Revenue for Telecoms

2cdncba

2cdncba

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Revenue</strong> <strong>for</strong> <strong>Telecoms</strong> – Issues In-Depth | 99<br />

5.1 Determine stand-alone selling prices |<br />

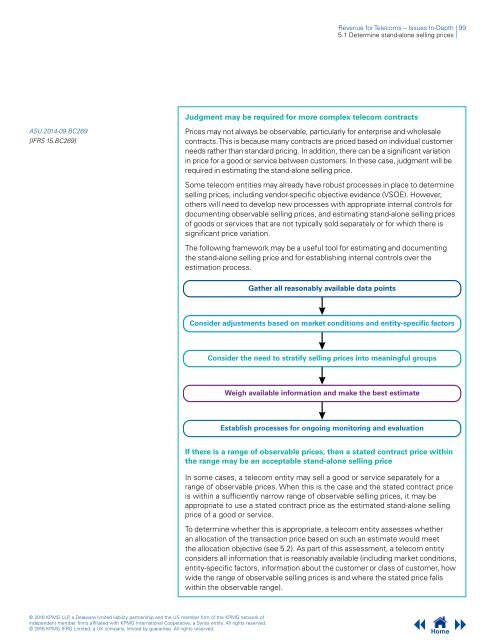

Judgment may be required <strong>for</strong> more complex telecom contracts<br />

ASU 2014-09.BC269<br />

[IFRS 15.BC269]<br />

Prices may not always be observable, particularly <strong>for</strong> enterprise and wholesale<br />

contracts. This is because many contracts are priced based on individual customer<br />

needs rather than standard pricing. In addition, there can be a significant variation<br />

in price <strong>for</strong> a good or service between customers. In these case, judgment will be<br />

required in estimating the stand-alone selling price.<br />

Some telecom entities may already have robust processes in place to determine<br />

selling prices, including vendor-specific objective evidence (VSOE). However,<br />

others will need to develop new processes with appropriate internal controls <strong>for</strong><br />

documenting observable selling prices, and estimating stand-alone selling prices<br />

of goods or services that are not typically sold separately or <strong>for</strong> which there is<br />

significant price variation.<br />

The following framework may be a useful tool <strong>for</strong> estimating and documenting<br />

the stand-alone selling price and <strong>for</strong> establishing internal controls over the<br />

estimation process.<br />

Gather all reasonably available data points<br />

Consider adjustments based on market conditions and entity-specific factors<br />

Consider the need to stratify selling prices into meaningful groups<br />

Weigh available in<strong>for</strong>mation and make the best estimate<br />

Establish processes <strong>for</strong> ongoing monitoring and evaluation<br />

If there is a range of observable prices, then a stated contract price within<br />

the range may be an acceptable stand-alone selling price<br />

In some cases, a telecom entity may sell a good or service separately <strong>for</strong> a<br />

range of observable prices. When this is the case and the stated contract price<br />

is within a sufficiently narrow range of observable selling prices, it may be<br />

appropriate to use a stated contract price as the estimated stand-alone selling<br />

price of a good or service.<br />

To determine whether this is appropriate, a telecom entity assesses whether<br />

an allocation of the transaction price based on such an estimate would meet<br />

the allocation objective (see 5.2). As part of this assessment, a telecom entity<br />

considers all in<strong>for</strong>mation that is reasonably available (including market conditions,<br />

entity-specific factors, in<strong>for</strong>mation about the customer or class of customer, how<br />

wide the range of observable selling prices is and where the stated price falls<br />

within the observable range).<br />

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of<br />

independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.<br />

© 2016 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.<br />

Home