OECD Economic Outlook 69 - Biblioteca Hegoa

OECD Economic Outlook 69 - Biblioteca Hegoa

OECD Economic Outlook 69 - Biblioteca Hegoa

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

24 - <strong>OECD</strong> <strong>Economic</strong> <strong>Outlook</strong> <strong>69</strong><br />

Falling US interest rates will<br />

provide support to some heavily<br />

indebted countries<br />

If a recession were to take place<br />

in the United States in<br />

the near term…<br />

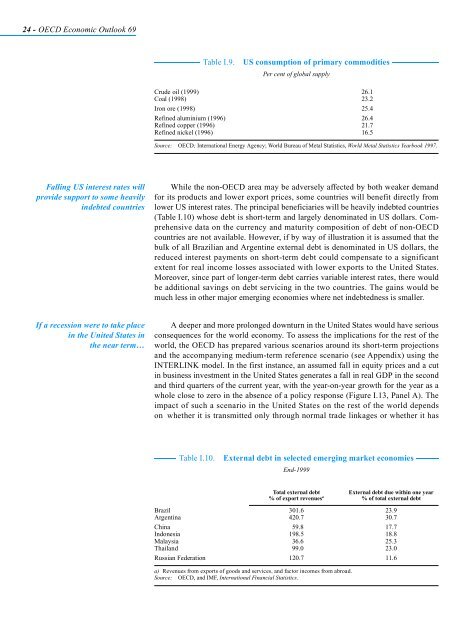

Table I.9. US consumption of primary commodities<br />

Per cent of global supply<br />

Crude oil (1999) 26.1<br />

Coal (1998) 23.2<br />

Iron ore (1998) 25.4<br />

Refined aluminium (1996) 26.4<br />

Refined copper (1996) 21.7<br />

Refined nickel (1996) 16.5<br />

Source: <strong>OECD</strong>; International Energy Agency; World Bureau of Metal Statistics, World Metal Statistics Yearbook 1997.<br />

While the non-<strong>OECD</strong> area may be adversely affected by both weaker demand<br />

for its products and lower export prices, some countries will benefit directly from<br />

lower US interest rates. The principal beneficiaries will be heavily indebted countries<br />

(Table I.10) whose debt is short-term and largely denominated in US dollars. Comprehensive<br />

data on the currency and maturity composition of debt of non-<strong>OECD</strong><br />

countries are not available. However, if by way of illustration it is assumed that the<br />

bulk of all Brazilian and Argentine external debt is denominated in US dollars, the<br />

reduced interest payments on short-term debt could compensate to a significant<br />

extent for real income losses associated with lower exports to the United States.<br />

Moreover, since part of longer-term debt carries variable interest rates, there would<br />

be additional savings on debt servicing in the two countries. The gains would be<br />

much less in other major emerging economies where net indebtedness is smaller.<br />

A deeper and more prolonged downturn in the United States would have serious<br />

consequences for the world economy. To assess the implications for the rest of the<br />

world, the <strong>OECD</strong> has prepared various scenarios around its short-term projections<br />

and the accompanying medium-term reference scenario (see Appendix) using the<br />

INTERLINK model. In the first instance, an assumed fall in equity prices and a cut<br />

in business investment in the United States generates a fall in real GDP in the second<br />

and third quarters of the current year, with the year-on-year growth for the year as a<br />

whole close to zero in the absence of a policy response (Figure I.13, Panel A). The<br />

impact of such a scenario in the United States on the rest of the world depends<br />

on whether it is transmitted only through normal trade linkages or whether it has<br />

Table I.10. External debt in selected emerging market economies<br />

End-1999<br />

Total external debt<br />

% of export revenues a<br />

External debt due within one year<br />

% of total external debt<br />

Brazil 301.6 23.9<br />

Argentina 420.7 30.7<br />

China 59.8 17.7<br />

Indonesia 198.5 18.8<br />

Malaysia 36.6 25.3<br />

Thailand 99.0 23.0<br />

Russian Federation 120.7 11.6<br />

a) Revenues from exports of goods and services, and factor incomes from abroad.<br />

Source: <strong>OECD</strong>, and IMF, International Financial Statistics.