Download PDF version English (3237KB) - Hamon

Download PDF version English (3237KB) - Hamon

Download PDF version English (3237KB) - Hamon

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Part 3 - Financial statements<br />

65<br />

liabilities and contingent liabilities recognized. The initial<br />

accounting for business combinations is not restated.<br />

Any adjustments to the consideration transferred<br />

in these business combinations changes their initial<br />

accounting and leads to a matching adjustment to<br />

goodwill.<br />

b. Business combinations carried out after<br />

1 January 2010<br />

Goodwill is measured as the excess of the aggregate of:<br />

(i) the consideration transferred;<br />

(ii) the amount of any non-controlling interests<br />

in the acquiree; and<br />

(iii) in a business combination achieved in stages, the<br />

acquisition-date fair value of the previously held<br />

equity interest in the acquiree;<br />

over the net of the acquisition-date fair values of the<br />

identifiable assets acquired and the liabilities assumed.<br />

Goodwill recognized on the acquisition date is not<br />

subsequently adjusted.<br />

Measurement of goodwill<br />

Goodwill is not depreciated but it is tested for impairment<br />

at least once a year. Any impairment loss is charged to<br />

the income statement. An impairment loss accounted<br />

for on goodwill cannot be reversed at a later date.<br />

At the time of the sale of a subsidiary or a jointly<br />

controlled entity, the relevant goodwill is included in the<br />

determination of the result of the sale. Goodwill on<br />

associated companies is presented under ‘Investments<br />

In Associated Companies’.<br />

3.4.2 Tangible Assets<br />

An item of property, plant and equipment is recognized<br />

as a tangible asset if it is probable that the future<br />

economic benefits attributable to the asset will flow to<br />

the Group and if their costs can be measured reliably.<br />

After the initial accounting, all tangible assets are<br />

stated at cost less the accumulated depreciation and<br />

impairment losses. The cost includes all the costs<br />

directly attributable to bringing the asset to the location<br />

and condition necessary for it to be capable of operating<br />

in the intended manner.<br />

Repair and maintenance costs and other subsequent<br />

expenditure linked to an asset are charged as expenses<br />

in the income statement of the financial year during<br />

which they are incurred.<br />

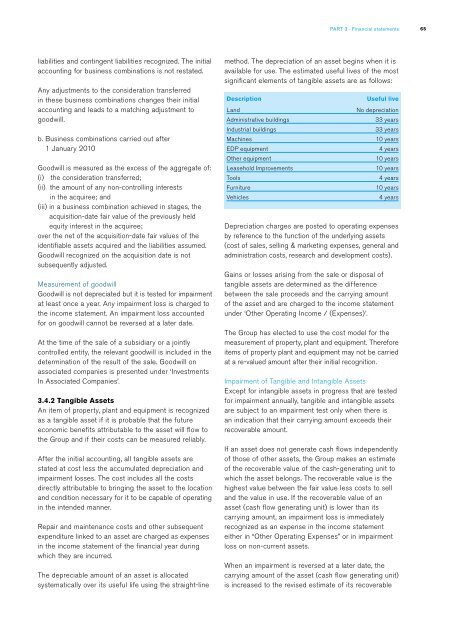

The depreciable amount of an asset is allocated<br />

systematically over its useful life using the straight-line<br />

method. The depreciation of an asset begins when it is<br />

available for use. The estimated useful lives of the most<br />

significant elements of tangible assets are as follows:<br />

Description<br />

Land<br />

Administrative buildings<br />

Industrial buildings<br />

Machines<br />

EDP equipment<br />

Other equipment<br />

Leasehold Improvements<br />

Tools<br />

Furniture<br />

Vehicles<br />

Useful live<br />

No depreciation<br />

33 years<br />

33 years<br />

10 years<br />

4 years<br />

10 years<br />

10 years<br />

4 years<br />

10 years<br />

4 years<br />

Depreciation charges are posted to operating expenses<br />

by reference to the function of the underlying assets<br />

(cost of sales, selling & marketing expenses, general and<br />

administration costs, research and development costs).<br />

Gains or losses arising from the sale or disposal of<br />

tangible assets are determined as the difference<br />

between the sale proceeds and the carrying amount<br />

of the asset and are charged to the income statement<br />

under ‘Other Operating Income / (Expenses)’.<br />

The Group has elected to use the cost model for the<br />

measurement of property, plant and equipment. Therefore<br />

items of property plant and equipment may not be carried<br />

at a re-valued amount after their initial recognition.<br />

Impairment of Tangible and Intangible Assets<br />

Except for intangible assets in progress that are tested<br />

for impairment annually, tangible and intangible assets<br />

are subject to an impairment test only when there is<br />

an indication that their carrying amount exceeds their<br />

recoverable amount.<br />

If an asset does not generate cash flows independently<br />

of those of other assets, the Group makes an estimate<br />

of the recoverable value of the cash-generating unit to<br />

which the asset belongs. The recoverable value is the<br />

highest value between the fair value less costs to sell<br />

and the value in use. If the recoverable value of an<br />

asset (cash flow generating unit) is lower than its<br />

carrying amount, an impairment loss is immediately<br />

recognized as an expense in the income statement<br />

either in “Other Operating Expenses” or in impairment<br />

loss on non-current assets.<br />

When an impairment is reversed at a later date, the<br />

carrying amount of the asset (cash flow generating unit)<br />

is increased to the revised estimate of its recoverable