Deciding the Future: Energy Policy Scenarios to 2050

Deciding the Future: Energy Policy Scenarios to 2050

Deciding the Future: Energy Policy Scenarios to 2050

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

30<br />

<strong>Deciding</strong> <strong>the</strong> <strong>Future</strong>: <strong>Energy</strong> <strong>Policy</strong> <strong>Scenarios</strong> <strong>to</strong> <strong>2050</strong> World <strong>Energy</strong> Council 2007 Results of Analysis<br />

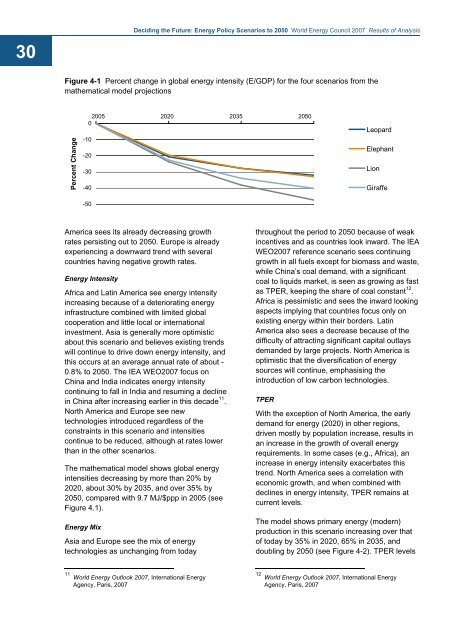

Figure 4-1 Percent change in global energy intensity (E/GDP) for <strong>the</strong> four scenarios from <strong>the</strong><br />

ma<strong>the</strong>matical model projections<br />

Percent Change<br />

2005 2020 2035 <strong>2050</strong><br />

0<br />

-10<br />

-20<br />

-30<br />

-40<br />

-50<br />

Leopard<br />

Elephant<br />

Lion<br />

Giraffe<br />

America sees its already decreasing growth<br />

rates persisting out <strong>to</strong> <strong>2050</strong>. Europe is already<br />

experiencing a downward trend with several<br />

countries having negative growth rates.<br />

<strong>Energy</strong> Intensity<br />

Africa and Latin America see energy intensity<br />

increasing because of a deteriorating energy<br />

infrastructure combined with limited global<br />

cooperation and little local or international<br />

investment. Asia is generally more optimistic<br />

about this scenario and believes existing trends<br />

will continue <strong>to</strong> drive down energy intensity, and<br />

this occurs at an average annual rate of about -<br />

0.8% <strong>to</strong> <strong>2050</strong>. The IEA WEO2007 focus on<br />

China and India indicates energy intensity<br />

continuing <strong>to</strong> fall in India and resuming a decline<br />

in China after increasing earlier in this decade 11 .<br />

North America and Europe see new<br />

technologies introduced regardless of <strong>the</strong><br />

constraints in this scenario and intensities<br />

continue <strong>to</strong> be reduced, although at rates lower<br />

than in <strong>the</strong> o<strong>the</strong>r scenarios.<br />

The ma<strong>the</strong>matical model shows global energy<br />

intensities decreasing by more than 20% by<br />

2020, about 30% by 2035, and over 35% by<br />

<strong>2050</strong>, compared with 9.7 MJ/$ppp in 2005 (see<br />

Figure 4.1).<br />

<strong>Energy</strong> Mix<br />

Asia and Europe see <strong>the</strong> mix of energy<br />

technologies as unchanging from <strong>to</strong>day<br />

throughout <strong>the</strong> period <strong>to</strong> <strong>2050</strong> because of weak<br />

incentives and as countries look inward. The IEA<br />

WEO2007 reference scenario sees continuing<br />

growth in all fuels except for biomass and waste,<br />

while China’s coal demand, with a significant<br />

coal <strong>to</strong> liquids market, is seen as growing as fast<br />

as TPER, keeping <strong>the</strong> share of coal constant 12 .<br />

Africa is pessimistic and sees <strong>the</strong> inward looking<br />

aspects implying that countries focus only on<br />

existing energy within <strong>the</strong>ir borders. Latin<br />

America also sees a decrease because of <strong>the</strong><br />

difficulty of attracting significant capital outlays<br />

demanded by large projects. North America is<br />

optimistic that <strong>the</strong> diversification of energy<br />

sources will continue, emphasising <strong>the</strong><br />

introduction of low carbon technologies.<br />

TPER<br />

With <strong>the</strong> exception of North America, <strong>the</strong> early<br />

demand for energy (2020) in o<strong>the</strong>r regions,<br />

driven mostly by population increase, results in<br />

an increase in <strong>the</strong> growth of overall energy<br />

requirements. In some cases (e.g., Africa), an<br />

increase in energy intensity exacerbates this<br />

trend. North America sees a correlation with<br />

economic growth, and when combined with<br />

declines in energy intensity, TPER remains at<br />

current levels.<br />

The model shows primary energy (modern)<br />

production in this scenario increasing over that<br />

of <strong>to</strong>day by 35% in 2020, 65% in 2035, and<br />

doubling by <strong>2050</strong> (see Figure 4-2). TPER levels<br />

11 World <strong>Energy</strong> Outlook 2007, International <strong>Energy</strong><br />

Agency, Paris, 2007<br />

12 World <strong>Energy</strong> Outlook 2007, International <strong>Energy</strong><br />

Agency, Paris, 2007