Revenue for Telecoms

2cdncba

2cdncba

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Revenue</strong> <strong>for</strong> <strong>Telecoms</strong> – Issues In-Depth | 121<br />

6.3 Measuring progress toward complete satisfaction of a per<strong>for</strong>mance obligation |<br />

By contrast, the new standard introduces new concepts and uses new wording<br />

that telecom entities need to apply to the specific facts and circumstances of<br />

individual per<strong>for</strong>mance obligations. Subtle differences in contract terms could<br />

result in different assessment outcomes – and there<strong>for</strong>e significant differences in<br />

the timing of revenue recognition compared with current practice.<br />

Comparison with current US GAAP<br />

Some similarities, but new concepts to be applied<br />

Criteria 1 and 3 of the new standard will require telecom entities to think<br />

differently about the satisfaction of per<strong>for</strong>mance obligations. In general,<br />

the impact of applying the criteria will vary depending on relevant facts and<br />

circumstances, and subtle differences in contract terms could result in different<br />

assessment outcomes. These different assessments could create significant<br />

differences in the timing or pattern of revenue recognition.<br />

6.3 Measuring progress toward complete<br />

satisfaction of a per<strong>for</strong>mance obligation<br />

Requirements of the new standard<br />

606-10-25-31 – 25-35, 55-17 – 55-21<br />

[IFRS 15.39–43, B15–B19]<br />

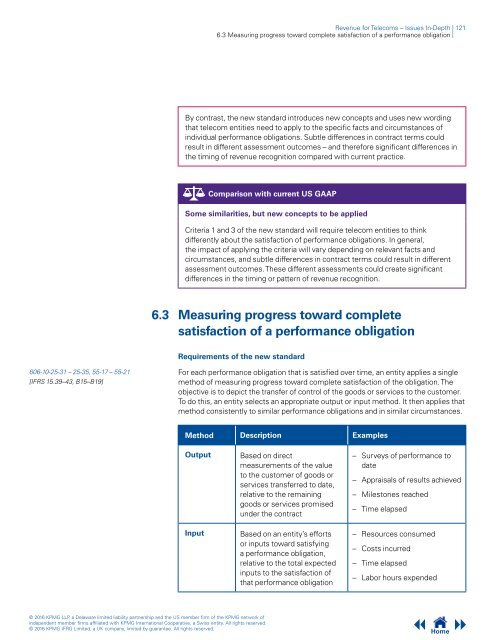

For each per<strong>for</strong>mance obligation that is satisfied over time, an entity applies a single<br />

method of measuring progress toward complete satisfaction of the obligation. The<br />

objective is to depict the transfer of control of the goods or services to the customer.<br />

To do this, an entity selects an appropriate output or input method. It then applies that<br />

method consistently to similar per<strong>for</strong>mance obligations and in similar circumstances.<br />

Method Description Examples<br />

Output<br />

Based on direct<br />

measurements of the value<br />

to the customer of goods or<br />

services transferred to date,<br />

relative to the remaining<br />

goods or services promised<br />

under the contract<br />

– Surveys of per<strong>for</strong>mance to<br />

date<br />

– Appraisals of results achieved<br />

– Milestones reached<br />

– Time elapsed<br />

Input<br />

Based on an entity’s ef<strong>for</strong>ts<br />

or inputs toward satisfying<br />

a per<strong>for</strong>mance obligation,<br />

relative to the total expected<br />

inputs to the satisfaction of<br />

that per<strong>for</strong>mance obligation<br />

– Resources consumed<br />

– Costs incurred<br />

– Time elapsed<br />

– Labor hours expended<br />

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of<br />

independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.<br />

© 2016 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.<br />

Home