Revenue for Telecoms

2cdncba

2cdncba

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Revenue</strong> <strong>for</strong> <strong>Telecoms</strong> – Issues In-Depth | 9<br />

1.1 In scope |<br />

1 Scope<br />

Overview<br />

The new standard applies to contracts to deliver goods or services to a customer.<br />

However, if a contract, or part of a contract, is in the scope of other specific<br />

requirements, then it falls outside the scope of the new standard. For example,<br />

a lease would be in the scope of the leasing standards. This may apply to some<br />

equipment provided to customers in a telecom contract.<br />

Furthermore, some non-monetary exchanges may be outside the scope of the<br />

new standard, which could potentially apply to exchanges of airtime or network<br />

capacity.<br />

In some cases, the new standard will be applied to part of a contract or to a<br />

portfolio of contracts. The new standard provides guidance on when it should or<br />

may be applied to these circumstances and how to apply it.<br />

1.1 In scope<br />

Requirements of the new standard<br />

606-10-15-3<br />

[IFRS 15.6]<br />

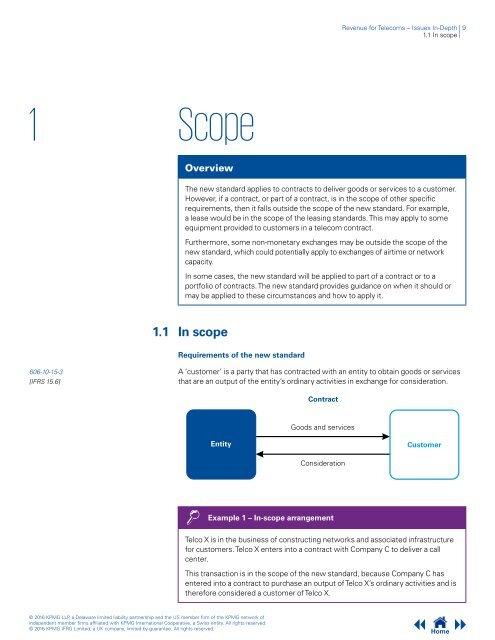

A ‘customer’ is a party that has contracted with an entity to obtain goods or services<br />

that are an output of the entity’s ordinary activities in exchange <strong>for</strong> consideration.<br />

Contract<br />

Goods and services<br />

Entity<br />

Customer<br />

Consideration<br />

Example 1 – In-scope arrangement<br />

Telco X is in the business of constructing networks and associated infrastructure<br />

<strong>for</strong> customers. Telco X enters into a contract with Company C to deliver a call<br />

center.<br />

This transaction is in the scope of the new standard, because Company C has<br />

entered into a contract to purchase an output of Telco X’s ordinary activities and is<br />

there<strong>for</strong>e considered a customer of Telco X.<br />

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of<br />

independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.<br />

© 2016 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.<br />

Home