OECD Economic Outlook 69 - Biblioteca Hegoa

OECD Economic Outlook 69 - Biblioteca Hegoa

OECD Economic Outlook 69 - Biblioteca Hegoa

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

124 - <strong>OECD</strong> <strong>Economic</strong> <strong>Outlook</strong> <strong>69</strong><br />

Strong export growth continued to support GDP throughout 2000 despite falling domestic demand. Export competitiveness<br />

was supported by real wage moderation, but unemployment increased. The government was able to meet its fiscal<br />

targets and pushed ahead with reforms, inducing a significant increase in foreign direct investment. However, structural<br />

changes are taking longer than expected to work through the economy. Nevertheless, domestic demand is expected to<br />

increase in 2001, and GDP growth to strengthen despite a sharply reduced contribution of net exports.<br />

Some deterioration in the budget position is expected this year, largely accounted for by the one-off costs of bank restructuring.<br />

But with the fiscal room for manoeuvre extremely limited, the authorities will have to guard against any lapse of<br />

discipline on current expenditure.<br />

Per cent<br />

40<br />

Weak growth was a result of<br />

structural adjustment<br />

Price and wage increases<br />

remained moderate<br />

Increasing consumption is<br />

expected to lead to a further<br />

pick up in growth...<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

-20<br />

-30<br />

Exports<br />

Imports<br />

Slovak Republic<br />

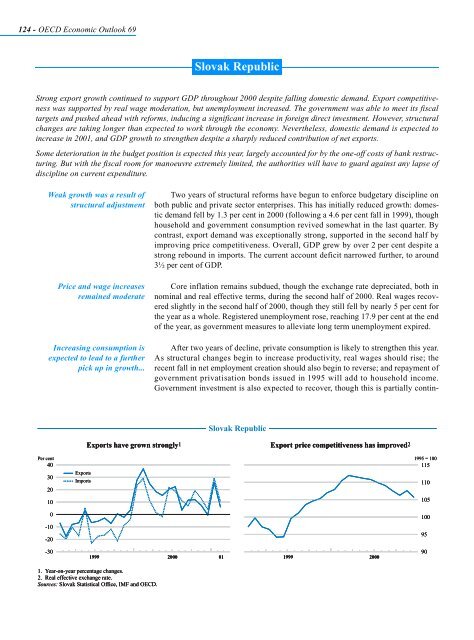

Two years of structural reforms have begun to enforce budgetary discipline on<br />

both public and private sector enterprises. This has initially reduced growth: domestic<br />

demand fell by 1.3 per cent in 2000 (following a 4.6 per cent fall in 1999), though<br />

household and government consumption revived somewhat in the last quarter. By<br />

contrast, export demand was exceptionally strong, supported in the second half by<br />

improving price competitiveness. Overall, GDP grew by over 2 per cent despite a<br />

strong rebound in imports. The current account deficit narrowed further, to around<br />

3½ per cent of GDP.<br />

Core inflation remains subdued, though the exchange rate depreciated, both in<br />

nominal and real effective terms, during the second half of 2000. Real wages recovered<br />

slightly in the second half of 2000, though they still fell by nearly 5 per cent for<br />

the year as a whole. Registered unemployment rose, reaching 17.9 per cent at the end<br />

of the year, as government measures to alleviate long term unemployment expired.<br />

After two years of decline, private consumption is likely to strengthen this year.<br />

As structural changes begin to increase productivity, real wages should rise; the<br />

recent fall in net employment creation should also begin to reverse; and repayment of<br />

government privatisation bonds issued in 1995 will add to household income.<br />

Government investment is also expected to recover, though this is partially contin-<br />

Slovak Republic<br />

Exports have grown strongly1 strongly1 strongly1 Export price competitiveness has improved2 improved2 improved2<br />

1999 2000 01 1999 2000<br />

1. Year-on-year percentage changes.<br />

2. Real effective exchange rate.<br />

Sources: Slovak Statistical Office, IMF and <strong>OECD</strong>.<br />

1995 = 100<br />

115<br />

110<br />

105<br />

100<br />

95<br />

90