Simplification is the key - Centre for Policy Studies

Simplification is the key - Centre for Policy Studies

Simplification is the key - Centre for Policy Studies

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

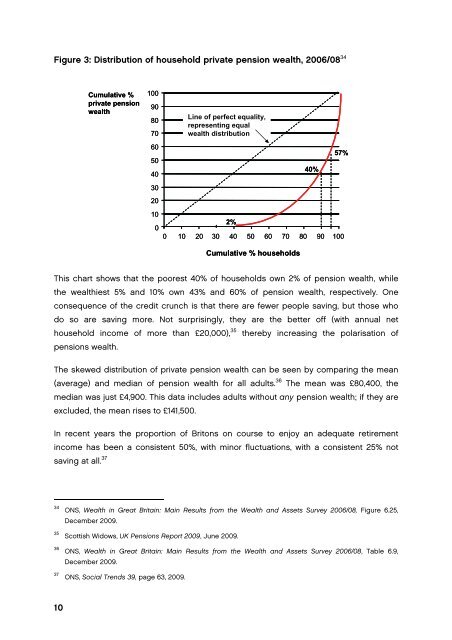

Figure 3: D<strong>is</strong>tribution of household private pension wealth, 2006/08 34<br />

Cumulative %<br />

private pension<br />

wealth<br />

100<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

Line of perfect equality,<br />

representing equal<br />

wealth d<strong>is</strong>tribution<br />

57%<br />

40%<br />

2%<br />

0 10 20<br />

30 40 50 60 70 80 90 100<br />

Cumulative % households<br />

Th<strong>is</strong> chart shows that <strong>the</strong> poorest 40% of households own 2% of pension wealth, while<br />

<strong>the</strong> wealthiest 5% and 10% own 43% and 60% of pension wealth, respectively. One<br />

consequence of <strong>the</strong> credit crunch <strong>is</strong> that <strong>the</strong>re are fewer people saving, but those who<br />

do so are saving more. Not surpr<strong>is</strong>ingly, <strong>the</strong>y are <strong>the</strong> better off (with annual net<br />

household income of more than £20,000), 35 <strong>the</strong>reby increasing <strong>the</strong> polar<strong>is</strong>ation of<br />

pensions wealth.<br />

The skewed d<strong>is</strong>tribution of private pension wealth can be seen by comparing <strong>the</strong> mean<br />

(average) and median of pension wealth <strong>for</strong> all adults. 36 The mean was £80,400, <strong>the</strong><br />

median was just £4,900. Th<strong>is</strong> data includes adults without any pension wealth; if <strong>the</strong>y are<br />

excluded, <strong>the</strong> mean r<strong>is</strong>es to £141,500.<br />

In recent years <strong>the</strong> proportion of Britons on course to enjoy an adequate retirement<br />

income has been a cons<strong>is</strong>tent 50%, with minor fluctuations, with a cons<strong>is</strong>tent 25% not<br />

saving at all. 37<br />

34<br />

35<br />

36<br />

37<br />

ONS, Wealth in Great Britain: Main Results from <strong>the</strong> Wealth and Assets Survey 2006/08, Figure 6.25,<br />

December 2009.<br />

Scott<strong>is</strong>h Widows, UK Pensions Report 2009, June 2009.<br />

ONS, Wealth in Great Britain: Main Results from <strong>the</strong> Wealth and Assets Survey 2006/08, Table 6.9,<br />

December 2009.<br />

ONS, Social Trends 39, page 63, 2009.<br />

10