkredit-Gruppe 2008 ... - Volksbank AG

Jahresabschluss der Investkredit-Gruppe 2008 ... - Volksbank AG

Erfolgreiche ePaper selbst erstellen

Machen Sie aus Ihren PDF Publikationen ein blätterbares Flipbook mit unserer einzigartigen Google optimierten e-Paper Software.

ge Vorgangsweisen und die Darstellung und Limitierung des Kreditrisikos. Die Kreditrisikolimite orientieren<br />

sich nach den internen Ratings und Laufzeiten und gelten sowohl für das Neugeschäft als auch für das bestehende<br />

Kreditportfolio. Konkrete Festlegungen sind in Organisationsregelungen, Bestimmungen <strong>der</strong> Aufbauorganisation,<br />

<strong>der</strong> Geschäftsordnung für den Vorstand und <strong>der</strong> Geschäftsordnung für den Kreditausschuss enthalten.<br />

Im Immobilienbereich ergibt sich das Kreditrisiko aus den Mietverpflichtungen. Der Ausfall eines Mieters und<br />

die dadurch entfallenen Mietzinszahlungen stellen eine barwertige Min<strong>der</strong>ung des Immobilienprojekts dar.<br />

Dieses Risiko wird auf Basis <strong>der</strong> Expertenschätzungen auf Projektebene mitberücksichtigt.<br />

Die Details zu den Risiken zusammen mit Performance-Kennzahlen werden in dem vierteljährlichen Kreditrisikobericht<br />

zusammengefasst, <strong>der</strong> als Steuerungsinstrument für das Kreditrisiko des Bankportfolios dient. Für<br />

die aktive Steuerung des Kreditrisikos mit dem Ziel <strong>der</strong> Maximierung <strong>der</strong> risikoadjustierten Rendite setzt die<br />

Bank vermehrt Instrumente wie Syndizierungen und Kredit<strong>der</strong>ivate ein.<br />

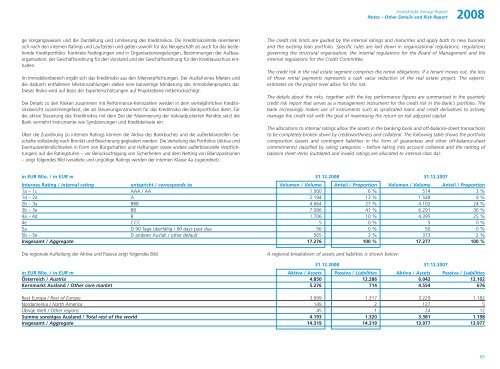

Über die Zuordnung zu internen Ratings können die Aktiva des Bankbuches und die außerbilanziellen Geschäfte<br />

vollständig nach Bonität und Besicherung geglie<strong>der</strong>t werden. Die Verteilung des Portfolios (Aktiva und<br />

Eventualverbindlichkeiten in Form von Bürgschaften und Haftungen sowie an<strong>der</strong>e außerbilanzielle Verpflichtungen)<br />

auf die Ratingstufen – vor Berücksichtigung von Sicherheiten und dem Netting von Bilanzpositionen<br />

– zeigt folgendes Bild (veraltete und ungültige Ratings werden <strong>der</strong> internen Klasse 4a zugeordnet):<br />

Die regionale Aufteilung <strong>der</strong> Aktiva und Passiva zeigt folgendes Bild:<br />

<strong>Investkredit</strong> Annual Report<br />

Notes – Other Details and Risk Report <strong>2008</strong><br />

The credit risk limits are guided by the internal ratings and maturities and apply both to new business<br />

and the existing loan portfolio. Specific rules are laid down in organisational regulations, regulations<br />

governing the structural organisation, the internal regulations for the Board of Management and the<br />

internal regulations for the Credit Committee.<br />

The credit risk in the real estate segment comprises the rental obligations. If a tenant moves out, the loss<br />

of those rental payments represents a cash value reduction of the real estate project. The experts’<br />

estimates on the project level allow for this risk.<br />

The details about the risks, together with the key performance figures are summarised in the quarterly<br />

credit risk report that serves as a management instrument for the credit risk in the Bank’s portfolio. The<br />

bank increasingly makes use of instruments such as syndicated loans and credit <strong>der</strong>ivatives to actively<br />

manage the credit risk with the goal of maximising the return on risk adjusted capital.<br />

The allocations to internal ratings allow the assets in the banking book and off-balance-sheet transactions<br />

to be completely broken down by creditworthiness and collateral. The following table shows the portfolio<br />

composition (assets and contingent liabilities in the form of guarantees and other off-balance-sheet<br />

commitments) classified by rating categories – before taking into account collateral and the netting of<br />

balance sheet items (outdated and invalid ratings are allocated to internal class 4a):<br />

in EUR Mio. / in EUR m 31.12.<strong>2008</strong> 31.12.2007<br />

Internes Rating / internal rating entspricht / corresponds to Volumen / Volume Anteil / Proportion Volumen / Volume Anteil / Proportion<br />

1a – 1c AAA / AA 1.000 6 % 514 3 %<br />

1d – 2a A 2.194 13 % 1.548 9 %<br />

2b – 3a BBB 4.664 27 % 4.102 24 %<br />

3b – 3e BB 7.086 41 % 6.291 36 %<br />

4a – 4d B 1.706 10 % 4.395 25 %<br />

4e CCC 5 0 % 5 0 %<br />

5a D 90 Tage überfällig / 90 days past due 56 0 % 50 0 %<br />

5b – 5e D an<strong>der</strong>er Ausfall / other default 565 3 % 373 2 %<br />

Insgesamt / Aggregate 17.276 100 % 17.277 100 %<br />

A regional breakdown of assets and liablities is shown below:<br />

31.12.<strong>2008</strong> 31.12.2007<br />

in EUR Mio. / in EUR m Aktiva / Assets Passiva / Liabilities Aktiva / Assets Passiva / Liabilities<br />

Österreich / Austria 4.850 12.286 6.042 12.102<br />

Kernmarkt Ausland / Other core market 5.276 714 4.554 676<br />

Rest Europa / Rest of Europe 3.999 1.317 3.229 1.182<br />

Nordamerika / North America 149 2 127 5<br />

Übrige Welt / Other regions 45 1 24 12<br />

Summe sonstiges Ausland / Total rest of the world 4.193 1.320 3.381 1.198<br />

Insgesamt / Aggregate 14.319 14.319 13.977 13.977<br />

69