Deciding the Future: Energy Policy Scenarios to 2050

Deciding the Future: Energy Policy Scenarios to 2050

Deciding the Future: Energy Policy Scenarios to 2050

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Deciding</strong> <strong>the</strong> <strong>Future</strong>: <strong>Energy</strong> <strong>Policy</strong> <strong>Scenarios</strong> <strong>to</strong> <strong>2050</strong> World <strong>Energy</strong> Council 2007 Appendices<br />

95<br />

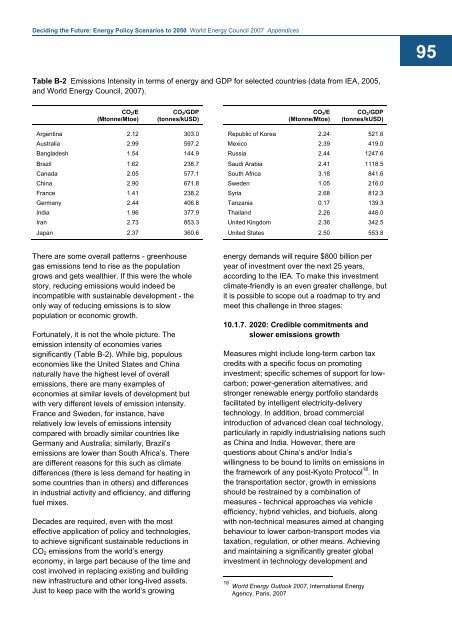

Table B-2 Emissions Intensity in terms of energy and GDP for selected countries (data from IEA, 2005,<br />

and World <strong>Energy</strong> Council, 2007).<br />

CO 2 /E<br />

(M<strong>to</strong>nne/M<strong>to</strong>e)<br />

CO 2 /GDP<br />

(<strong>to</strong>nnes/kUSD)<br />

CO 2 /E<br />

(M<strong>to</strong>nne/M<strong>to</strong>e)<br />

CO 2 /GDP<br />

(<strong>to</strong>nnes/kUSD)<br />

Argentina 2.12 303.0<br />

Australia 2.99 597.2<br />

Bangladesh 1.54 144.9<br />

Brazil 1.62 238.7<br />

Canada 2.05 577.1<br />

China 2.90 671.8<br />

France 1.41 238.2<br />

Germany 2.44 406.8<br />

India 1.96 377.9<br />

Iran 2.73 853.3<br />

Japan 2.37 360.6<br />

Republic of Korea 2.24 521.6<br />

Mexico 2.39 419.0<br />

Russia 2.44 1247.6<br />

Saudi Arabia 2.41 1118.5<br />

South Africa 3.18 841.6<br />

Sweden 1.05 216.0<br />

Syria 2.68 812.3<br />

Tanzania 0.17 139.3<br />

Thailand 2.26 448.0<br />

United Kingdom 2.36 342.5<br />

United States 2.50 553.8<br />

There are some overall patterns - greenhouse<br />

gas emissions tend <strong>to</strong> rise as <strong>the</strong> population<br />

grows and gets wealthier. If this were <strong>the</strong> whole<br />

s<strong>to</strong>ry, reducing emissions would indeed be<br />

incompatible with sustainable development - <strong>the</strong><br />

only way of reducing emissions is <strong>to</strong> slow<br />

population or economic growth.<br />

Fortunately, it is not <strong>the</strong> whole picture. The<br />

emission intensity of economies varies<br />

significantly (Table B-2). While big, populous<br />

economies like <strong>the</strong> United States and China<br />

naturally have <strong>the</strong> highest level of overall<br />

emissions, <strong>the</strong>re are many examples of<br />

economies at similar levels of development but<br />

with very different levels of emission intensity.<br />

France and Sweden, for instance, have<br />

relatively low levels of emissions intensity<br />

compared with broadly similar countries like<br />

Germany and Australia; similarly, Brazil’s<br />

emissions are lower than South Africa’s. There<br />

are different reasons for this such as climate<br />

differences (<strong>the</strong>re is less demand for heating in<br />

some countries than in o<strong>the</strong>rs) and differences<br />

in industrial activity and efficiency, and differing<br />

fuel mixes.<br />

Decades are required, even with <strong>the</strong> most<br />

effective application of policy and technologies,<br />

<strong>to</strong> achieve significant sustainable reductions in<br />

CO 2 emissions from <strong>the</strong> world’s energy<br />

economy, in large part because of <strong>the</strong> time and<br />

cost involved in replacing existing and building<br />

new infrastructure and o<strong>the</strong>r long-lived assets.<br />

Just <strong>to</strong> keep pace with <strong>the</strong> world’s growing<br />

energy demands will require $800 billion per<br />

year of investment over <strong>the</strong> next 25 years,<br />

according <strong>to</strong> <strong>the</strong> IEA. To make this investment<br />

climate-friendly is an even greater challenge, but<br />

it is possible <strong>to</strong> scope out a roadmap <strong>to</strong> try and<br />

meet this challenge in three stages:<br />

10.1.7. 2020: Credible commitments and<br />

slower emissions growth<br />

Measures might include long-term carbon tax<br />

credits with a specific focus on promoting<br />

investment; specific schemes of support for lowcarbon;<br />

power-generation alternatives; and<br />

stronger renewable energy portfolio standards<br />

facilitated by intelligent electricity-delivery<br />

technology. In addition, broad commercial<br />

introduction of advanced clean coal technology,<br />

particularly in rapidly industrialising nations such<br />

as China and India. However, <strong>the</strong>re are<br />

questions about China’s and/or India’s<br />

willingness <strong>to</strong> be bound <strong>to</strong> limits on emissions in<br />

<strong>the</strong> framework of any post-Kyo<strong>to</strong> Pro<strong>to</strong>col 18 . In<br />

<strong>the</strong> transportation sec<strong>to</strong>r, growth in emissions<br />

should be restrained by a combination of<br />

measures - technical approaches via vehicle<br />

efficiency, hybrid vehicles, and biofuels, along<br />

with non-technical measures aimed at changing<br />

behaviour <strong>to</strong> lower carbon-transport modes via<br />

taxation, regulation, or o<strong>the</strong>r means. Achieving<br />

and maintaining a significantly greater global<br />

investment in technology development and<br />

18 World <strong>Energy</strong> Outlook 2007, International <strong>Energy</strong><br />

Agency, Paris, 2007