Chapter 3 â Policy Implications for Gaelic - University of Edinburgh

Chapter 3 â Policy Implications for Gaelic - University of Edinburgh

Chapter 3 â Policy Implications for Gaelic - University of Edinburgh

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

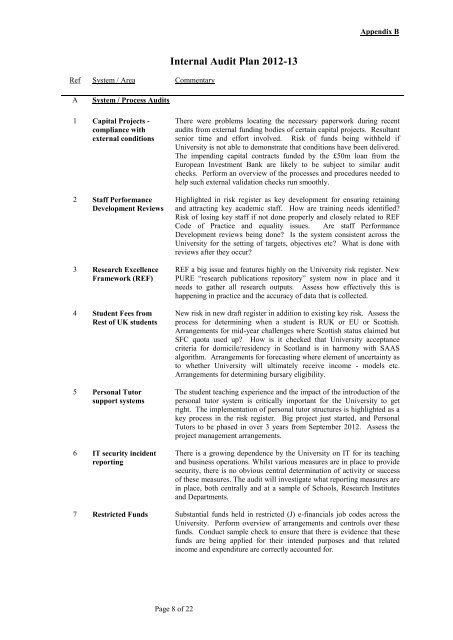

Appendix B<br />

Ref System / Area Commentary<br />

Internal Audit Plan 2012-13<br />

A<br />

System / Process Audits<br />

1 Capital Projects -<br />

compliance with<br />

external conditions<br />

2 Staff Per<strong>for</strong>mance<br />

Development Reviews<br />

3 Research Excellence<br />

Framework (REF)<br />

4 Student Fees from<br />

Rest <strong>of</strong> UK students<br />

5 Personal Tutor<br />

support systems<br />

6 IT security incident<br />

reporting<br />

There were problems locating the necessary paperwork during recent<br />

audits from external funding bodies <strong>of</strong> certain capital projects. Resultant<br />

senior time and ef<strong>for</strong>t involved. Risk <strong>of</strong> funds being withheld if<br />

<strong>University</strong> is not able to demonstrate that conditions have been delivered.<br />

The impending capital contracts funded by the £50m loan from the<br />

European Investment Bank are likely to be subject to similar audit<br />

checks. Per<strong>for</strong>m an overview <strong>of</strong> the processes and procedures needed to<br />

help such external validation checks run smoothly.<br />

Highlighted in risk register as key development <strong>for</strong> ensuring retaining<br />

and attracting key academic staff. How are training needs identified?<br />

Risk <strong>of</strong> losing key staff if not done properly and closely related to REF<br />

Code <strong>of</strong> Practice and equality issues. Are staff Per<strong>for</strong>mance<br />

Development reviews being done? Is the system consistent across the<br />

<strong>University</strong> <strong>for</strong> the setting <strong>of</strong> targets, objectives etc? What is done with<br />

reviews after they occur?<br />

REF a big issue and features highly on the <strong>University</strong> risk register. New<br />

PURE “research publications repository” system now in place and it<br />

needs to gather all research outputs. Assess how effectively this is<br />

happening in practice and the accuracy <strong>of</strong> data that is collected.<br />

New risk in new draft register in addition to existing key risk. Assess the<br />

process <strong>for</strong> determining when a student is RUK or EU or Scottish.<br />

Arrangements <strong>for</strong> mid-year challenges where Scottish status claimed but<br />

SFC quota used up? How is it checked that <strong>University</strong> acceptance<br />

criteria <strong>for</strong> domicile/residency in Scotland is in harmony with SAAS<br />

algorithm. Arrangements <strong>for</strong> <strong>for</strong>ecasting where element <strong>of</strong> uncertainty as<br />

to whether <strong>University</strong> will ultimately receive income - models etc.<br />

Arrangements <strong>for</strong> determining bursary eligibility.<br />

The student teaching experience and the impact <strong>of</strong> the introduction <strong>of</strong> the<br />

personal tutor system is critically important <strong>for</strong> the <strong>University</strong> to get<br />

right. The implementation <strong>of</strong> personal tutor structures is highlighted as a<br />

key process in the risk register. Big project just started, and Personal<br />

Tutors to be phased in over 3 years from September 2012. Assess the<br />

project management arrangements.<br />

There is a growing dependence by the <strong>University</strong> on IT <strong>for</strong> its teaching<br />

and business operations. Whilst various measures are in place to provide<br />

security, there is no obvious central determination <strong>of</strong> activity or success<br />

<strong>of</strong> these measures. The audit will investigate what reporting measures are<br />

in place, both centrally and at a sample <strong>of</strong> Schools, Research Institutes<br />

and Departments.<br />

7 Restricted Funds Substantial funds held in restricted (J) e-financials job codes across the<br />

<strong>University</strong>. Per<strong>for</strong>m overview <strong>of</strong> arrangements and controls over these<br />

funds. Conduct sample check to ensure that there is evidence that these<br />

funds are being applied <strong>for</strong> their intended purposes and that related<br />

income and expenditure are correctly accounted <strong>for</strong>.<br />

Page 8 <strong>of</strong> 22