Revenue for Telecoms

2cdncba

2cdncba

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Revenue</strong> <strong>for</strong> <strong>Telecoms</strong> – Issues In-Depth | 119<br />

6.2 Per<strong>for</strong>mance obligations satisfied over time |<br />

Criterion 3<br />

606-10-25-28<br />

[IFRS 15.36]<br />

In assessing whether an asset has an alternative use, at contract inception an entity<br />

considers its ability to readily direct that asset in its completed state <strong>for</strong> another use,<br />

such as selling it to a different customer.<br />

606-10-55-6, 55-8 – 55-10, ASU 2014-09.BC127<br />

[IFRS 15.B4, B6–B8, BC127]<br />

Applying Criteria 1 and 3<br />

Potential contractual restrictions or practical restrictions may prevent the entity from<br />

transferring the remaining per<strong>for</strong>mance obligation to another entity (Criterion 1) or<br />

directing the asset <strong>for</strong> another use (Criterion 3). The new standard provides guidance<br />

on whether these facts or possible termination impact the assessment of those<br />

criteria. It provides the following guidance on the assumptions that an entity should<br />

make when applying Criteria 1 and 3.<br />

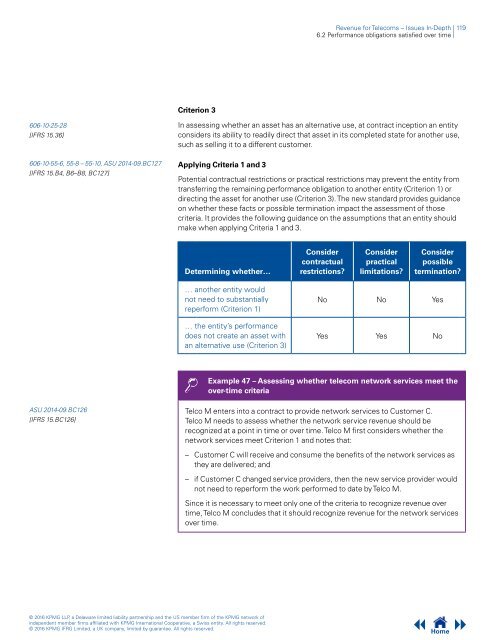

Determining whether…<br />

Consider<br />

contractual<br />

restrictions?<br />

Consider<br />

practical<br />

limitations?<br />

Consider<br />

possible<br />

termination?<br />

… another entity would<br />

not need to substantially<br />

reper<strong>for</strong>m (Criterion 1)<br />

… the entity’s per<strong>for</strong>mance<br />

does not create an asset with<br />

an alternative use (Criterion 3)<br />

No No Yes<br />

Yes Yes No<br />

Example 47 – Assessing whether telecom network services meet the<br />

over-time criteria<br />

ASU 2014-09.BC126<br />

[IFRS 15.BC126]<br />

Telco M enters into a contract to provide network services to Customer C.<br />

Telco M needs to assess whether the network service revenue should be<br />

recognized at a point in time or over time. Telco M first considers whether the<br />

network services meet Criterion 1 and notes that:<br />

– Customer C will receive and consume the benefits of the network services as<br />

they are delivered; and<br />

– if Customer C changed service providers, then the new service provider would<br />

not need to reper<strong>for</strong>m the work per<strong>for</strong>med to date by Telco M.<br />

Since it is necessary to meet only one of the criteria to recognize revenue over<br />

time, Telco M concludes that it should recognize revenue <strong>for</strong> the network services<br />

over time.<br />

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of<br />

independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.<br />

© 2016 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.<br />

Home