Revenue for Telecoms

2cdncba

2cdncba

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

20 | <strong>Revenue</strong> <strong>for</strong> <strong>Telecoms</strong> – Issues In-Depth<br />

| 2 Step 1: Identify the contract with a customer<br />

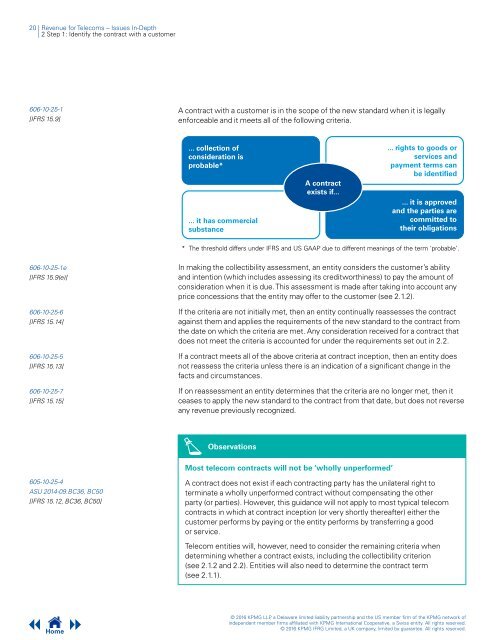

606-10-25-1<br />

[IFRS 15.9]<br />

A contract with a customer is in the scope of the new standard when it is legally<br />

en<strong>for</strong>ceable and it meets all of the following criteria.<br />

... collection of<br />

consideration is<br />

probable*<br />

... it has commercial<br />

substance<br />

A contract<br />

exists if...<br />

... rights to goods or<br />

services and<br />

payment terms can<br />

be identified<br />

... it is approved<br />

and the parties are<br />

committed to<br />

their obligations<br />

* The threshold differs under IFRS and US GAAP due to different meanings of the term ‘ probable ’.<br />

606-10-25-1e<br />

[IFRS 15.9(e)]<br />

606-10-25-6<br />

[IFRS 15.14]<br />

606-10-25-5<br />

[IFRS 15.13]<br />

606-10-25-7<br />

[IFRS 15.15]<br />

In making the collectibility assessment, an entity considers the customer’s ability<br />

and intention (which includes assessing its creditworthiness) to pay the amount of<br />

consideration when it is due. This assessment is made after taking into account any<br />

price concessions that the entity may offer to the customer (see 2.1.2).<br />

If the criteria are not initially met, then an entity continually reassesses the contract<br />

against them and applies the requirements of the new standard to the contract from<br />

the date on which the criteria are met. Any consideration received <strong>for</strong> a contract that<br />

does not meet the criteria is accounted <strong>for</strong> under the requirements set out in 2.2.<br />

If a contract meets all of the above criteria at contract inception, then an entity does<br />

not reassess the criteria unless there is an indication of a significant change in the<br />

facts and circumstances.<br />

If on reassessment an entity determines that the criteria are no longer met, then it<br />

ceases to apply the new standard to the contract from that date, but does not reverse<br />

any revenue previously recognized.<br />

Observations<br />

Most telecom contracts will not be ‘wholly unper<strong>for</strong>med’<br />

605-10-25-4<br />

ASU 2014-09.BC36, BC50<br />

[IFRS 15.12, BC36, BC50]<br />

A contract does not exist if each contracting party has the unilateral right to<br />

terminate a wholly unper<strong>for</strong>med contract without compensating the other<br />

party (or parties). However, this guidance will not apply to most typical telecom<br />

contracts in which at contract inception (or very shortly thereafter) either the<br />

customer per<strong>for</strong>ms by paying or the entity per<strong>for</strong>ms by transferring a good<br />

or service.<br />

Telecom entities will, however, need to consider the remaining criteria when<br />

determining whether a contract exists, including the collectibility criterion<br />

(see 2.1.2 and 2.2). Entities will also need to determine the contract term<br />

(see 2.1.1).<br />

Home<br />

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of<br />

independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.<br />

© 2016 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.