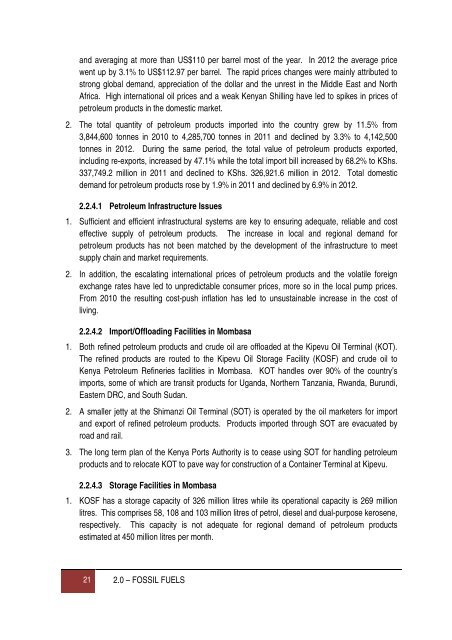

2.2.2 Petroleum Demand and Consumption1. According to the Economic Survey <strong>2013</strong>, consumption of petroleum fuels in Kenya rose from3.1 million Tons of Oil Equivalent (TOE) in 2007 to 3.9 million TOE in 2011 and fell to 3.6 millionTOE in 2012. This is equivalent to a per capita consumption of 94.4 kilograms, which is still lowcompared to the standards of developing economies, and is attributable to low economic growthand over dependence on rain-fed agriculture.2. The Survey further indicates that retail pump outlets and road transport accounted forapproximately 79.7% of petroleum consumption, industrial and commercial sectors accountedfor 11.4% while power generation accounted for 8%.3. A study by the Kenya Institute of Public <strong>Policy</strong> Research and Analysis (KIPPRA) of August2010, estimated that unconstrained demand of Liquefied Petroleum Gas (LPG) was projected tobe over 300,000 metric tonnes in 2012. Suppressed LPG consumption in 2007 was more than75,000 metric tonnes, while the refinery production was about 35,000 metric tonnes.4. The average consumption ofpetroleum products in Kenya hasbeen increasing over the years.In 2004, actual consumption was2.9 million TOE, rising to 3.6million TOE in 2009 and 3.77million TOE in 2010. Some ofthe factors that explain thisvariation in consumption includeGDP growth, electrical energydemand, population growth,urban population growth, andincrease in motorization and airtransport.5. Demand for petroleum products(in m 3 ) is projected to rise by3.1% on average per annum from2009 to 2030. The projectionsunder different scenarios aregiven in Figure 2.2.Fig 2.2 <strong>National</strong> Demand Forecast for petroleum productsDemand (m 3 )12,000,00010,000,0008,000,0006,000,0004,000,0002,000,00002009201020112012<strong>2013</strong>20<strong>14</strong>2015201620172018201920202021202220232024202520262027202820292030YearOPTIMISTICConstrainedOPTIMISTICUnconstrainedBUSINESS ASUSUALConstrainedBUSINESS ASUSUALUnconstrainedPESSIMISTICConstrainedPESSIMISTICUnconstrained2.2.4 Petroleum Supply and Distribution1. The world economy emerged from the recession experienced in 2009 recording a significantgrowth of 4.6% in 2010. This influenced world oil demand and supply. In 2011 oil pricesfluctuated rapidly with the lowest at US$ 95.6 in January, peaking in April at US$ 120 per barrel20 NATIONAL ENERGY POLICY FINAL DRAFT NOVEMBER <strong>2013</strong>

and averaging at more than US$110 per barrel most of the year. In 2012 the average pricewent up by 3.1% to US$112.97 per barrel. The rapid prices changes were mainly attributed tostrong global demand, appreciation of the dollar and the unrest in the Middle East and NorthAfrica. High international oil prices and a weak Kenyan Shilling have led to spikes in prices ofpetroleum products in the domestic market.2. The total quantity of petroleum products imported into the country grew by 11.5% from3,844,600 tonnes in 2010 to 4,285,700 tonnes in 2011 and declined by 3.3% to 4,<strong>14</strong>2,500tonnes in 2012. During the same period, the total value of petroleum products exported,including re-exports, increased by 47.1% while the total import bill increased by 68.2% to KShs.337,749.2 million in 2011 and declined to KShs. 326,921.6 million in 2012. Total domesticdemand for petroleum products rose by 1.9% in 2011 and declined by 6.9% in 2012.2.2.4.1 Petroleum Infrastructure Issues1. Sufficient and efficient infrastructural systems are key to ensuring adequate, reliable and costeffective supply of petroleum products. The increase in local and regional demand forpetroleum products has not been matched by the development of the infrastructure to meetsupply chain and market requirements.2. In addition, the escalating international prices of petroleum products and the volatile foreignexchange rates have led to unpredictable consumer prices, more so in the local pump prices.From 2010 the resulting cost-push inflation has led to unsustainable increase in the cost ofliving.2.2.4.2 Import/Offloading Facilities in Mombasa1. Both refined petroleum products and crude oil are offloaded at the Kipevu Oil Terminal (KOT).The refined products are routed to the Kipevu Oil Storage Facility (KOSF) and crude oil toKenya Petroleum Refineries facilities in Mombasa. KOT handles over 90% of the country’simports, some of which are transit products for Uganda, Northern Tanzania, Rwanda, Burundi,Eastern DRC, and South Sudan.2. A smaller jetty at the Shimanzi Oil Terminal (SOT) is operated by the oil marketers for importand export of refined petroleum products. Products imported through SOT are evacuated byroad and rail.3. The long term plan of the Kenya Ports Authority is to cease using SOT for handling petroleumproducts and to relocate KOT to pave way for construction of a Container Terminal at Kipevu.2.2.4.3 Storage Facilities in Mombasa1. KOSF has a storage capacity of 326 million litres while its operational capacity is 269 millionlitres. This comprises 58, 108 and 103 million litres of petrol, diesel and dual-purpose kerosene,respectively. This capacity is not adequate for regional demand of petroleum productsestimated at 450 million litres per month.21 2.0 – FOSSIL FUELS

- Page 1 and 2: NOVEMBER 2013 DRAFTREPUBLIC OF KENY

- Page 3 and 4: 2.4.4.1 Challenges in Coal explorat

- Page 5 and 6: 4.5.5 Policies and Strategies and I

- Page 7 and 8: Table 10.1 Energy Generation Potent

- Page 9 and 10: FOREWORD BY THE CABINET SECRETARY F

- Page 11 and 12: EXECUTIVE SUMMARY1. This policy doc

- Page 13 and 14: 14. To enhance exploitation of the

- Page 15 and 16: 24. The Government shall establish

- Page 17 and 18: 1.0 - INTRODUCTION1.1 THE ROLE OF E

- Page 19 and 20: (k) Promote appropriate standards,

- Page 21 and 22: (e) The Weights and Measures Act, C

- Page 23 and 24: fund, mobilizing resources for rura

- Page 25 and 26: 2.0 - FOSSIL FUELS2.1 BACKGROUND1.

- Page 27: immense value through acquisition o

- Page 31 and 32: town of Mombasa, through Nairobi to

- Page 33 and 34: 3. The prices in Kenya as published

- Page 35 and 36: 6. It is hoped that the discovery o

- Page 37 and 38: (c) High sulphur levels have advers

- Page 39 and 40: Policies and StrategiesPetroleum Ex

- Page 41 and 42: Policies and StrategiesPetroleum Su

- Page 43 and 44: plants has several advantages over

- Page 45 and 46: Natural GasShort Term2014-2017Mediu

- Page 47 and 48: 3. The introduction of clean coal t

- Page 49 and 50: 6. Lack of a special purpose vehicl

- Page 51 and 52: Policies and StrategiesFossil Fuels

- Page 53 and 54: 4. Geothermal power plants use stea

- Page 55 and 56: about 1,450MW remains unexploited.

- Page 57 and 58: 8. Ownership of physical dam reserv

- Page 59 and 60: (d) Competing interests between dev

- Page 61 and 62: 3.4.2 Challenges1. Unsustainable us

- Page 63 and 64: 4. Land will need to be set aside f

- Page 65 and 66: Limited in Kilifi County generates

- Page 67 and 68: high temperatures estimated at 4-6

- Page 69 and 70: Policies and StrategiesSolar Energy

- Page 71 and 72: 3. Inadequate wind regime data.4. L

- Page 73 and 74: through co-generation and bioethano

- Page 75 and 76: (d) 1 sea wave energy projects with

- Page 77 and 78: 3.12.3 Policies and Strategies and

- Page 79 and 80:

4.0 - ELECTRICITY4.1 BACKGROUND1. E

- Page 81 and 82:

2. It is estimated that as at 2013,

- Page 83 and 84:

Figure 4.2 - Evolution of the Energ

- Page 85 and 86:

(e) Thermal power plants have a rel

- Page 87 and 88:

6. Nuclear fuel can be recycled and

- Page 89 and 90:

Policies and StrategiesNuclear Elec

- Page 91 and 92:

Table 4.5 - Planned Regional Inter-

- Page 93 and 94:

to this worsening situation leading

- Page 95 and 96:

4.5.5 Policies and Strategies and I

- Page 97 and 98:

Policies and StrategiesRural Electr

- Page 99 and 100:

Policies and StrategiesElectricity

- Page 101 and 102:

7. The energy policy and the Energy

- Page 103 and 104:

6.0 - LAND, ENVIRONMENT, HEALTH AND

- Page 105 and 106:

6.2.3 Renewable Energy1. Generally,

- Page 107 and 108:

causes indoor air pollution leading

- Page 109 and 110:

6.5 DISASTER PREPAREDNESS AND MITIG

- Page 111 and 112:

from the licensee.Policies and Stra

- Page 113 and 114:

Policies and StrategiesEnvironment,

- Page 115 and 116:

6.7.4.4 Nuclear ElectricityPolicies

- Page 117 and 118:

of the risk levels.Policies and Str

- Page 119 and 120:

6 It is a further requirement under

- Page 121 and 122:

Policies and StrategiesAccess to En

- Page 123 and 124:

Kenya.Policies and StrategiesEnergy

- Page 125 and 126:

15. Seek financing of clean energy

- Page 127 and 128:

Figure 8.1 - Pass-Through Costs in

- Page 129 and 130:

Table 8.1 - Energy Tariffs and Cost

- Page 131 and 132:

Policies and StrategiesEnergy Prici

- Page 133 and 134:

Policies and StrategiesCross Cuttin

- Page 135 and 136:

3. In 2009, ERC established a commi

- Page 137 and 138:

9.3.3 Policies and Strategies and I

- Page 139 and 140:

9.7 ENERGY RESOURCES BENEFITS SHARI

- Page 141 and 142:

10.0 - ANNEXURESAnnex 10.1 The PSC

- Page 143:

Table 10.3 Nuclear electricity gene

- Page 146 and 147:

Table 10.4 Summary of the Energy St

- Page 148 and 149:

County Population Area (km 2 ) Foss

- Page 150 and 151:

County Population Area (km 2 ) Foss

- Page 152 and 153:

County Population Area (km 2 ) Foss

- Page 154 and 155:

ACRONYMS AND GLOSSARY OF TERMS1. AC

- Page 156 and 157:

RD&DREAREPRMSSMRsSAPPToEVATWpResear

- Page 158:

Reticulation means the network used