Revenue for Telecoms

2cdncba

2cdncba

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

54 | <strong>Revenue</strong> <strong>for</strong> <strong>Telecoms</strong> – Issues In-Depth<br />

| 3 Step 2: Identify the per<strong>for</strong>mance obligations in the contract<br />

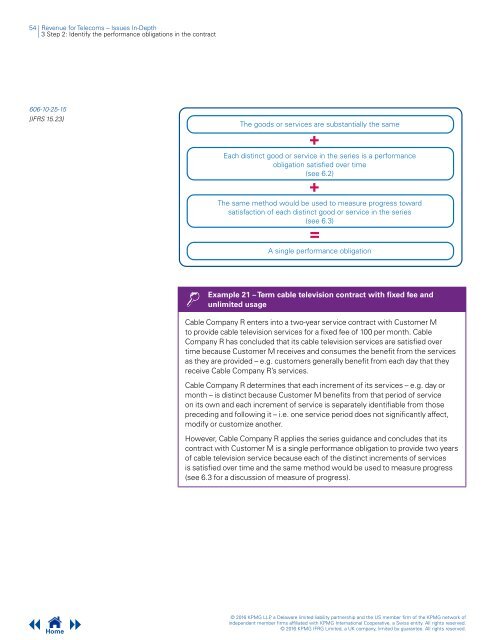

606-10-25-15<br />

[IFRS 15.23]<br />

The goods or services are substantially the same<br />

+<br />

Each distinct good or service in the series is a per<strong>for</strong>mance<br />

obligation satisfied over time<br />

(see 6.2)<br />

+<br />

The same method would be used to measure progress toward<br />

satisfaction of each distinct good or service in the series<br />

(see 6.3)<br />

=<br />

A single per<strong>for</strong>mance obligation<br />

Example 21 – Term cable television contract with fixed fee and<br />

unlimited usage<br />

Cable Company R enters into a two-year service contract with Customer M<br />

to provide cable television services <strong>for</strong> a fixed fee of 100 per month. Cable<br />

Company R has concluded that its cable television services are satisfied over<br />

time because Customer M receives and consumes the benefit from the services<br />

as they are provided – e.g. customers generally benefit from each day that they<br />

receive Cable Company R’s services.<br />

Cable Company R determines that each increment of its services – e.g. day or<br />

month – is distinct because Customer M benefits from that period of service<br />

on its own and each increment of service is separately identifiable from those<br />

preceding and following it – i.e. one service period does not significantly affect,<br />

modify or customize another.<br />

However, Cable Company R applies the series guidance and concludes that its<br />

contract with Customer M is a single per<strong>for</strong>mance obligation to provide two years<br />

of cable television service because each of the distinct increments of services<br />

is satisfied over time and the same method would be used to measure progress<br />

(see 6.3 <strong>for</strong> a discussion of measure of progress).<br />

Home<br />

© 2016 KPMG LLP, a Delaware limited liability partnership and the US member firm of the KPMG network of<br />

independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.<br />

© 2016 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.