Revenue for Telecoms

2cdncba

2cdncba

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Revenue</strong> <strong>for</strong> <strong>Telecoms</strong> – Issues In-Depth | 157<br />

9 Nonrefundable up-front fees |<br />

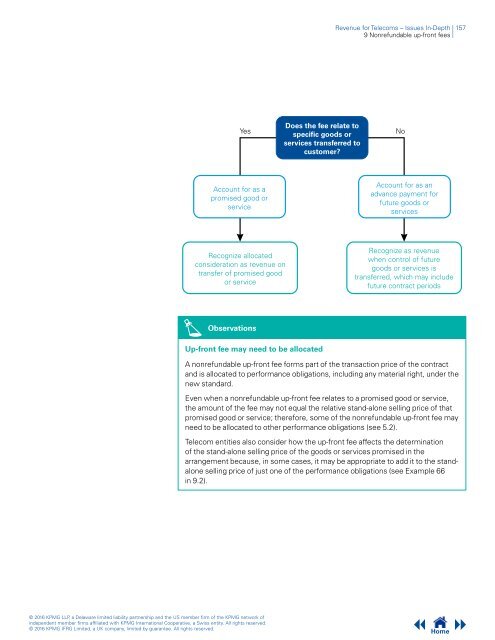

Yes<br />

Does the fee relate to<br />

specific goods or<br />

services transferred to<br />

customer?<br />

No<br />

Account <strong>for</strong> as a<br />

promised good or<br />

service<br />

Account <strong>for</strong> as an<br />

advance payment <strong>for</strong><br />

future goods or<br />

services<br />

Recognize allocated<br />

consideration as revenue on<br />

transfer of promised good<br />

or service<br />

Recognize as revenue<br />

when control of future<br />

goods or services is<br />

transferred, which may include<br />

future contract periods<br />

Observations<br />

Up-front fee may need to be allocated<br />

A nonrefundable up-front fee <strong>for</strong>ms part of the transaction price of the contract<br />

and is allocated to per<strong>for</strong>mance obligations, including any material right, under the<br />

new standard.<br />

Even when a nonrefundable up-front fee relates to a promised good or service,<br />

the amount of the fee may not equal the relative stand-alone selling price of that<br />

promised good or service; there<strong>for</strong>e, some of the nonrefundable up-front fee may<br />

need to be allocated to other per<strong>for</strong>mance obligations (see 5.2).<br />

Telecom entities also consider how the up-front fee affects the determination<br />

of the stand-alone selling price of the goods or services promised in the<br />

arrangement because, in some cases, it may be appropriate to add it to the standalone<br />

selling price of just one of the per<strong>for</strong>mance obligations (see Example 66<br />

in 9.2).<br />

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of<br />

independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.<br />

© 2016 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.<br />

Home